Points of Return

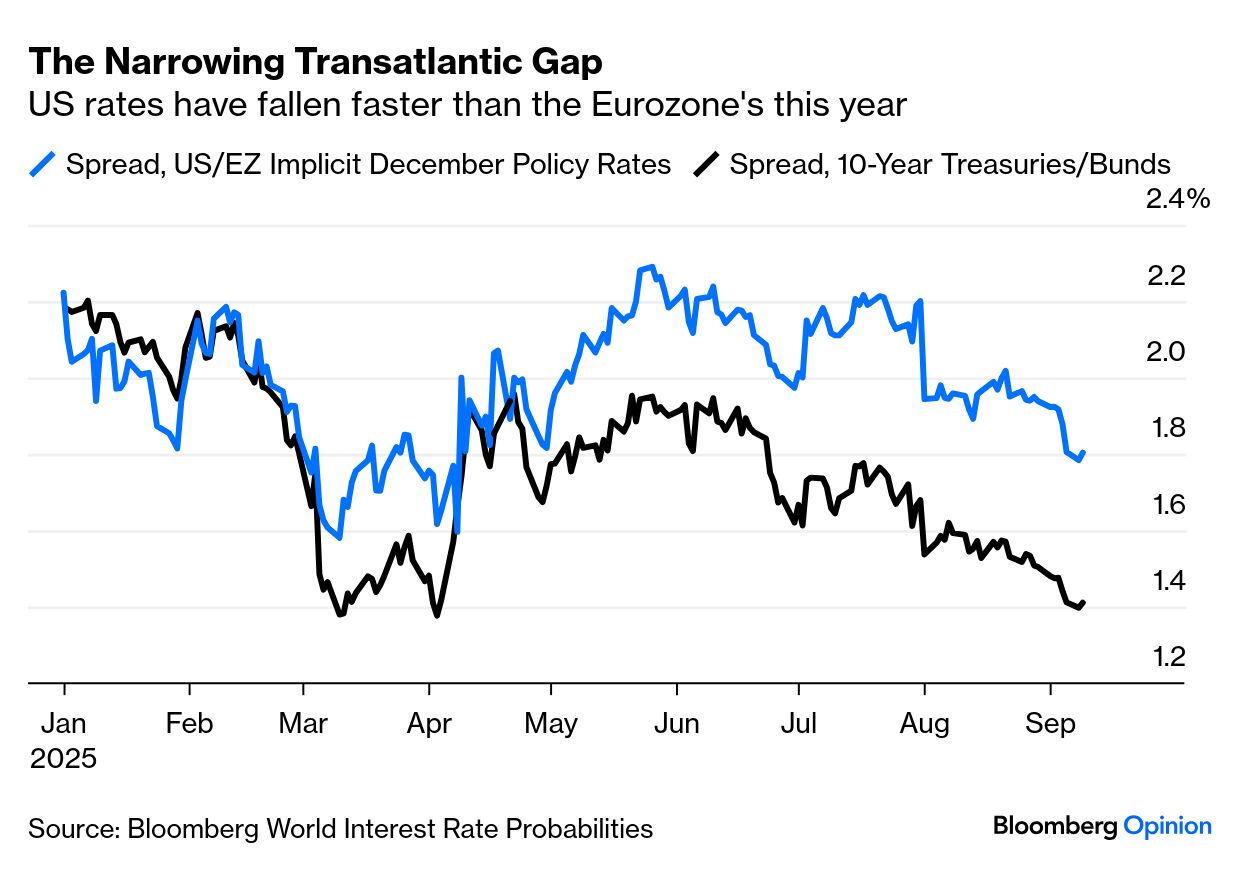

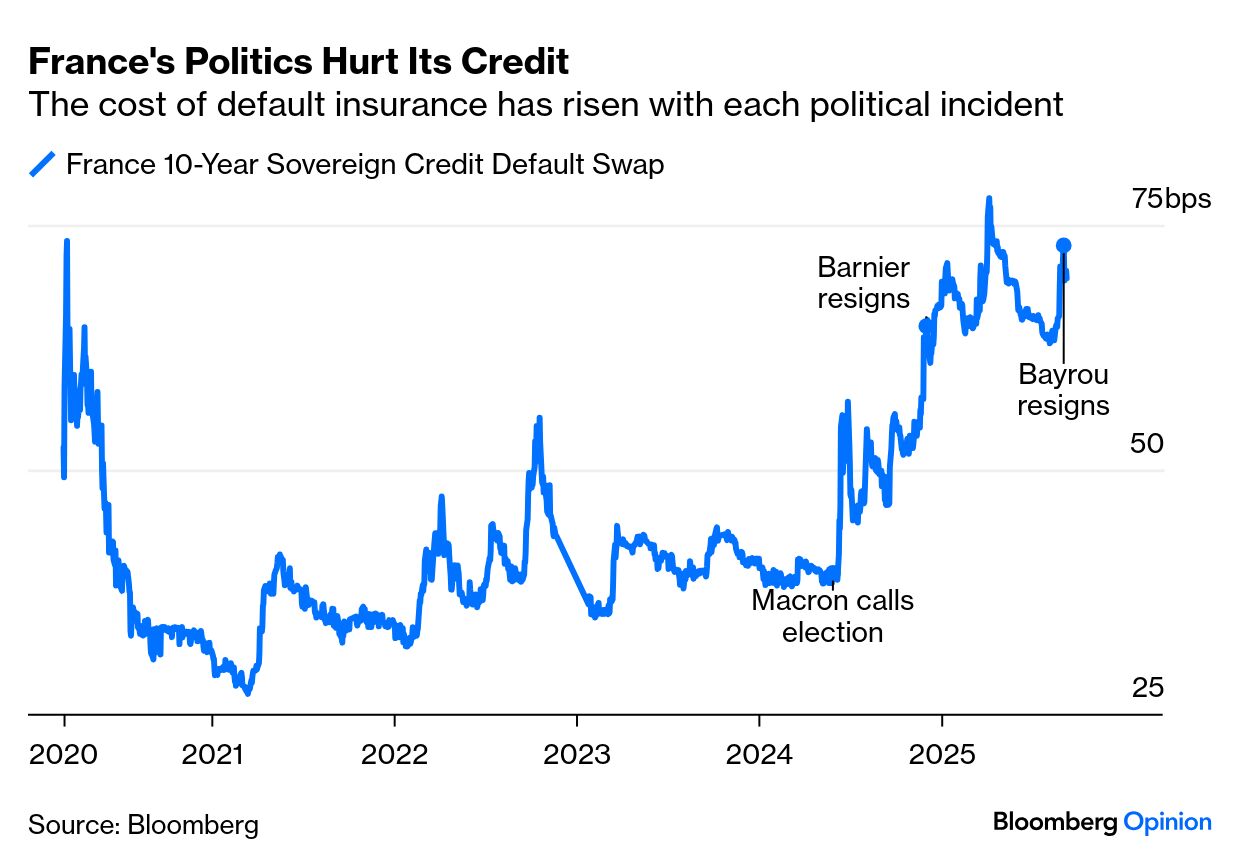

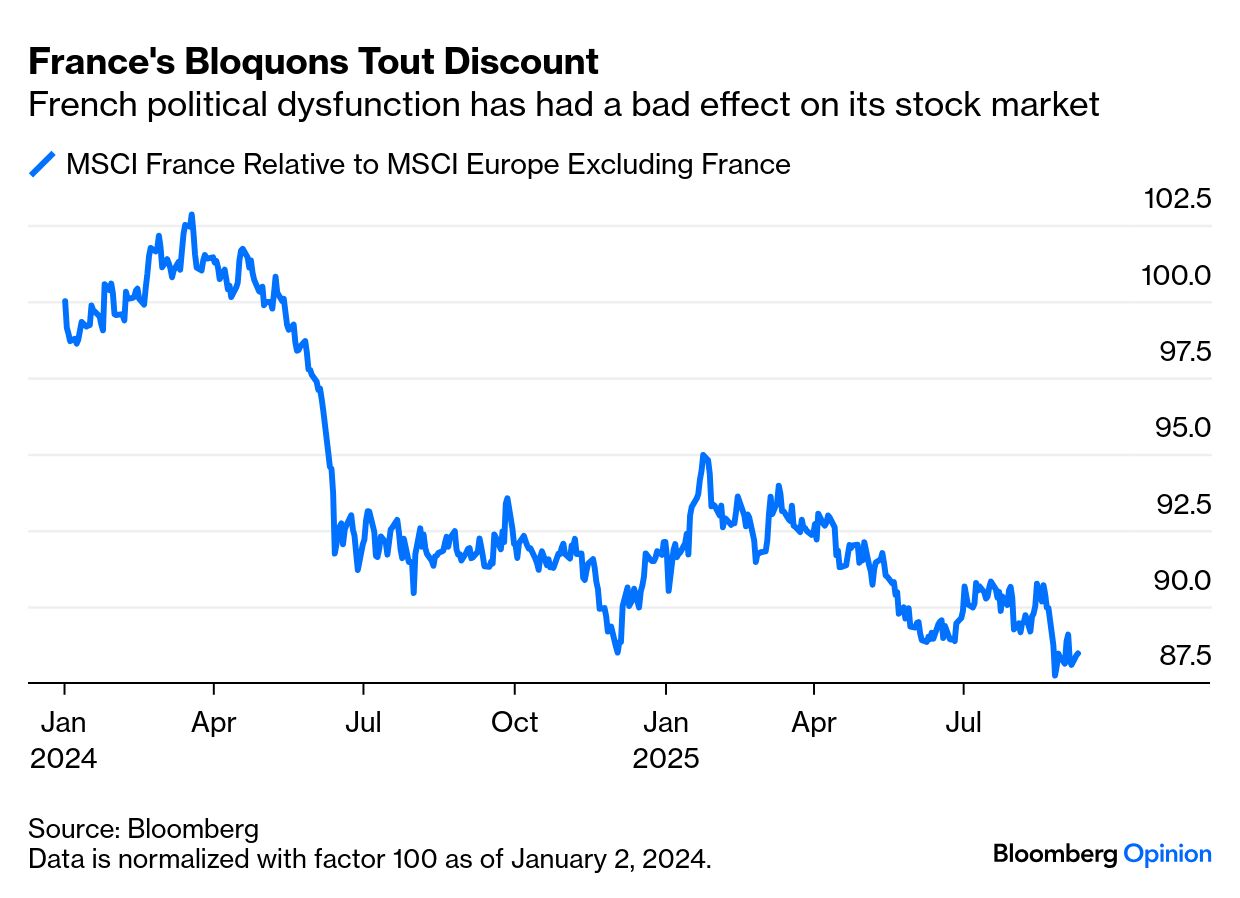

| To get John Authers’ newsletter delivered directly to your inbox, sign up here. The ECB is likely to keep rates on hold, as it looks like it | | | | | | To get John Authers’ newsletter delivered directly to your inbox, sign up here. | | | | | | Permission to Land for the ECB | | | While the furor over the Federal Open Market Committee’s next meeting reaches an ever greater crescendo, Thursday’s European Central Bank gathering has long seemed done and dusted. It’s finished cutting and now it’s on hold. Anything else would be a black swan. Market estimates for the policy rate at the end of this year took a dive after Donald Trump’s “Liberation Day” tariffs on April 2, but they’re now barely changed from Jan. 1: Many want the ECB to cut further, given the political and fiscal mess in France, but a hold would reflect an important and underestimated truth. It looks like the central bank has engineered a soft landing. This is the classic misery index — a combination of the inflation and unemployment rates: That’s helped by another easy-to-miss positive development. Europe’s banks languished after the Global Financial Crisis far longer than US counterparts, but have finally regained investors’ confidence in the value of the assets on their balance sheets. For the first time since the Greek crisis broke out in early 2010, eurozone banks are priced at more than their book value: Further, inflation expectations have been slain. This is the norm for Germany, but market forecasts surged briefly and exceeded US breakevens during the energy crisis that followed the invasion of Ukraine in 2022. German 10-year breakevens are back comfortably below 2%, and below the US: Meanwhile, US rates are falling. That’s narrowed the gap between US and European 10-year yields back to the levels seen before “Liberation Day,” when the dramatic German plan for fiscal expansion ignited optimism: All this sounds Pollyanna-ish when France is in a full-blown political crisis. President Emmanuel Macron has appointed his defense minister, Sebastien Lecornu, as his fourth prime minister in less than two years. With a seemingly intractable fiscal problem, the cost of insuring French debt has risen with each step in the political turmoil: With widespread street protests by a group called Bloquons Tout (“Let’s Block Everything”), successors to 2018’s gilets jaunes, and France’s legislature split between three roughly equal but incompatible political blocs, Lecornu’s chances of finding a meaningful fiscal resolution look minimal. And yet the negativity might create an opportunity. Since the beginning of 2024, French stocks have lagged the rest of the continent by 12%: There is a deep bench of international French companies for whom domestic politics have little relevance. This degree of underperformance therefore looks overdone. To quote Vincent Deluard, macro strategist for StoneX Financial: French equities have already underperformed their German peers by 25% since 2024, wiping out almost all of the relative gains they achieved during Germany’s post-2015 economic slump. The French luxury groups that dominate the CAC-40 index derive less than 10% of their revenues from France, and most of them trade at a lower multiple than US fast-food chains. The caretaker government and its likely right-wing successor after the 2027 general election are unlikely to raise corporate taxes, so French stocks should catch up in the coming years.

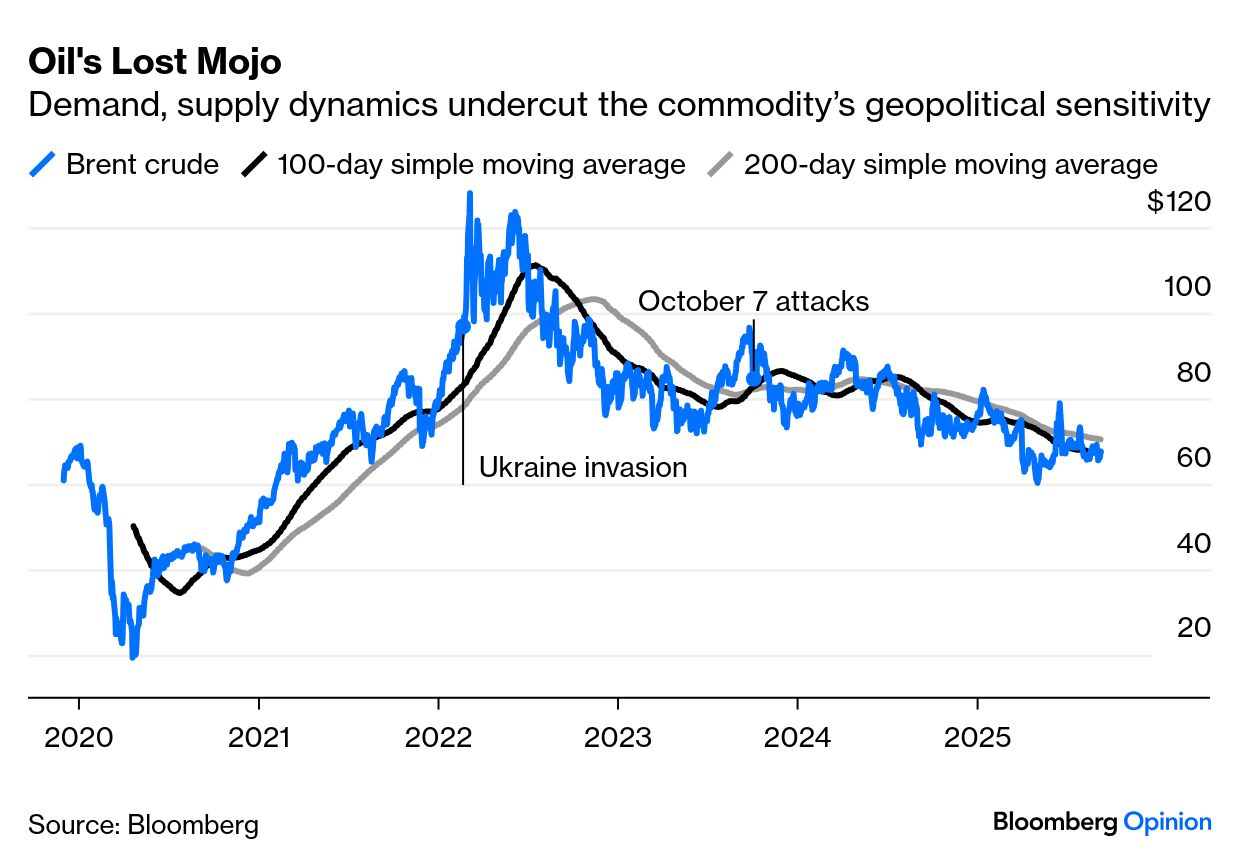

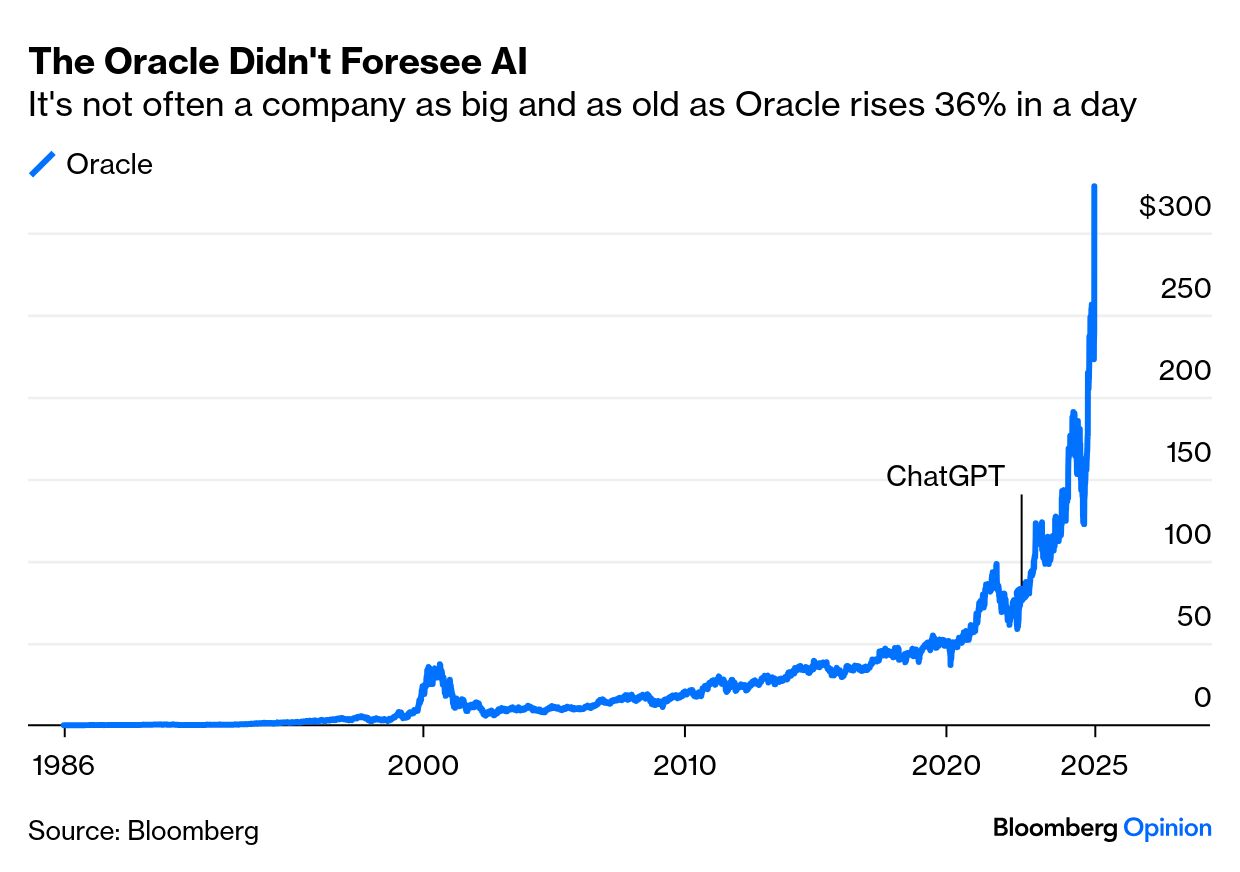

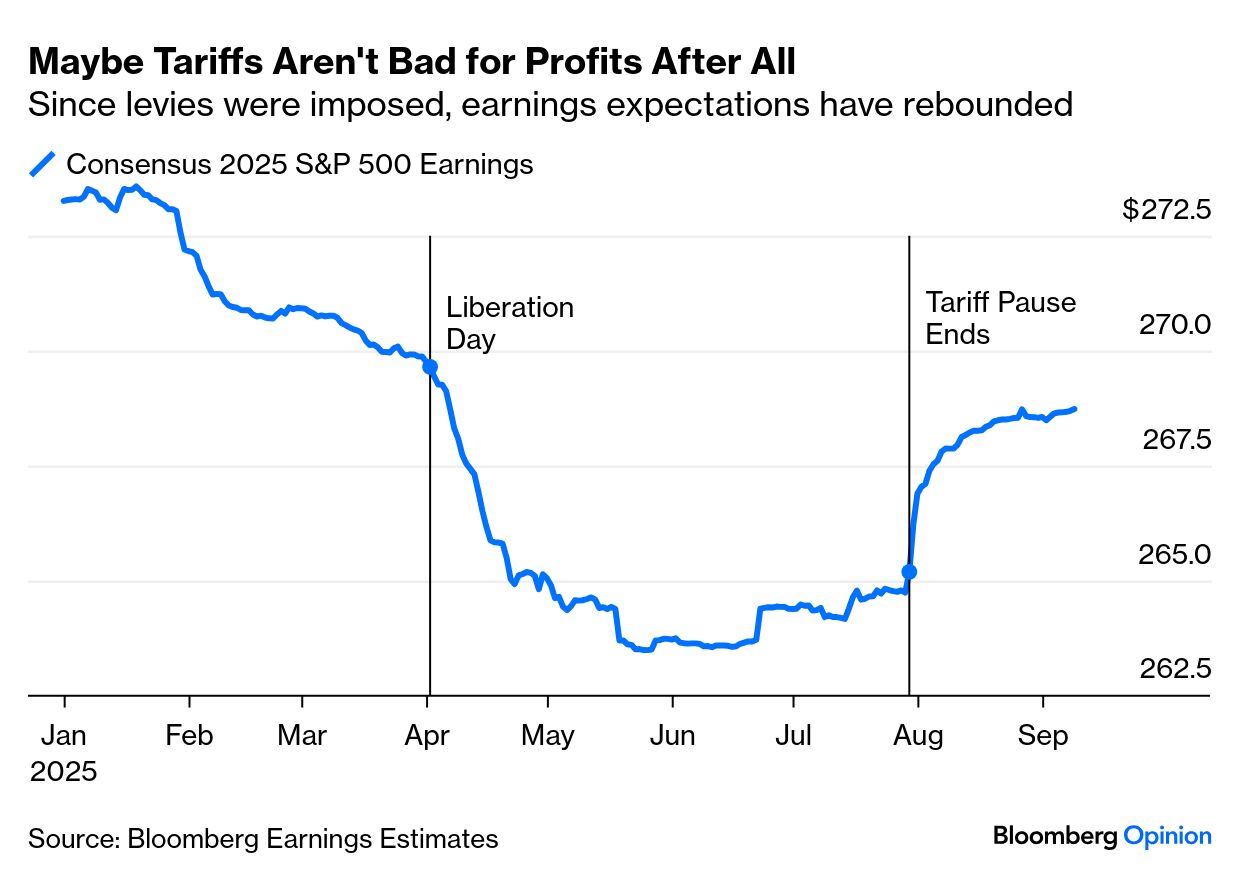

Using the brutal logic of markets, French stocks look like a buy. And the rest of Europe looks more investable than it did a few months ago, and well positioned to benefit if the Fed cuts rates as hoped. | | | | | Oil seems ever less sensitive to geopolitical shocks. In the last week, it’s barely reacted to two major flashpoints: Israel’s strikes deep inside US ally Qatar, risking dangerous escalation in the Middle East, and Russia’s brazen violation of Polish airspace, the Kremlin’s most direct engagement with NATO in recent times. It prompted Poland to invoke NATO’s Article IV, which calls for mutual defense. After the Polish incident, oil rose as much as 2.3% before giving up some of the advance. Brent crude remains below its 100-day and 200-day moving averages. Bloomberg Economics’ Dina Esfandiary and Ziad Daoud argue that although the temporary spike is understandable, prices are no more likely to rise persistently after this latest strike than after other recent flashpoints in the Middle East. Qatar is a significant gas provider, but its production and transportation facilities remain intact: Also keeping a lid on the price is OPEC+’s policy of oversupply, even though its most recent announcement fell short of market expectations. The cartel is still ramping up output even as global demand stays flat, effectively capping prices at moments of tension. The interventions suggest a covert attempt aimed at placating Trump, who has made clear his preference for cheaper oil. Further, Bloomberg Opinion colleague Javier Blas notes the growth in oil demand is on a structural downward trajectory, thanks to shifts in China’s economy, and the growing adoption of electric vehicles around the world. Oil is very unlikely to see production fall short of demand, so the status quo should hold. This bearish price outlook does, at the margin, make it easier for Trump to move to resolve the Ukraine conflict. But bringing Vladimir Putin to the negotiating table and securing meaningful concessions will require cooperation from key Russian allies, led by China and India. Tina Fordham of Fordham Global Foresight sees Trump trying to pressure the European Union to impose sanctions on countries that buy Russian energy. The Kremlin’s escalating aggression toward Kyiv and its confrontation with Poland could test the US president’s resolve. Andrew Bishop of Signum Global Advisors argues that the Polish incident could annoy Washington more than Moscow thinks, but is unlikely to matter as Trump wouldn’t want to risk the 2026 midterm elections by allowing gasoline prices to rise. BCA Research’s Marko Papic suggests that Putin might at last prompt a Trump reaction; an indirect approach similar to the one the Obama administration used to pressure Iran could work. That would be painful in the short term for countries that rely on Russian energy supplies, argues Kaan Nazli of Neuberger Berman. Secondary sanctions would disrupt the global economy, and deepen the trade war. Such an aggressive coordinated attempt to cut off Russia’s oil exports would raise oil prices. Without such an action, expect them to remain anchored. -- Richard Abbey | | | | | The S&P 500 set yet another record Wednesday, after the briefest of tremors in response to the appalling news of the assassination of the prominent conservative activist Charlie Kirk. The rally since the gauge’s April 8 nadir is now 31.1%. It all seems dissonant, as I tried to explore in this video: There are some explanations, which go beyond an almost certain rate cut by the Federal Reserve next week. First, almost three years after ChatGPT ignited an artificial intelligence gold rush, AI still has the capacity to administer a positive surprise. This is true even when applied to a huge and established name like Oracle Corp., which has been a public company for 40 years. Its results, published after Tuesday’s close, prompted a 36% rise when trading resumed. That kind of positive jolt for a business so well-known and so big is vanishingly rare: AI is being hyped and at some point will be over-hyped. But while there’s still the possibility for something like Oracle’s miraculous day, animal spirits will continue. And Oracle still didn’t gain quite as much market cap on Wednesday as Nvidia Corp. The other key driver for the rally is a massive upgrade in S&P 500 earnings expectations since August. Consensus projections for 2025 remain a little lower than before the April 2 tariff announcement — but in essence reflect a belief that the levies won’t have the impact initially expected: They also assume that corporate profits will somehow continue to rise even as the economy slows — an essential condition for a significant cut in interest rates. This isn’t necessarily a safe assumption, but while people are making it, the market rallies. | | | | | Violence — we should all remember on the 24th anniversary of 9/11 — is never the way to deal with political disagreements. Wednesday’s appalling assassination of the conservative activist Charlie Kirk, a 31-year-old father of two, is only the latest reminder. Today’s reactions bring to mind a classic piece of reportage. Alistair Cook, the legendary British journalist, was by chance only feet away when Bobby Kennedy was shot in 1968. Amid the confusion, he reported a woman beat a table and “howled like a wolf, ‘Stinking country, no no no no’.” That’s the way Americans, on either end of the political spectrum, are reacting to Kirk’s murder. It’s worth reading all of Cook’s piece, but this passage, addressed to Europeans, is most relevant: I have no doubt that this experience is a trauma and because of it, no doubt, and five days later I still cannot rise to the general lamentations about a sick society. I, for one, do not feel like an accessory to a crime. And I reject almost as a frivolous obscenity the sophistry of collective guilt, the idea that I, or the American people, killed John Fitzgerald Kennedy and Martin Luther King, and Robert Francis Kennedy. I don’t believe, either, that you conceived Hitler, and that in some deep, unfathomable sense, all Europe was responsible for the extermination of six million Jews. With Edmund Burke, I do not know how you can indict a whole nation.

Kirk’s murder understandably shakes Americans’ confidence in their nation, but it’s too soon to indict any national sickness. Rest in Peace, Charlie Kirk. More From Bloomberg Opinion: | | | | | You received this message because you are subscribed to Bloomberg's Points of Return newsletter. If a friend forwarded you this message, sign up here to get it in your inbox. | | | |