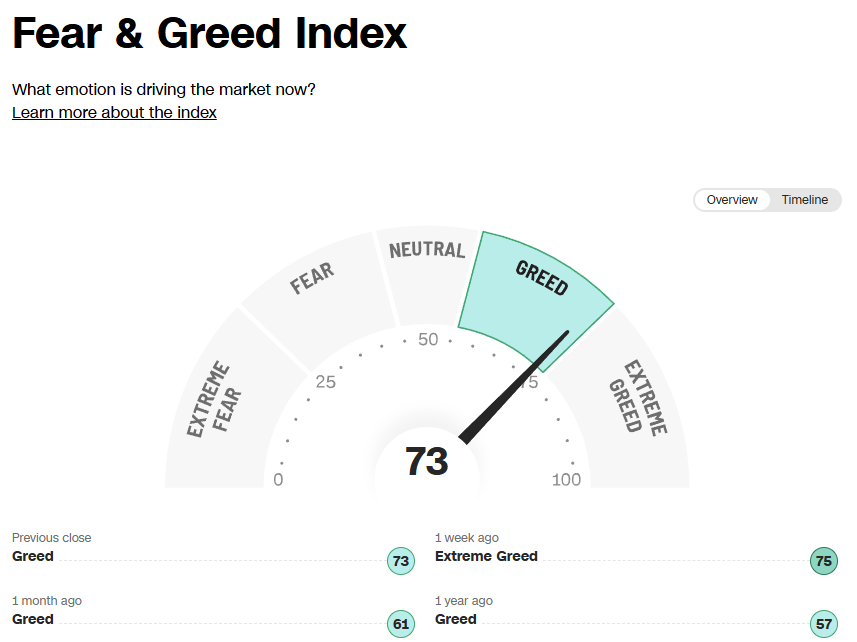

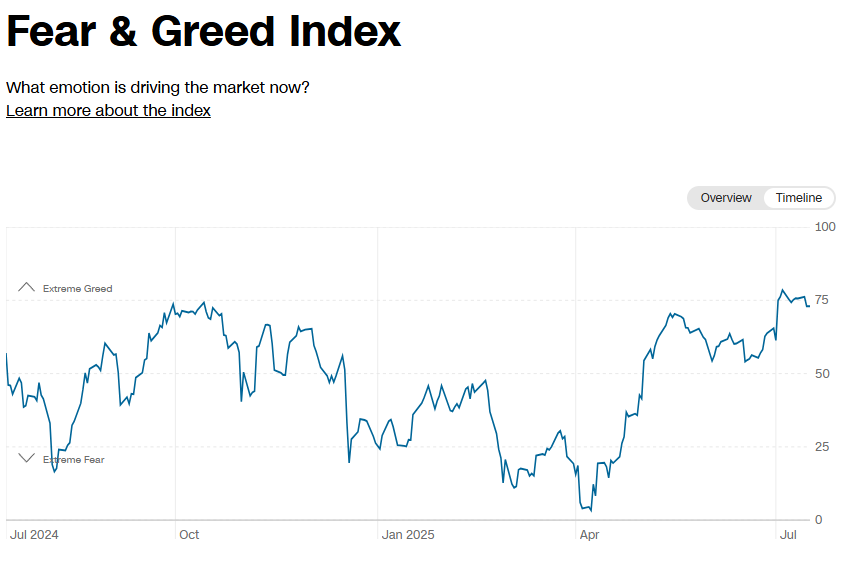

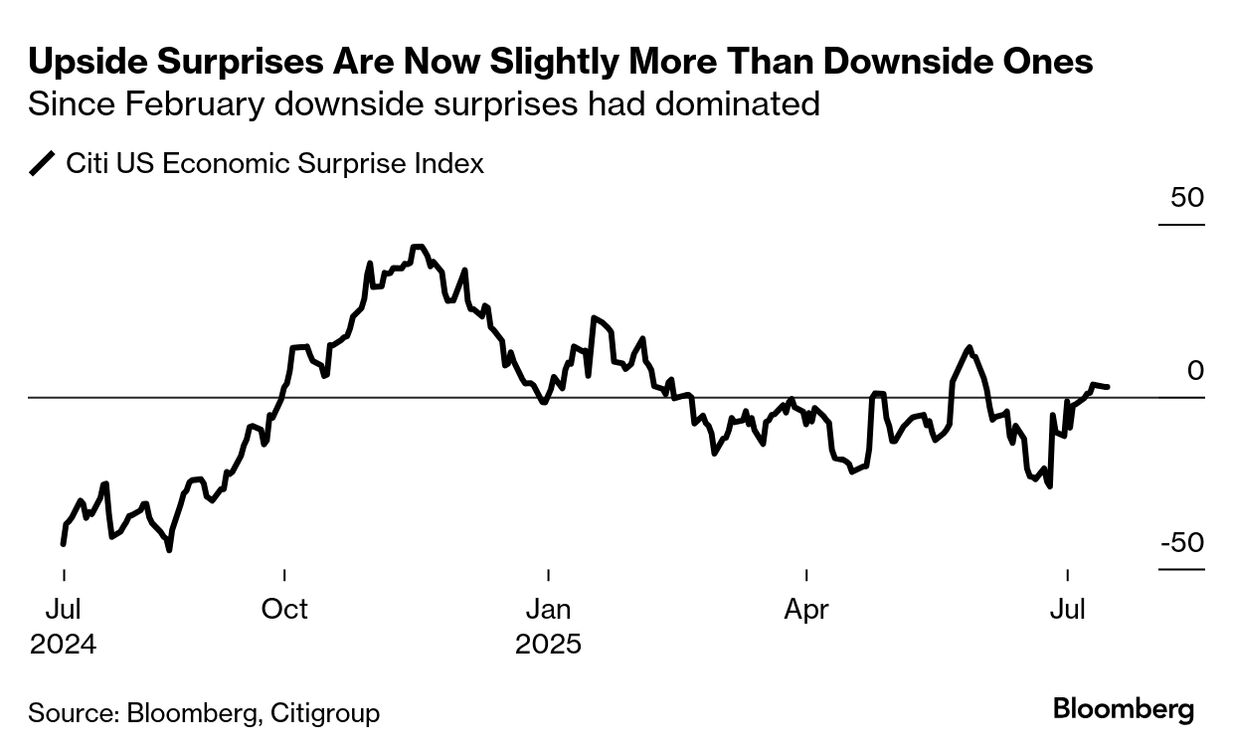

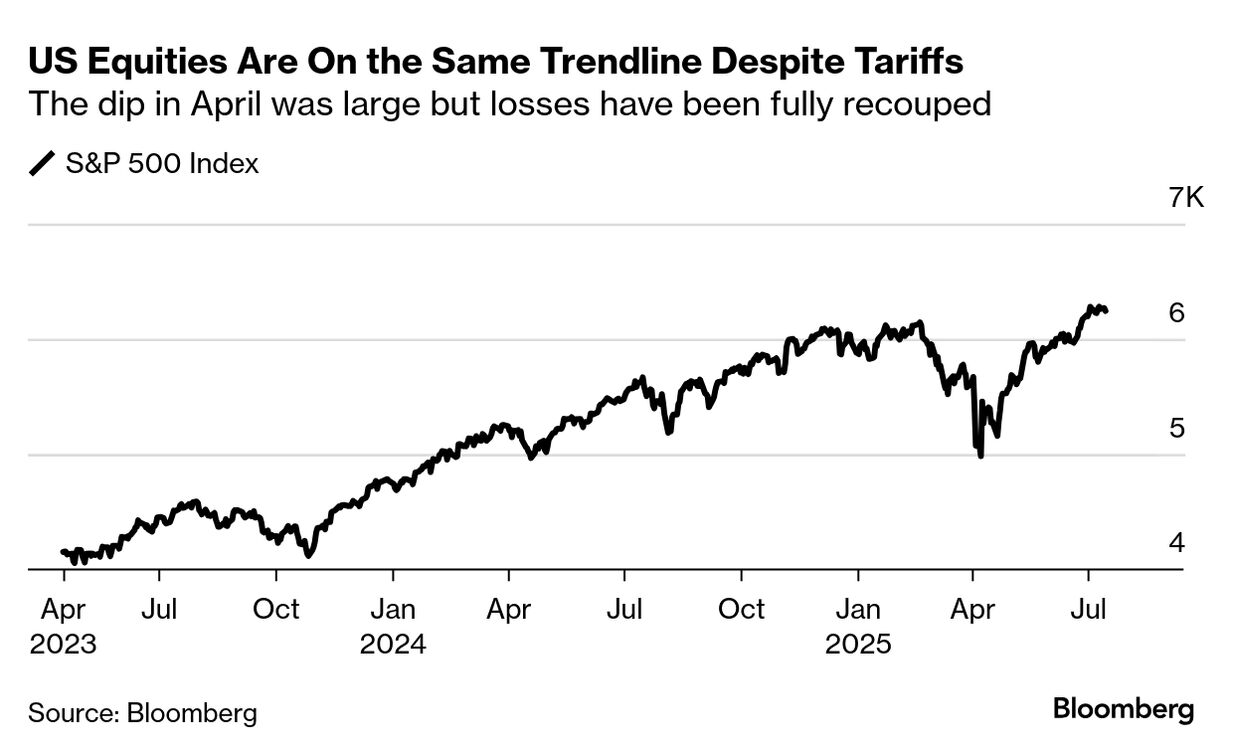

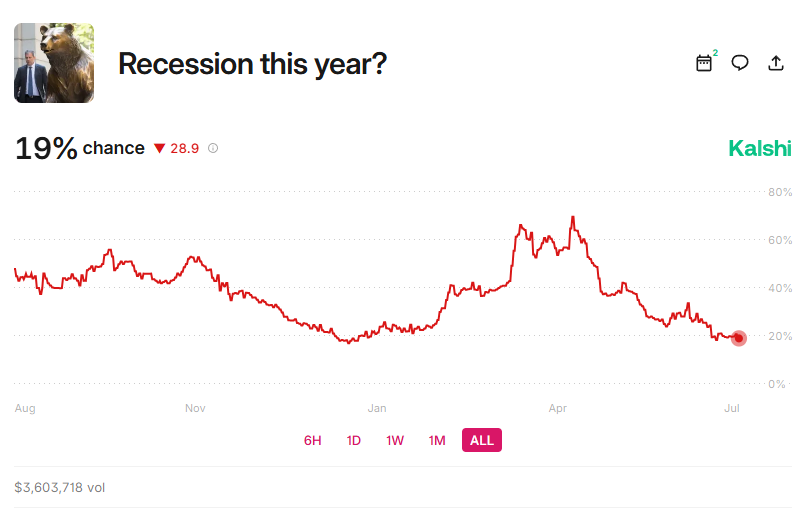

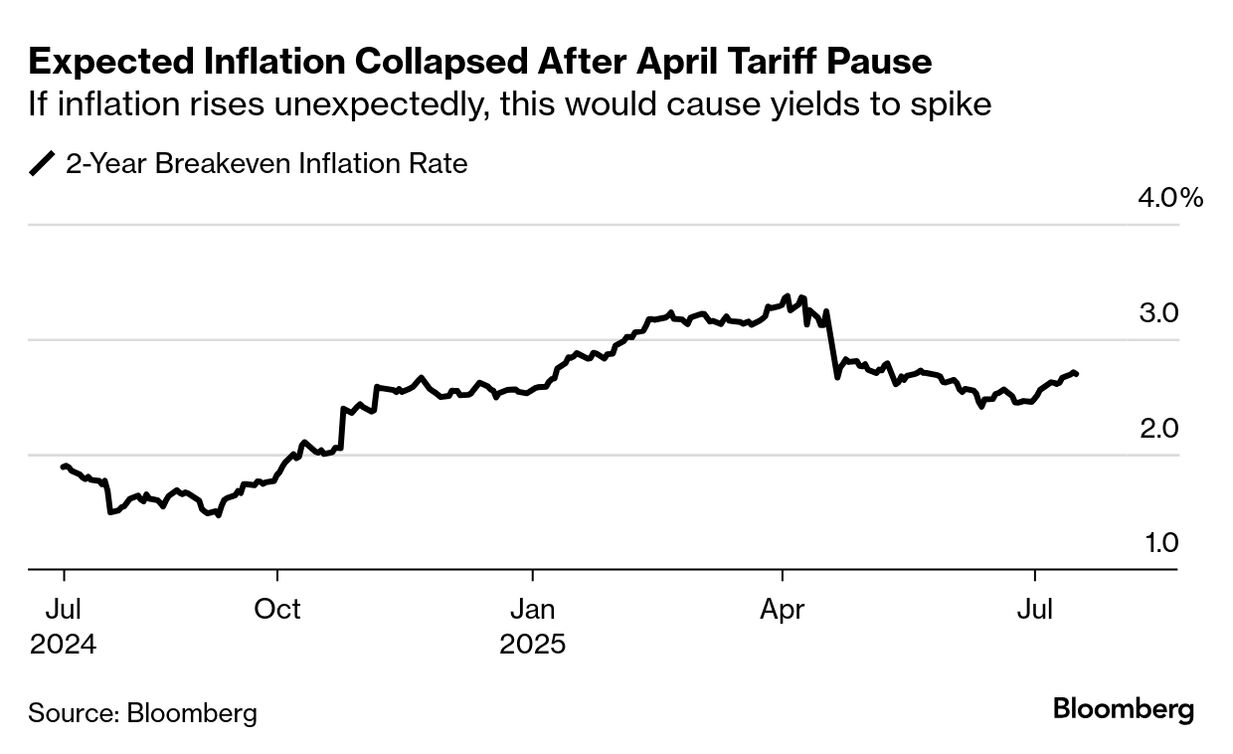

| While the ongoing earnings season gives investors a chance to focus on the thing that actually underpins stocks — earnings — there’s still a tariff overhang to contend with. Despite that, the S&P 500 has rallied about 25% from the April lows, such that it is largely on the same trendline it was before April 2. And betting platform Kalshi shows investors think a recession this year is a remote possibility. Trump has to see this as vindication of his economic policy. And that makes higher tariffs on Aug. 1 more likely, not less. US tariff revenue is at a record high, filling government coffers to offset the tax cuts. And that has been rewarded with repeated record highs on the Nasdaq 100 and the S&P 500. In Trump’s mind, then, now must be the time to press his advantage. Therefore, we have to see the proposed 30% tariff on the EU, 30% on Mexico and 50% on Brazil not as bargaining chips, but levels Trump is willing to impose. Slowly at first, then all at once? | The stock market’s momentum may be enough to get through a second Liberation Day-style tariff salvo without as severe a hit to prices. But it was the triple threat of quickening inflation, rising bond yields and a sinking economy that were the toxic mix that cratered stocks. That mix — which hurts revenue and margins and reduces the present value of future earnings — is what it would take to hurt the market again. The evidence so far is that revenue and margins have held up — and the economy, too. So the recent data work to keep the market in disbelief about any coming recession or earnings hit. The reality, of course, is that the labor market is softening and inflation has only just begun to rise, such that the recently mooted import tax rates Trump has floated are almost certain to create exactly the mix that caused panic in April. If that outcome materializes, the market will catch on to that. And the Treasury market? Bond traders haven’t been anywhere near as upbeat as stock investors, though bond vigilantes don’t seem to be out in full force. If you look at the breakeven inflation rate that makes an investor in Treasury Inflation Protected Securities whole versus conventional Treasury bonds, it’s now at levels almost 70 basis points lower than it was after the April 2 tariff announcement. If inflation accelerates unexpectedly, this would cause yields to shoot higher. As for stocks, unexpected inflation and sky-high tariffs would be a catalyst for a re-appraisal there, too — even if earnings come through ok. Trump may have successfully helped the stock market reach new highs by delaying Liberation Day tariffs, but eventually he’s going to have to make a decision. Ironically, the stock market’s new highs — predicated on Trump not imposing any draconian tariffs — may be just the thing that cajoles him into imposing sky-high levies, with negative consequences for equities. |