| Welcome to Next Africa, a twice-weekly newsletter on where the continent stands now — and where it’s headed. Sign up here to have it delivered to your email. With just days to go until the US is due to impose punishing new tariffs on imports, not a single African nation has clinched a deal with Washington to soften the impact. The new dispensation aims to give effect to President Donald Trump’s pledge to reset relations between America and Africa by pivoting from aid to trade.  The financial district and port in Cape Town, South Africa’s second-biggest city. Photographer: Dwayne Senior/Bloomberg Trump has been as good as his word with regard to halting most handouts to the least-developed region, bringing key healthcare initiatives and other programs to a halt. But instead of clearing a path for African exporters to do more business with the world’s biggest economy, he appears intent on doing just the opposite. Trump has effectively scrapped the 25-year-old African Growth and Opportunity Act, which was endorsed by Congress and enabled thousands of products from more than 30 countries to enter the US duty free. The new levies will place billions of dollars of exports — and the jobs they support — at risk. African nations are banking on Washington granting them reprieves so accords can be agreed that don’t decimate their economies. While the US leader is notoriously unpredictable and may yield some ground, there are no guarantees negotiations will deliver a favorable outcome. South Africa, which has the continent’s biggest economy and a fraught relationship with the Trump administration, is bracing for the worst. It shipped more than $4 billion’s worth of Mercedes-Benzes, oranges and other goods to the US last year that qualified for preferential access under AGOA. President Cyril Ramaphosa struck a resigned tone in his weekly newsletter, warning that steps must be taken to protect existing jobs from the fallout of the trade war, which has already hammered vehicle shipments. “The need to diversify our export base has become all the greater,” he wrote. With so much at stake, the next few weeks will be crucial. — Alexander Parker Key stories and opinion:

Big Take: Trump’s Tariffs Are Already Stunting Global Growth

Trump Tariffs to Supersede US Congress-Backed Africa Trade Pact

Dire Situation in Lesotho Even Before Trump’s 50% Levy Starts

Where Does President Trump’s Tariff Campaign Stand?: QuickTake

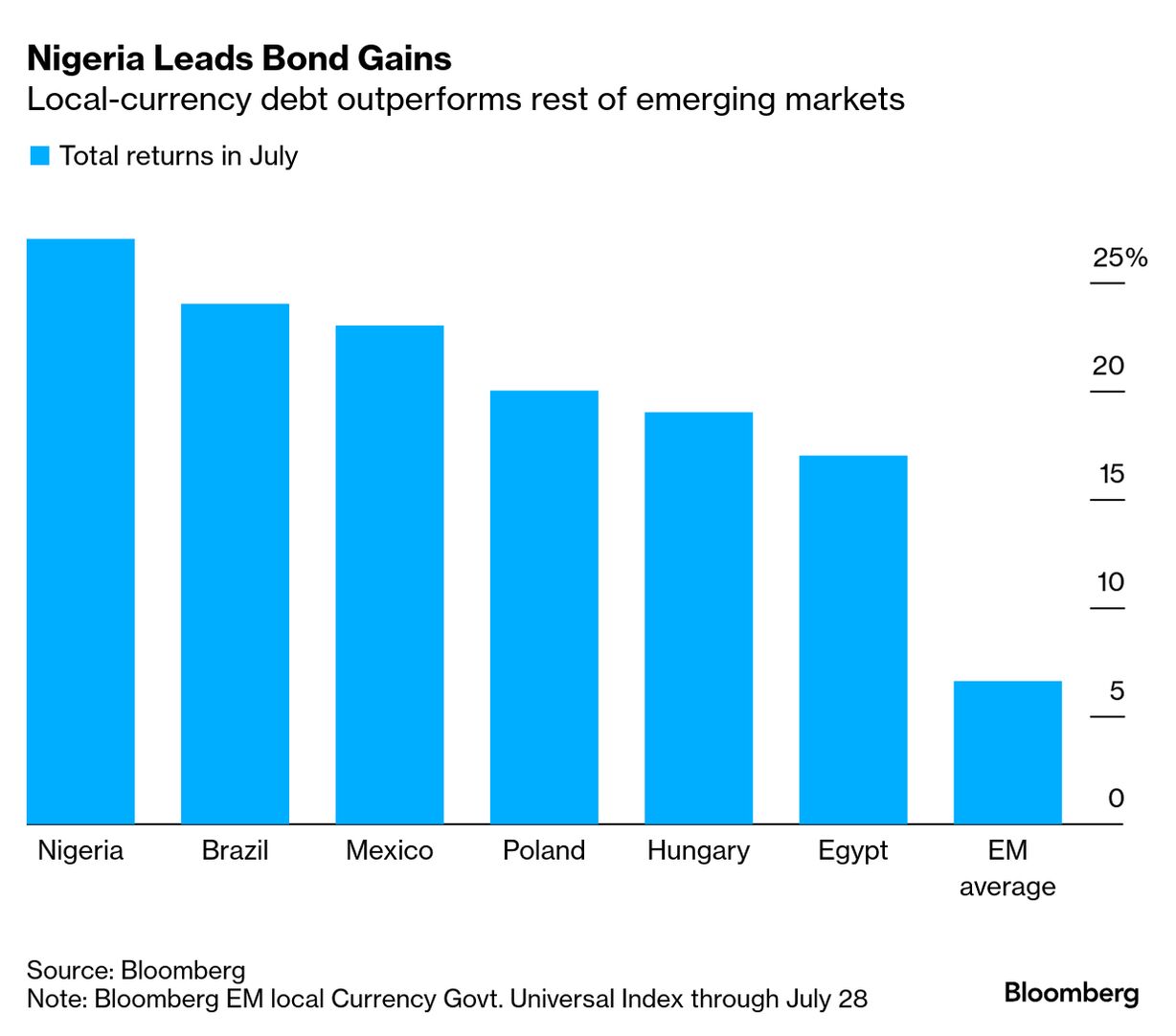

America’s Africa Policy Is Clear. Success Isn’t: Justice Malala At least three people were reported to have been killed in unrest linked to a taxi strike in Angola, which continued for a second day on Tuesday. Banks and the country’s biggest shopping mall closed their doors. The government reported more than 100 arrests in connection with disturbances sparked by protests over a surge in fuel prices after the oil-producing southwest African nation scrapped subsidies.  Minibus drivers in Luanda, Angola’s capital. Photographer: Osvaldo Silva/AFP/Getty Images Uganda’s coffee earnings more than doubled to a record in the past 12 months, buoyed by rising global prices and a push to increase production. The authorities have been trying to bolster the output of beans for the past decade, handing out seedlings and allocating funds to rehabilitate trees and train farmers — an effort that’s starting to pay off. The nation’s coffee industry, Africa’s biggest, contributed $2.22 billion to state coffers in the year through June. Helios Investment Partners, an Africa-focused private-equity firm, plans to boost investment to capitalize on surging demand from the continent’s youth using mobile phones to watch sports matches and concerts. With 40% of the population under 15, the region is ripe for investment, Tope Lawani, the firm’s founder and managing partner, said in an interview.  An image of football player Mohamed Salah on a street vendor’s cart in Cairo. Photographer: Islam Safwat/Bloomberg Namibia plans to expand its capital markets by introducing new investment instruments, increasing local listings and improving financial-market infrastructure. The initiatives, outlined in a new 10-year plan, are aimed at boosting the number of registered investors by 70%, and raising the value of listed assets. Meanwhile, the southern African nation appears to be moving closer to reaping the benefits of a long-awaited oil boom, writes Bloomberg columnist Javier Blas. Oscar-winning director Christopher Nolan’s upcoming movie is sparking controversy in North Africa, with the shooting of some scenes in a disputed territory incurring the ire of a rebel group fighting for independence. Nolan, who won Academy Awards for Oppenheimer in 2024, chose to film parts of The Odyssey in the desert landscape near Dakhla, an Atlantic city in Western Sahara. Trump recognized Moroccan rule of the area in 2020, opening up a wave of investment.  An aerial view of Dakhla. Photographer: benkrut/iStockphoto/Getty Images Sun King, the world’s largest off-grid solar company, secured a $156 million financing package backed by Citigroup and other funders to boost access to affordable power in Kenya. “This deal signals a major turning point for green-energy finance in Africa,” said Anish Thakkar, Sun King’s co-founder. The firm estimates the funding will enable it to bring electricity to 1.4 million low-income households and businesses. Thank you for your responses to our weekly Next Africa Quiz and congratulations to Sandeep Jain, who was first to identify South Africa as the African nation whose main stock index went through the 100,000 mark for the first time last week. Nigerian President Bola Tinubu’s economic reforms are sparking the biggest bond rally in major emerging markets, with naira-denominated securities extending their 2025 surge. Since coming to power in May 2023, Tinubu has eliminated fuel subsidies and overhauled the tax system, while the central bank has allowed the naira to trade more freely. The measures have helped reduce the fiscal deficit, boost reserves and maintain a current-account surplus, but have added to a cost-of-living crisis. Thanks for reading. We’ll be back in your inbox with the next edition on Friday. Send any feedback to mcohen21@bloomberg.net |