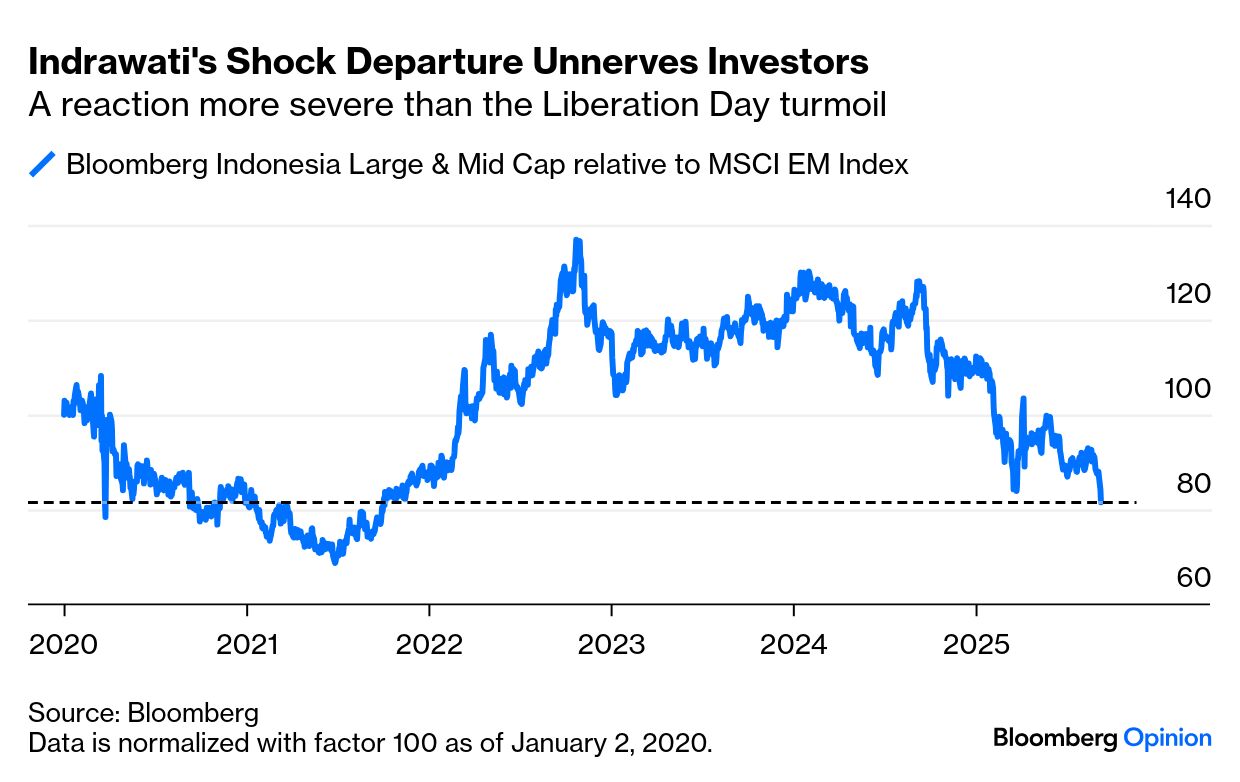

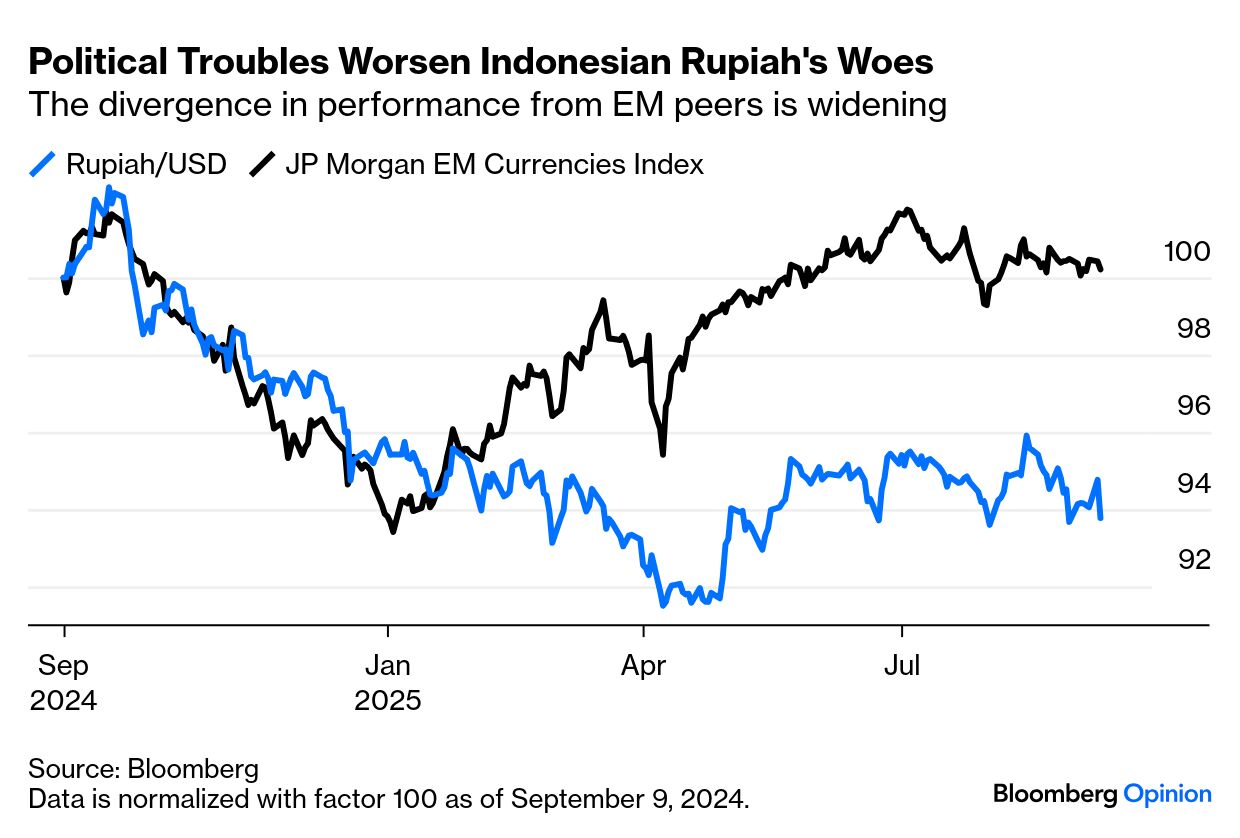

| For the Indonesians protesting harsh economic conditions, President Prabowo Subianto’s decision to part ways with respected Finance Minister Sri Mulyani Indrawati is a big deal. But what may count as a victory for the thousands who took to the streets offers little reassurance to investors. Prabowo’s decisive victory last year was fueled by populist ideals. Few would have predicted such a swift and widespread eruption of public discontent. Indrawati’s abrupt dismissal adds to the strain already imposed by President Donald Trump’s punitive tariffs on Indonesia’s export-dependent economy. But unlike the slower-burning impact of trade barriers, her exit sent an immediate jolt through the markets. The country’s stocks now lag emerging-market peers to a degree not seen since 2021 — worse even than the sharp decline on “Liberation Day:” Why did Indrawati’s departure take investors aback? Bloomberg Economics’ Tamara Mast Henderson explains that the point of contention between Prabowo and his former finance minister appears have been the degree of fiscal restraint amid protests about the cost of living and inequality. Now, it’s highly uncertain if the government will maintain fiscal prudence, especially as her successor, Purbaya Yudhi Sadewa, indicated the president would push for faster growth as quickly as possible: With Indrawati out, the key question is whether Prabowo intends to push through legislation to lift the budget-deficit limit, currently set at 3% of GDP. This limit has kept government debt in check and well within the standard 60% benchmark for debt sustainability.

Meanwhile, the country’s currency slid as much as 1.2% against the dollar, its steepest drop since December. It has parted company with emerging-market peers this year: Beyond the political upheaval, investors are also rattled by the perceived erosion of Indonesia’s central bank independence. A week ago, Governor Perry Warjiyo said that Bank Indonesia was helping Prabowo fund his priority projects by sharing some of the interest it earns on government bonds and buying debt in the secondary market. This involves, in part, increasing the interest paid on government deposits held at the central bank. Capital Economics’ Jason Tuvey adds that, in return, BI will share the interest costs associated with Prabowo’s housing and village cooperative programs. However well-intentioned such partnerships may seem, Tuvey warns that loss of central bank independence in other emerging markets has tended to fuel inflation and raise inflation expectations. Indrawati’s departure increases the suspicions that the government will step up pressure on BI to cut interest rates more aggressively. It has already eased by more than a percentage point since the policy rate peaked last year. Fed cuts might make it easier for this to continue: Still, Tuvey notes that he would probably need to see signs of more overt government pressure on the central bank before altering his forecast: This could take many forms, including calls from government officials for BI to lower interest rates faster and, potentially, moves to enable BI to purchase government debt on the primary market. Any changes to leadership at the central bank could be a signal that the government is trying to exert greater influence over BI’s policies.

Emerging markets are gaining credibility as alternative investment destinations, but political risk, a long-standing concern, remains a potent threat in South-East Asia. Thailand has also had its fair share of political upheavals. Such countries haven’t decoupled from the global economy — and a rate cut from the Fed would help them a lot.

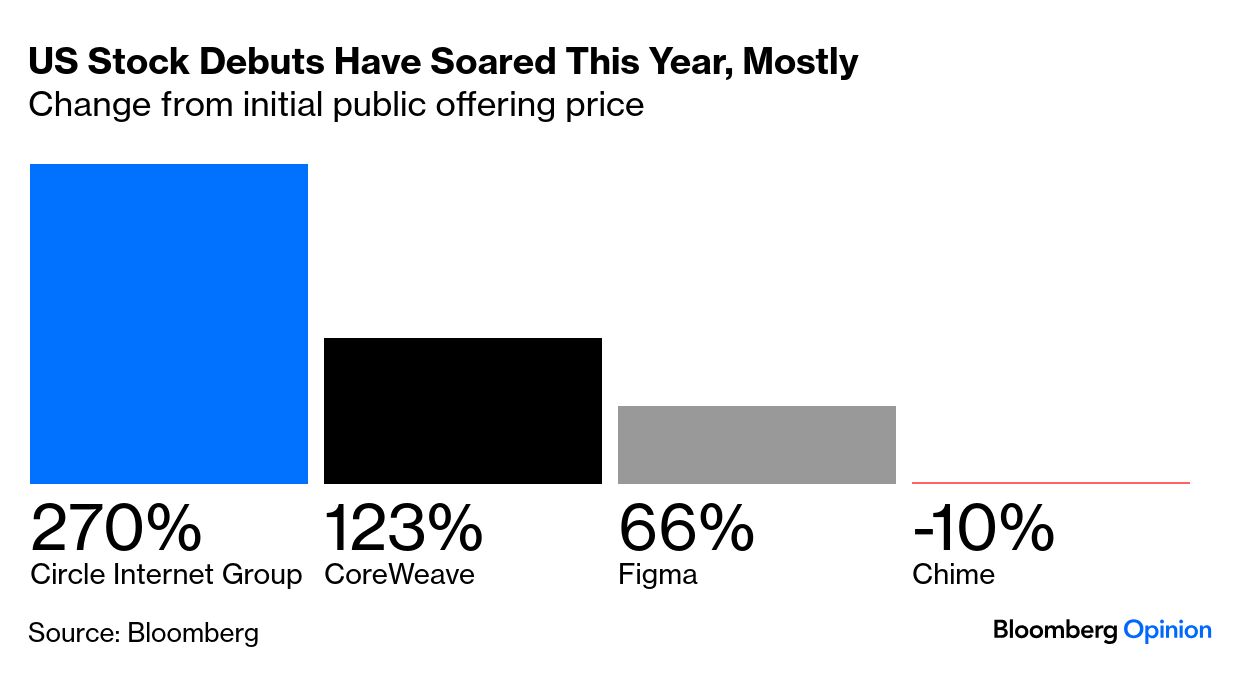

-- Richard Abbey Klarna Group Plc’s long-awaited initial public offering priced Tuesday. Valued at about $15 billion, it’s well below the $45 billion mooted for the Swedish buy-now-pay-later (BNPL) lending group at the height of the pandemic, but the debut was oversubscribed and suggests that a niche area of consumer finance is building a following. BNPL companies allow consumers to spread the payment for goods and services over at least four equal installments, typically without interest. According to the Consumer Financial Protection Bureau, the six largest BNPL firms — Affirm, Afterpay, Klarna, PayPal, Sezzle, and Zip — extended nearly $34 billion in loans for merchandise purchases in 2022. The industry shows no sign of slowing, but remains tiny compared to over $18 trillion in US consumer debt. Klarna’s debut is an important milestone for a sector that faces intensified regulatory scrutiny. Four months ago, New York adopted a licensing regime for providers. Similarly, the UK unveiled reforms to its 50-year-old Consumer Credit Act, aiming to extend key safeguards to BNPL borrowers. While the valuation trails Affirm’s $24 billion 2021 debut, it’s going public in a subdued dealmaking environment. Likely rate cuts enhance the prospects for deals, and should provide relief for Klarna customers already burdened by relatively high rates. The next question, Bloomberg Opinion colleague Paul Davies notes, is whether it can follow in the footsteps of recent strong fintech stock debuts: The US consumer’s health remains questionable, as measures of delinquency weaken, while household debt soars. Unsurprisingly, BNPL companies face rising defaults. Klarna’s consumer credit losses in the first quarter were up 17% compared to the same period last year, totaling $136 million. They coincided with a surge in total loan volume and could widen further if the economy slows down. The fintech company would gain from monetary easing — somewhat. Given that most buy-now-pay-later transactions are interest free, the most plausible benefit lies not in reducing borrowing costs, but in fostering a sense of financial relief that expands consumers’ willingness to spend. Sydney-based Macquarie University published a paper on the psychology behind BNPL users’ behavior. It concluded that they perceived their purchases to be less expensive and felt less pain of payment when using BNPL. That led to more spending, and to buying more expensive items — which both buoys the economy in the short run and amplifies the risks. Despite this, Progressive Policy Institute's Andrew Fung argues that the relatively small scale of BNPL limits the chance of broader systemic failures. Rate cuts would also help shield consumers from further financial strain. That could prove a quiet boon for Klarna and — from today — its shareholders. -- Richard Abbey |