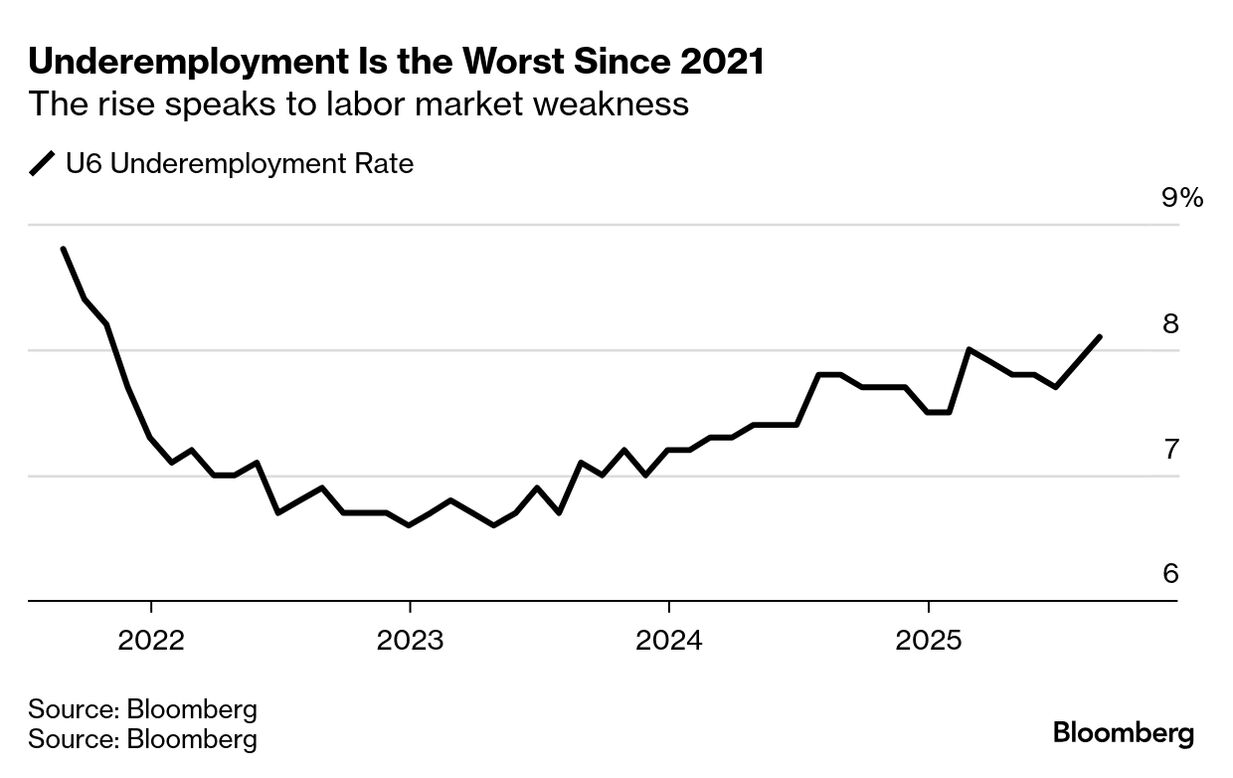

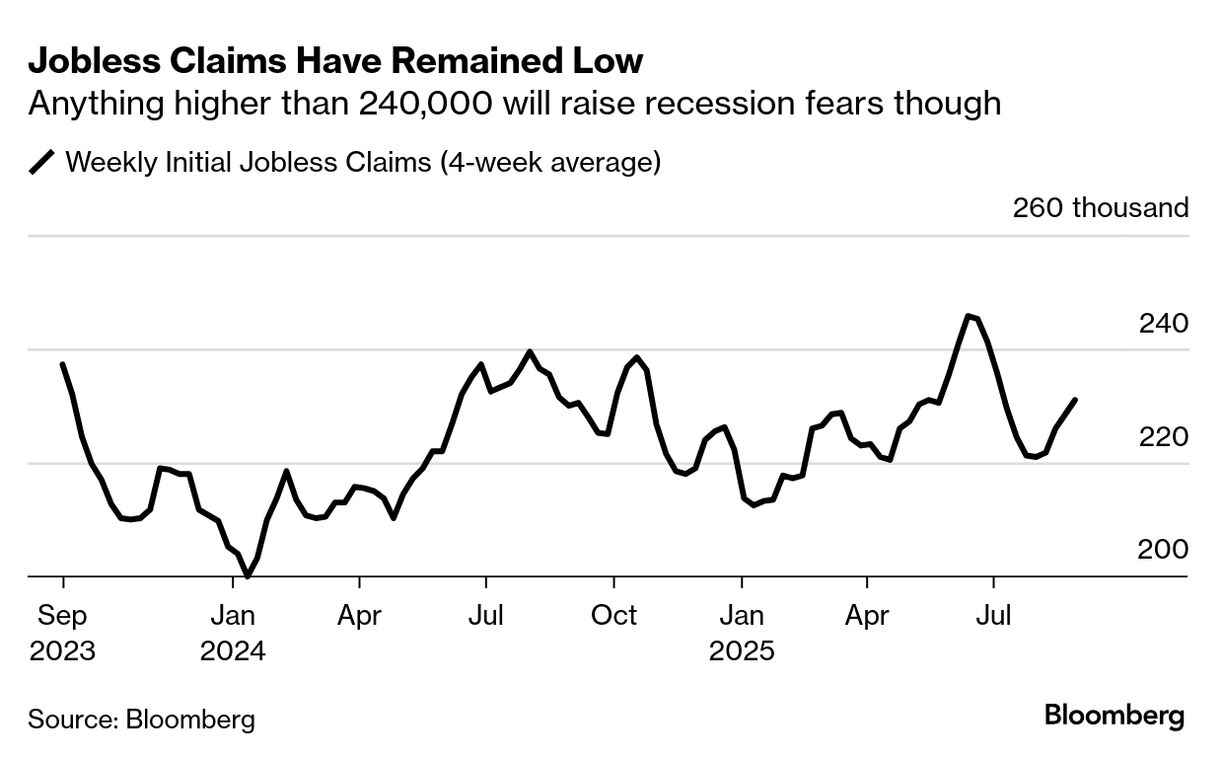

| How weak is the jobs market? The prevailing narrative — one supporting the rise in shares after a decent quarterly corporate earnings season — is that employment is weak but roughly in balance. As Fed Chair Jerome Powell outlined a few weeks ago, while job growth has slowed, firms aren’t firing people en masse. He added, though, that because supply and demand were lower, it means any weakness could unravel the balance more quickly. So the Fed is on the case. My concern is that the current reality may actually be worse. For example, the latest jobs report showed not only weak numbers for August, but also downward revisions to prior months, with the US economy losing jobs in June. What’s more, that report showed a more comprehensive unemployment figure — including those who are underemployed, marginally attached to the workforce or have given up looking for work — as rising to the highest level in four years. That measure is a full 1 ½ percentage points higher than at its trough. Add in Tuesday’s news of the biggest subtraction of job growth from any annual benchmark revision ever, and you get a labor market that is weaker than investors thought, perhaps much weaker. Markets are still in a rallying mood. But more weak employment figures could quickly change things. I’d look at weekly initial jobless claims of more than 240,000 as a threshold for where bad news is treated as bad news, and the market sells off. Risk of recession is not a problem. It’s a buy-the-dip opportunity | This isn’t cause for worry yet. Recession risk doesn’t seem particularly high yet. Polymarket pegs the chance of recession at a measly 8% before year-end. And my recent analysis shows that negative shifts in mood about equities don’t last long unless an actual recession comes. Whether its event risk or poor economic figures, time and again these have proven to be only temporary setbacks. To wit, JPMorgan’s trading desk warned of a pullback after a rate cut on Monday, pointing to a number of risk factors including inflation, employment and the trade war. Still, if you read their note, they also say “we maintain our lower conviction Tactical Bullish call. This current bull market feels unstoppable with new support forming as former tent poles weaken … Economic growth appears to be strengthening, earnings are robust, and the trade war has seen incremental improvement. ” In essence, buy the dip. Put all of this together, and given the low recession risk, it still makes sense to stay fully invested in the market. Recession risk that rises somewhat and triggers a drop in stock prices is essentially an opportunity in disguise. Moreover, we saw that a short recession in 2020 and a historically aggressive rate hike cycle in 2022 and 2023 didn’t keep the market down for long. That underpins investors’ buy-the-dip mentality. In fact, because so far we’ve overcome policy shifts by President Donald Trump that I’d call the biggest risk to the economy since 2009, there’s even greater incentive to double down on equities. The real risk? Experience from 2001 and 2007 shows that lengthy recessions and extreme overvaluation combine to be a wrecking ball to equity returns. On valuation, Bank of America recently surveyed fund managers and found that more than nine in 10 of them think US equities are overvalued. I argued a few weeks ago that means investors will likely sell at the first sign of trouble. That selling would continue if the risk of recession morphs into an actual recession. This expansion hinges on whether consumers can handle the impact of tariffs on inflation and on the ability of the AI boom to prop up capital spending and equity valuations. On the jobs numbers. it’s a short stone’s throw from fewer than 30,000 jobs being added to the economy to the economy actually losing jobs. And while Big Tech’s capital spending plans say this AI cycle can go on for a few more quarters, technology consultant Gartner’s view that we’re heading for a “Trough of Disillusionment by 2026” is a reality check on how long this boom can last. |