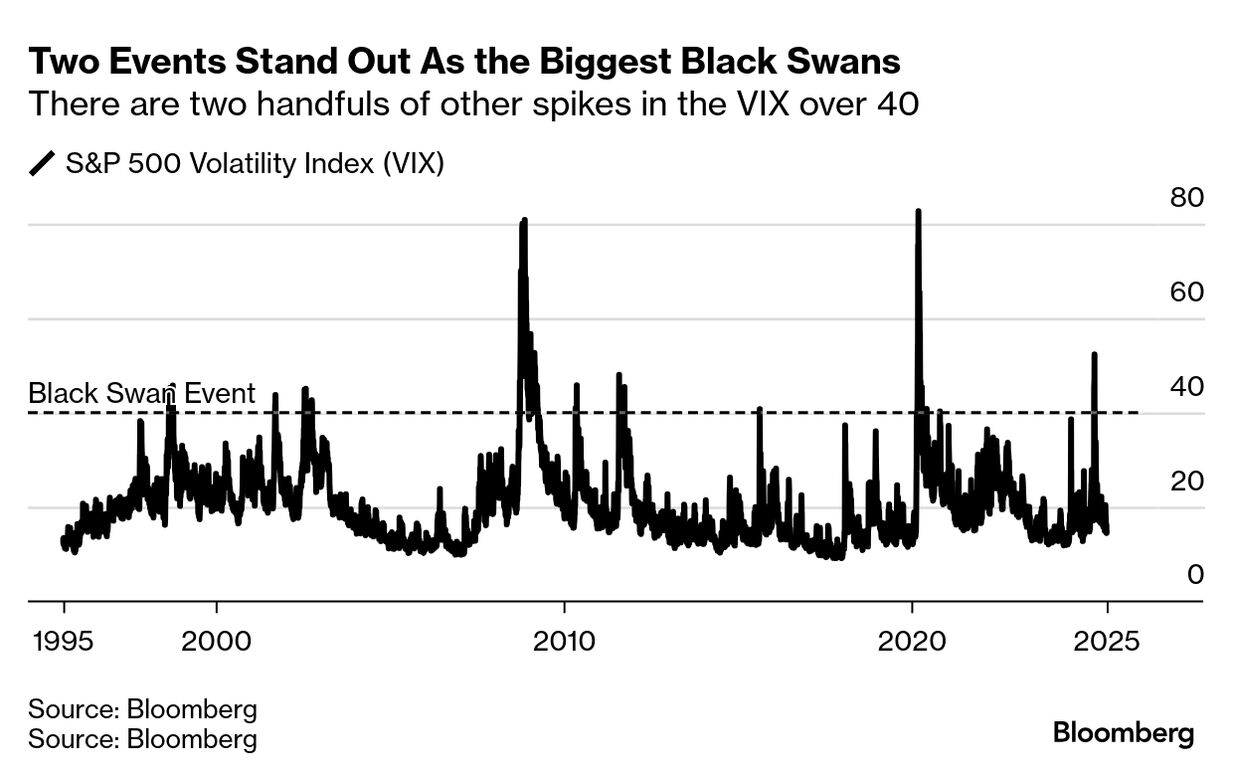

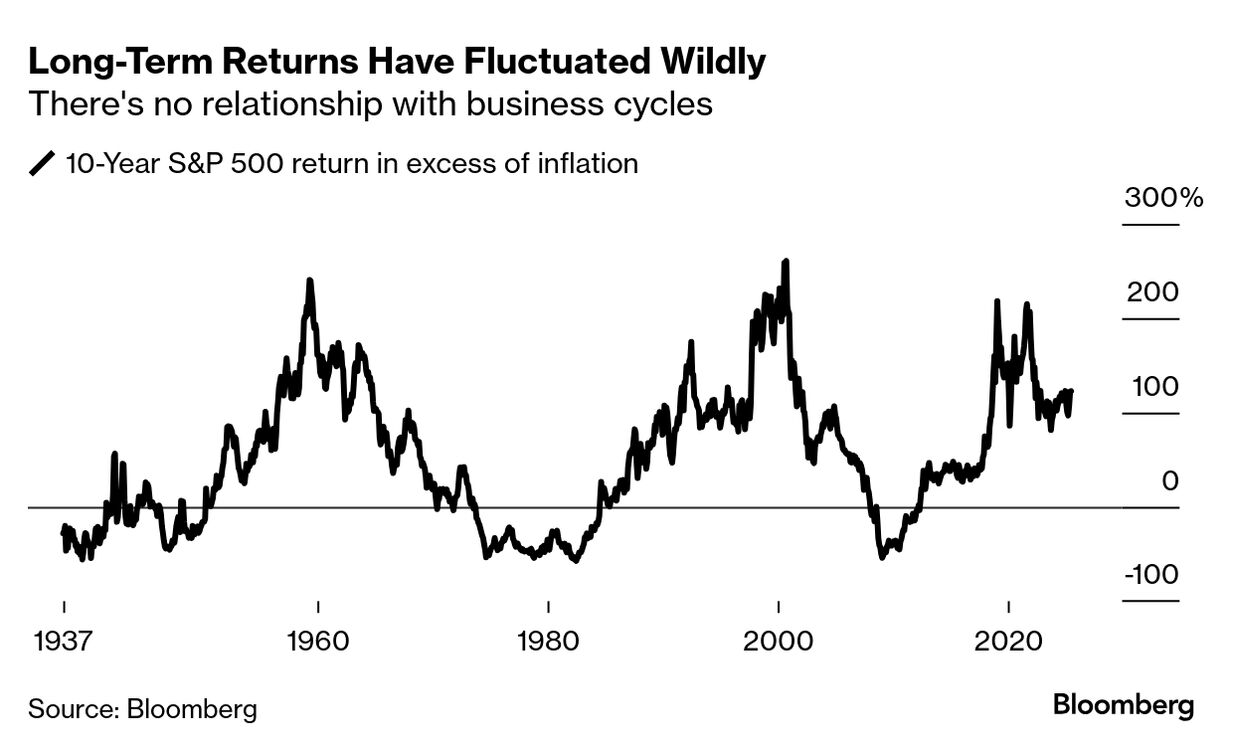

| There are a few conclusions here. First, the 10-year return chart is also further reason to ignore “Black Swan” risk unless it shakes the economy for a good while. There’s no correlation to the aforementioned volatility spikes. When the VIX spiked in 2008, inflation-adjusted 10-year returns were headed down. By contrast, 10-year returns were high in 2000 and in March 2020. The brief recession knocked stocks off their perch, but fiscal (and monetary) stimulus soon propelled them to new all-time highs. It's the business cycle that matters, not event risk. Second, if you’ve got a very long time horizon, you’re probably okay sticking with buy-and-hold even through economic downturns. Over a decade, returns can sometimes look awful. But over the very longest periods, things look better. Third — and I think this is where I get into the ‘alternative’ interpretation below — the increase in 30-year returns across business cycles since 2000 looks totally unsustainable. We hit a high in December of 30-year inflation-adjusted returns of 529%. That’s 6.6% a year for 30-years. That leaves me a bit uncomfortable. Some alternative ‘Minskyian’ thoughts to buy-and-hold | What 2008 taught us, summing up the work of the late economist Hyman Minsky, is that stability breeds instability. Humans are prone to pushing the limit. So whenever we individually or collectively get comfortable with any situation, we add a little risk on top! Just look at the recent China tariff policy. That increased risk can crystallize in big losses. I look at the 25-year increase in very long-term equity returns the same way — as a de-facto sign that more risk is being taken. We just don’t know how yet. what got us here is that after the dot-com crash, a lot of people felt burned by active fund managers who had just eviscerated their investment nest eggs. They sought solace in the safety of buy-and-hold: so-called passive investing. This trend got more popular after the Great Financial Crisis and then after the pandemic plunge in 2020. By the end of last year, investors deploying that strategy saw a record inflation-adjusted return for all periods going back to 1962. Herein lies the problem. It’s not just the very high long-term 30-year return. The stability of the last 16 years — with only the briefest of downturns — has caused stocks to reach heights that simply make them vulnerable. That’s what famed investor Howard Marks says. When you look at valuation too, whether it’s the price-to-earnings or price-to-book ratio, we are now at some of the highest levels in history. It feels like hedging the risk during the next downturn rather than blindly buying the dip makes the most sense. The very success of the buy-and-hold strategy has landed us in a place where buying a seemingly diversified S&P 500 index is in many ways a concentrated bet on the biggest technology stocks. Yes, they’re money-earning machines. But there’s a risk like during the Internet Bubble, where if technology falls, everything falls. For me, it’s worrying that just seven companies make up almost 40% of the S&P 500, such that when they put out poor results — as they eventually will — the selling of index funds will send the whole market crashing down. All I know is that when the economy does turn down and Big Tech stocks follow, lightening up on their weight in my portfolio and expecting new market leadership will certainly help me sleep better at night. |