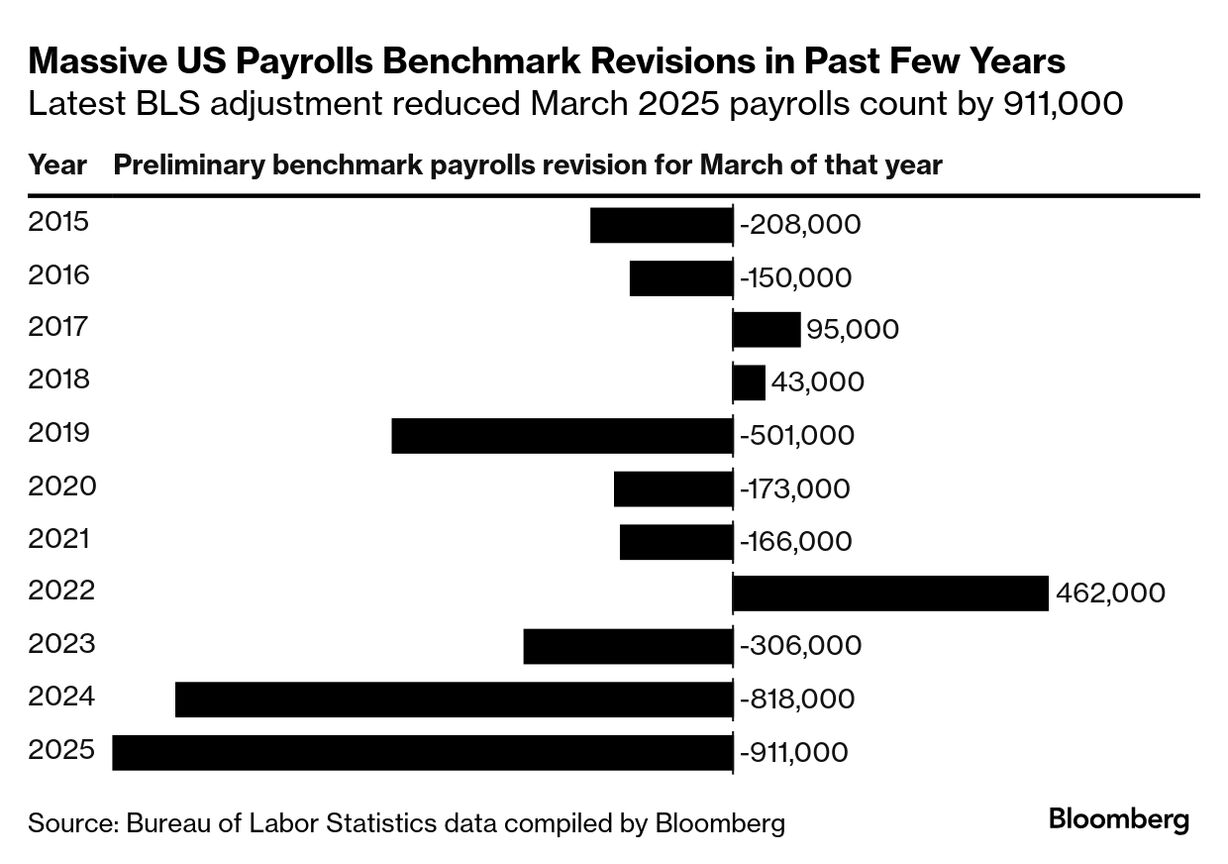

| For the Trump administration, today’s massive revision to US jobs numbers was vindication of the president’s attacks on both government data and the Federal Reserve. The White House called the widely anticipated downward revision by the beleaguered Bureau of Labor Statistics “another blunder in the lengthy history of inaccuracies and incompetence” at the agency and said it showed that President Donald Trump is right in saying the Fed’s been too slow to cut interest rates. The figures were striking. The BLS marked down the number of jobs added to the economy in the 12 months ending in March by 911,000 — a record. That suggests that the monthly pace of job growth, on average, was roughly half of what had been initially reported. Final numbers are due early next year. Trump fired the head of the BLS in August after similarly large downward revisions in monthly jobs data. His nominee to step into the role, EJ Antoni, chief economist at the Heritage Foundation, is awaiting a Senate confirmation hearing. And it’s not just a matter of filling the top job at the BLS. A third of high-level positions at the agency are vacant. The BLS has been laboring under declining inflation-adjusted funding for years, as well. (Although BLS budget woes predate Trump, other government data collection, from tracking infectious diseases to weather and climate statistics, is under stress from the president’s efforts to downsize the government.) The administration so far hasn’t outlined a specific plan as to how to fix the “broken” BLS, a characterization that many economists and statisticians dispute. Revisions to jobs data — which occur in both monthly reports as well as annually — are routine. The annual revisions benchmark the figures to more complete information from unemployment insurance tax records. Those are more accurate but less timely. The biggest preliminary downward revision before today occurred in 2024, during the Biden administration. Beyond the political impact, the new data gives another reason for the Fed to cut interest rates — already widely expected to happen at next week’s meeting. “The revisions make clear that the Fed’s monetary policy is far too restrictive and interest rates remain too high,” the White House statement said. — Molly Smith |