Hi readers,

In today’s newsletter, CoinDesk Indices’ Andy Baehr writes that the administration most supportive of crypto may have just highlighted the biggest barrier to crypto adoption: a retirement system where most participants never choose their investments at all.

Then, RDC’s Ankit Mehta says that depository receipts were the original form of tokenization and should be applied to tokenized infrastructure today to offer a scalable and legally sound foundation for modern equities.

Thanks for joining us. |

|

|

On August 7, the White House released an executive order directing the Labor Department, which regulates retirement investing, to accelerate access to alternative investments in employer-sponsored defined contribution (DC) retirement plans, such as 401k's. Alternative investments were defined to include private market investments, real estate, commodities, infrastructure projects, lifetime income strategies — and notably, "holdings in actively managed investment vehicles that are investing in digital assets." (Curiously, crypto was the only asset class where "actively managed" was specified versus the "direct or indirect" language used for everything else — a regulatory breadcrumb worth exploring.)

The crypto industry — at least its asset management segment — cheered this latest presidential order granting crypto managers access to a $12 trillion pool of very sticky U.S. investment money. CoinDesk's coverage included industry reactions like this from Bitwise's Matt Hougan: "This order isn't about the government saying 'crypto belongs in 401(k)s.' It's about the government getting out of the way and letting people make their own decisions." Herein lies the problem: most people who participate in 401k plans don't make their own decisions, or do so hastily. In fact, there is a law in place to make sure participants don't have to decide at all.

The Pension Protection Act of 2006 solved a thorny problem for employers: what to do when 401k participants don't choose their own investments. Previously, employers faced potential liability for any default investment that performed poorly. The act gives employers safe harbor protection if they make default elections a "Qualified Default Investment Alternative" (QDIA) — usually a target-date or balanced fund. HR departments no longer had to worry about being sued for picking the "wrong" default option.

While this solved the employer liability problem, it created an opportunity for folks to neglect one of the most important investment decisions of their lives. Participants typically join their 401k during the chaos of starting a new job — dealing with health insurance, taxes, onboarding and actually learning the job. Faced with investment choices they don't understand, many simply go with the flow and accept whatever default option their employer has selected, often a target-date fund with a retirement date that roughly matches their age. The glidepath concept — automatically shifting from stocks to bonds as retirement approaches — creates a false sense of security. Participants assume they're "all set" simply by not opting out, and never revisit the decision. Years or decades may pass.

Vanguard's 2025 "How America Saves" report reveals the remarkable stickiness of defaults: 61% of plans now offer automatic enrollment, achieving 94% participation rates versus just 64% for voluntary enrollment. Nearly all auto-enrollment plans designate target-date funds as their default, and among plans with qualified default investment alternatives, 98% use target-date funds. The result? A stunning 84% of participants use target-date funds, with 64% of all contributions flowing into them — up from just 46% in 2015. Most telling of all: 71% of target-date investors hold only a single target-date fund, and only 1% of these "pure" investors made any trades in 2024, demonstrating how powerfully defaults shape behavior.

So, why not include digital asset allocations or strategies in target-date funds or other QDIAs, providing access to the broadest set of DC plan participants? The incentives don't seem to be there. Participants, employers, target-date fund managers and DC recordkeepers all have limited incentives to change the status quo. Every layer of this system benefits from accumulating and retaining assets. Fund managers might have incentives to introduce new, potentially higher-returning or better-diversifying investment types, but they must navigate through multiple gatekeepers to reach investors who may never even look at their choices. And employers certainly won't advocate for change.

The irony is rich: the system designed to democratize retirement savings has democratized not choosing at all.

Of course, some employees care deeply about DC plan investment options and will demand that their employers add choices for alternatives and crypto. We're not worried about those folks — they will find a way — but they are in the minority. The fallacy lies in assuming that all young workers, or any demographic group, would uniformly embrace crypto access in their 401k plans. The reality is that most participants across all age groups operate on autopilot. If digital assets log more years as being among the highest performing asset classes, it will be a shame if the vast majority of 401k participants who make default elections won't come along for the ride.

|

- Andy Baehr, head of product and research, CoinDesk Indices |

|

|

Tokenized Equities Need an ADR Structure to Protect Investors |

Tokenization has significant potential to transform capital markets, promising real-time settlement, broader investor access and greater programmability across financial infrastructure. But while the rails are evolving, current models for tokenized equities remain fragmented, opaque and misaligned with the safeguards that define the traditional securities markets. Today, two dominant approaches exist:

The wrapper model involves tokenized IOUs that provide synthetic exposure to existing equities rather than direct ownership. These tokens do not grant holders any governance rights or enforceable claims to the underlying shares. Transferability is typically restricted to closed ecosystems, liquidity is siloed across issuer-controlled platforms and regulation can be murky, with many products not available to U.S. persons.

The on-chain issuance model means creating a native digital share class issued via blockchain. While this approach aligns more closely with the legal definition of security, it introduces operational complexities and scalability challenges. Active issuer participation is mandatory, liquidity remains fragmented between the on-chain tokens and traditional securities and broker-dealer standards are inconsistent, complicating participation for regulated financial institutions and investors.

What’s missing is a tokenization model that combines the speed, accessibility and composability of tokenization with the structure, safeguards and clarity of traditional capital markets. Fortunately, that model already exists elsewhere: depository receipts (DRs).

In many ways, DRs were the original form of tokenization. For over a century, American depository receipts (ADRs) have enabled foreign equities to trade in the U.S. through a regulated, custody-backed structure. Today, this framework can also bridge traditional securities with tokenized infrastructure, offering a scalable and legally sound foundation for modern equities. The case for tokenized DRs By combining blockchain rails with the legal and operational framework of DRs, market participants can unlock broader participation and real-time asset servicing without compromising on investor protections or operational standards. Other benefits include: |

- Preservation of shareholder rights

|

Unlike synthetic wrappers, the ADR structure perfects shareholder rights, enabling them to be passed along to token holders. This includes economic entities, such as dividends and other corporate actions, as well as governance rights such as voting. |

- Clear segregation of duties

|

A regulated custodian bank safekeeps the underlying shares in a segregated, bankruptcy-remote structure, held solely for the benefit of ADR holders. An independent, market-neutral depositary facilitates DR issuances and cancellations, maintains accurate records using an SEC-registered transfer agent and performs daily reconciliation with the underlying assets. The depositary has no ownership claim on the underlying shares themselves. |

ADRs are recognized as securities under U.S. law. For years, they have been used to allow U.S. investors to own and trade foreign shares in the U.S. markets. Furthermore, the receipt structure has been flexible to enable fractionalization of U.S. preferred shares. With regards to tokenized securities, Commissioner Hester Peirce in her latest statement on tokenization mentioned that “a token could be a receipt for a security.”

|

- Full fungibility and market access

|

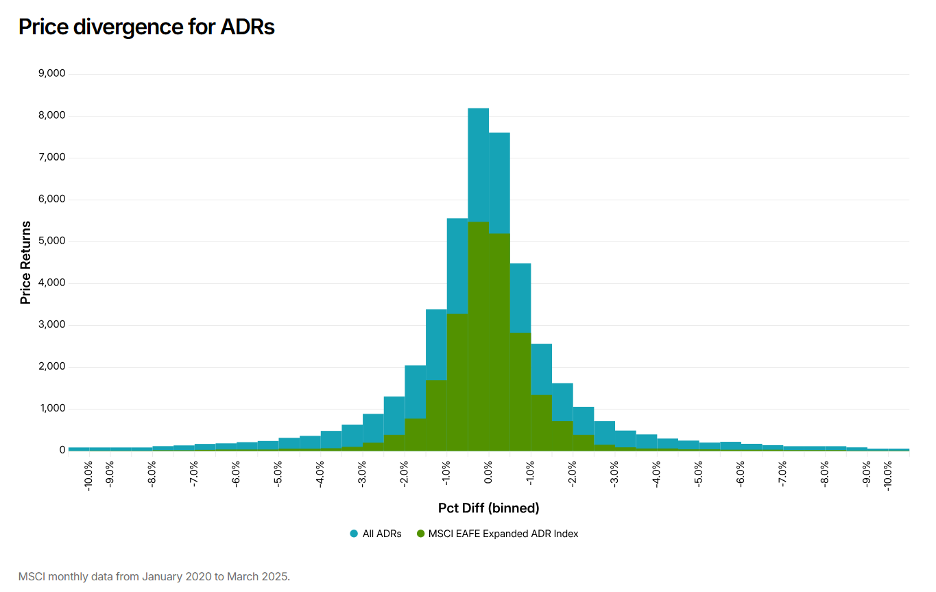

ADRs are fully fungible and redeemable for their underlying shares, enabling same-day, non-taxable conversions. They can be made available to both retail and institutional market participants who can choose to hold securities in tokenized or traditional form without sacrificing rights or liquidity. The fungibility of ADRs is supported by analysis from MSCI, which indicates that, on average, ADRs trade at parity with their underlying local shares.

|

ADRs can be deployed by both stock issuers and secondary market participants, enhancing scalability and adoption — unlike on-chain issuance models reliant on issuer initiation and active maintenance.

A trusted mechanism for bridging markets Proven and fully integrated into global finance, applying the ADR structure to tokenized equities is a logical evolution.

As tokenization matures, this kind of innovation is critical to scaling adoption and trust. Just as SEC Rule 12g3-2(b) streamlined access to foreign issuers, a similar regulatory mechanism could unlock broader tokenized equity markets, enabling public companies to offer tokenized shares to U.S. investors in a compliant manner.

The path forward doesn’t require inventing a new wrapper — it requires adapting a proven one. In other words, the bridge between traditional finance and digital infrastructure already exists. It just needs to be thoughtfully crossed. |

- Ankit Mehta, co-founder and CEO, Receipts Depositary Corporation (RDC)

|

|

|

Crypto's Most Influential Event returns in 2026.

Dealmaking. Networking. Big moves. Consensus 2026 is where the industry’s top players connect, innovate, and build what’s next.

Register early to lock down our best deal. |

|

|

|