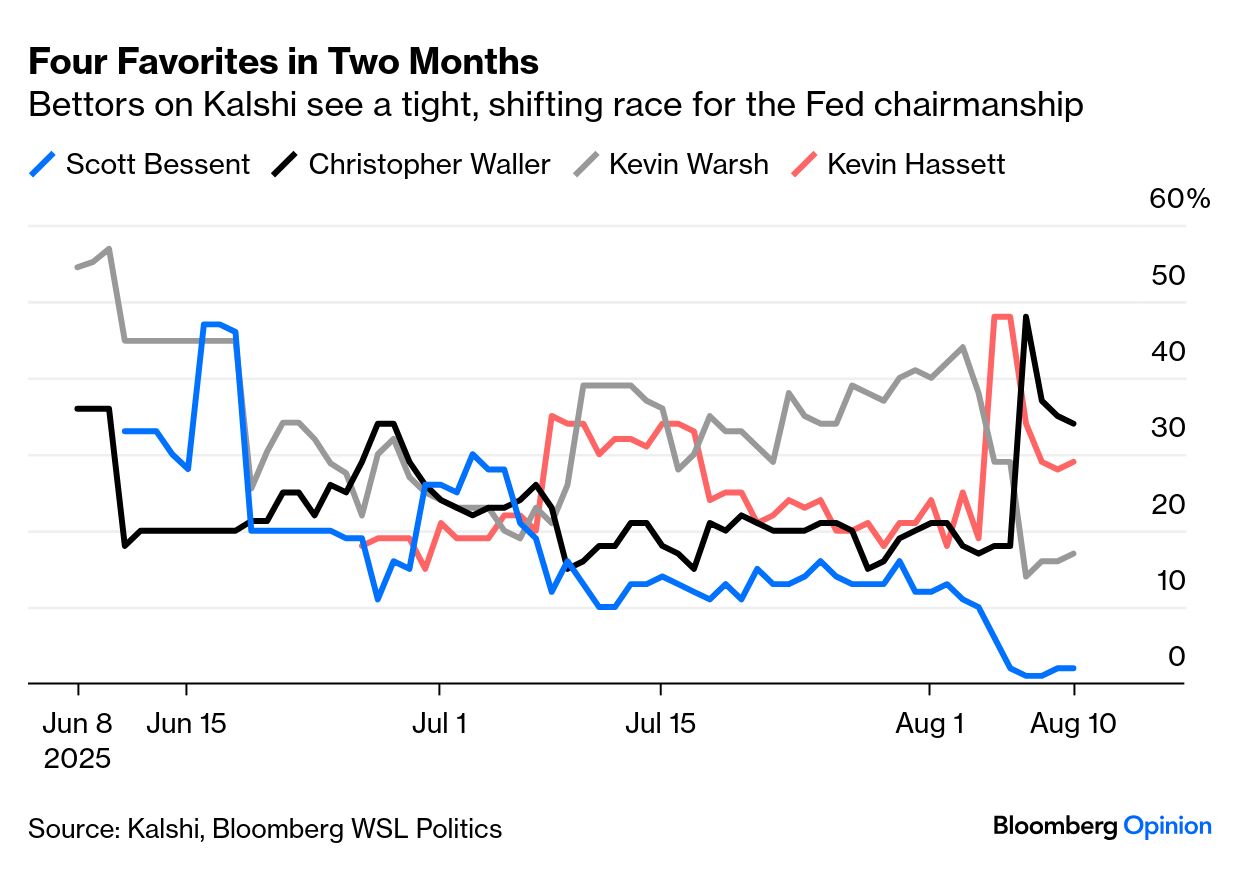

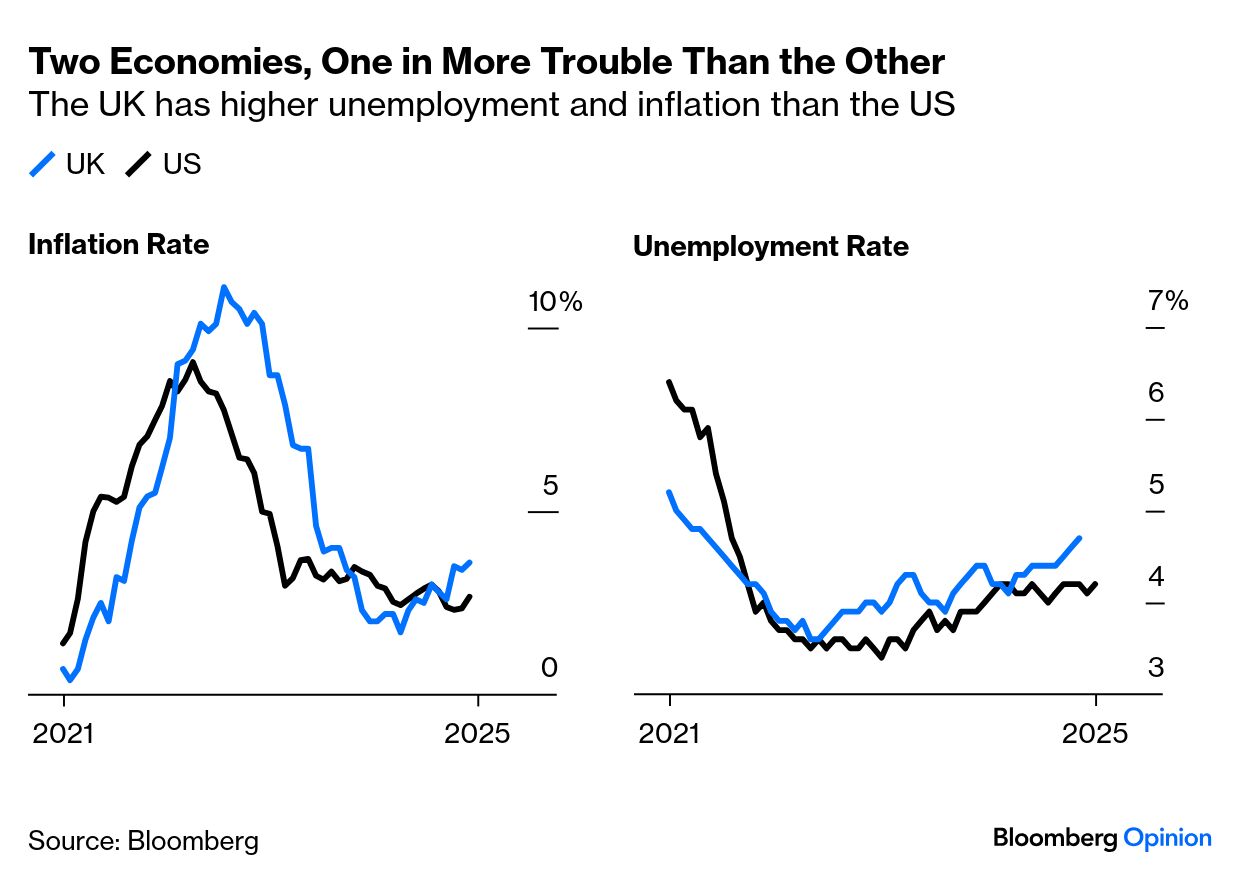

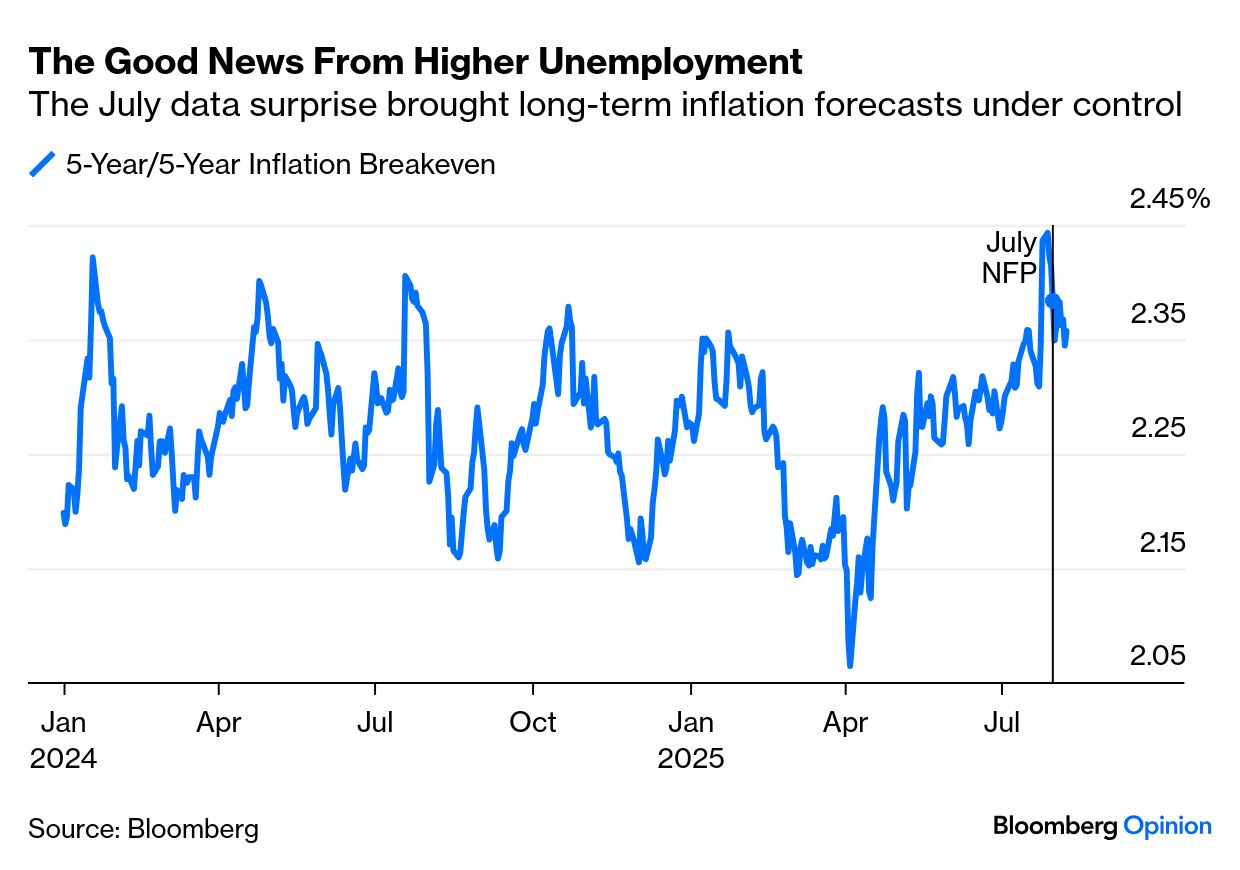

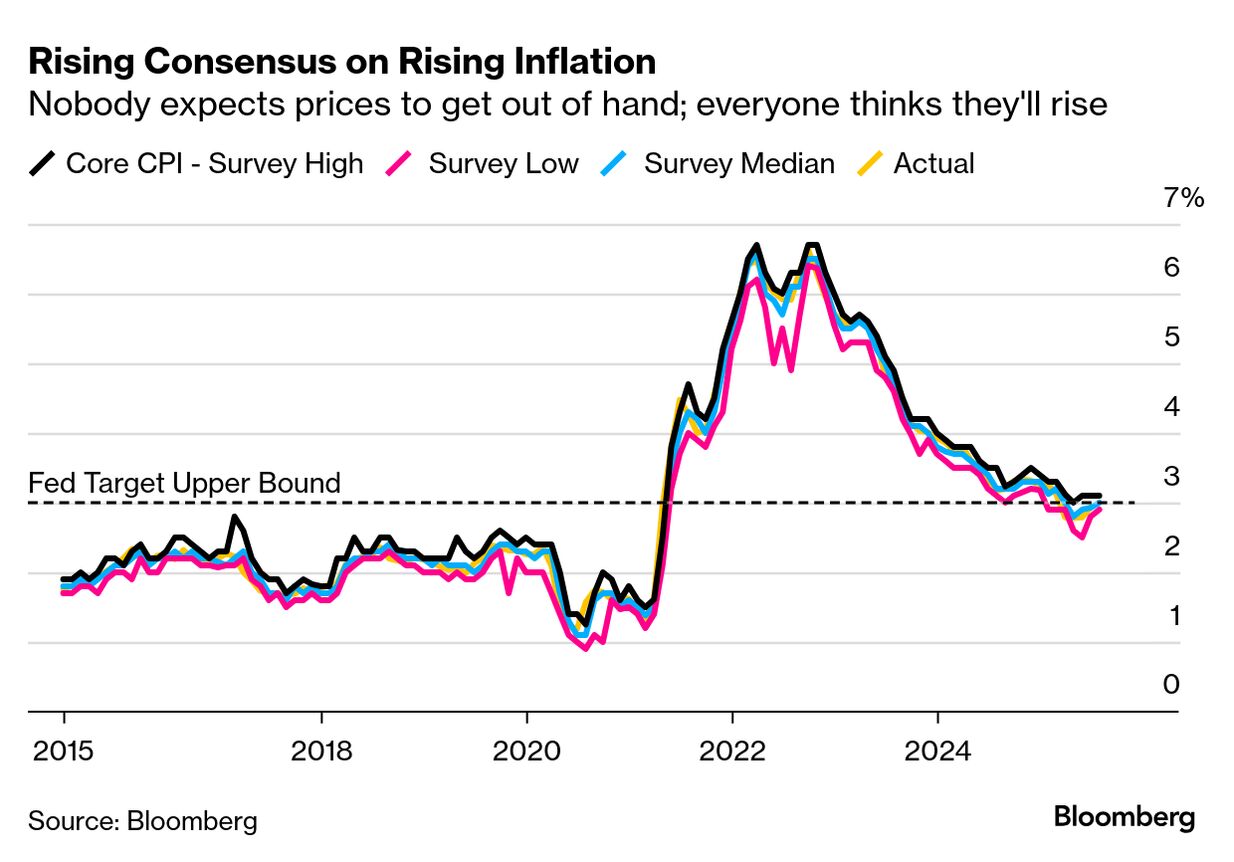

| Stephen Miran, who has been nominated to serve as a Federal Reserve governor until the end of the year, is a placeholder. He isn’t a candidate for the chairmanship. which falls vacant next May. But as placeholders go, he’s a very interesting one, and not just for his authorship of a now-notorious “User’s Guide” to restructuring global trade that has guided US tariff policy. As chairman of President Donald Trump’s Council of Economic Advisers, Miran has shown great loyalty as a spokesman for tariff policy. That is doubtless his chief appeal. He can be expected to vote for a rate cut as soon as he can join the Federal Open Market Committee, along with the two Trump appointees who dissented by voting for a cut last month. He won’t have time to make any substantive difference, but his Manhattan Institute paper published last year calling to reform the Fed’s governance, and attacking the status quo for encouraging “groupthink,” suggests that pressure for radical change will intensify. The range of Miran’s proposals for the Fed is almost as breathtakingly ambitious as his plans for world trade, which involved charging foreigners a fee for investing in the US and a possible “Mar-a-Lago Accord” to coordinate a weakening of the dollar. Those plans have gone very quiet as the dollar has fallen on its own while bond investors have been restive. His ideas for the Fed center on “monetary federalism” with more power for the regional Fed presidents and less direct influence for the FOMC; and as they don’t involve dealing with other countries, they have a better chance of happening. Trump’s choice not to name a potential next chairman to the role suggests that he now accepts that displacing incumbent Jerome Powell would be an unnecessary risk. Instead, there is a race straight out of reality television, with four candidates taking a lead since June on the Kalshi prediction market: Everything will come to an Apprentice-like denouement when Trump makes his pick. After the shock of the Aug. 1 revisions to US unemployment data, showing far weaker employment than initially reported, this seems a recipe for uncertainty and upheaval. None of this is showing up in markets. To explain why, look at the Bank of England. The UK economy is in far worse shape than the US. Both unemployment and inflation are higher: It also boasts an almost comically divided Monetary Policy Committee at the BOE. Two dissents came as a shock at the Fed; such an outcome would have been an outbreak of harmony in Threadneedle Street. Last week’s MPC held two votes after the first resulted in a tie — four to hold, four to cut by 25 basis points, and one to cut by 50. Cutting by 25 basis points eventually won 5-4. This has had no appreciable impact on rate expectations. According to overnight index swaps, the projected Bank Rate for the end of this year has been more stable than fed funds, even though the Fed maintained unanimity until July: The UK experience reflects good economists grappling with an extremely difficult situation. The market view of their likely path has reflected traders’ attempts to wrestle with the same issues. Even though the Fed has been far more united and clear in its guidance, that has added up to a bumpier road — because of the imponderable effect of tariffs, the political uncertainties, and then the shocking payroll revision. Dissent is not in itself damaging. Miran will be a dove, but his vote won’t swing the committee, and the balance of evidence is in any case shifting toward the doves. The jobs revision brought inflation forecasts, a potential barrier to rate cuts, back into line: July’s consumer price inflation, due Tuesday, is the next potential impediment. Almost all economists surveyed by Bloomberg expect a rise to or slightly beyond the Fed’s 3% upper-bound target. Nobody expects much worse than that. These forecasts overlap with total confidence in a September Fed cut, with or without Miran: That helps explain the greatest reason why markets are treating the upheavals with equanimity: The numbers aren’t that bad, even after the jobs revision (equivalent to only about 0.15% of the US workforce). David Roberts, head of fixed income at Nedgroup Investments, offers some cold water: OK, so there were some downward revisions to prior numbers. The current figures were a rounding error below consensus. Average earnings exceeded expectations, the unemployment rate was unchanged, and those employed worked LONGER than normal. Sure, the numbers ain't great — it's in my interests as a bond guy to talk the economy down. But dire? Not even close.

Daniel Von Ahlen of TS Lombard says the US labor market is in “a low-hiring, low-firing equilibrium.” He adds that there has been no credit boom and no obvious macro malinvestment; private-sector balance sheets are in robust health and real incomes are growing too fast for a recession (even if they have moderated). On the stock market, near record highs, cyclicals are beating defensive stocks to a record extent, despite sluggish signals from Institute of Supply Managers data. “One interpretation is that they are being complacent,” says John Higgins of Capital Economics. “Another is that the economic outlook is better than the ISM surveys suggest.” Absent evidence to the contrary, the market will allow the turbulence at the Fed to continue without complaint. But everyone, not just Miran, should be aware that that could change if the economy unambiguously weakens. |