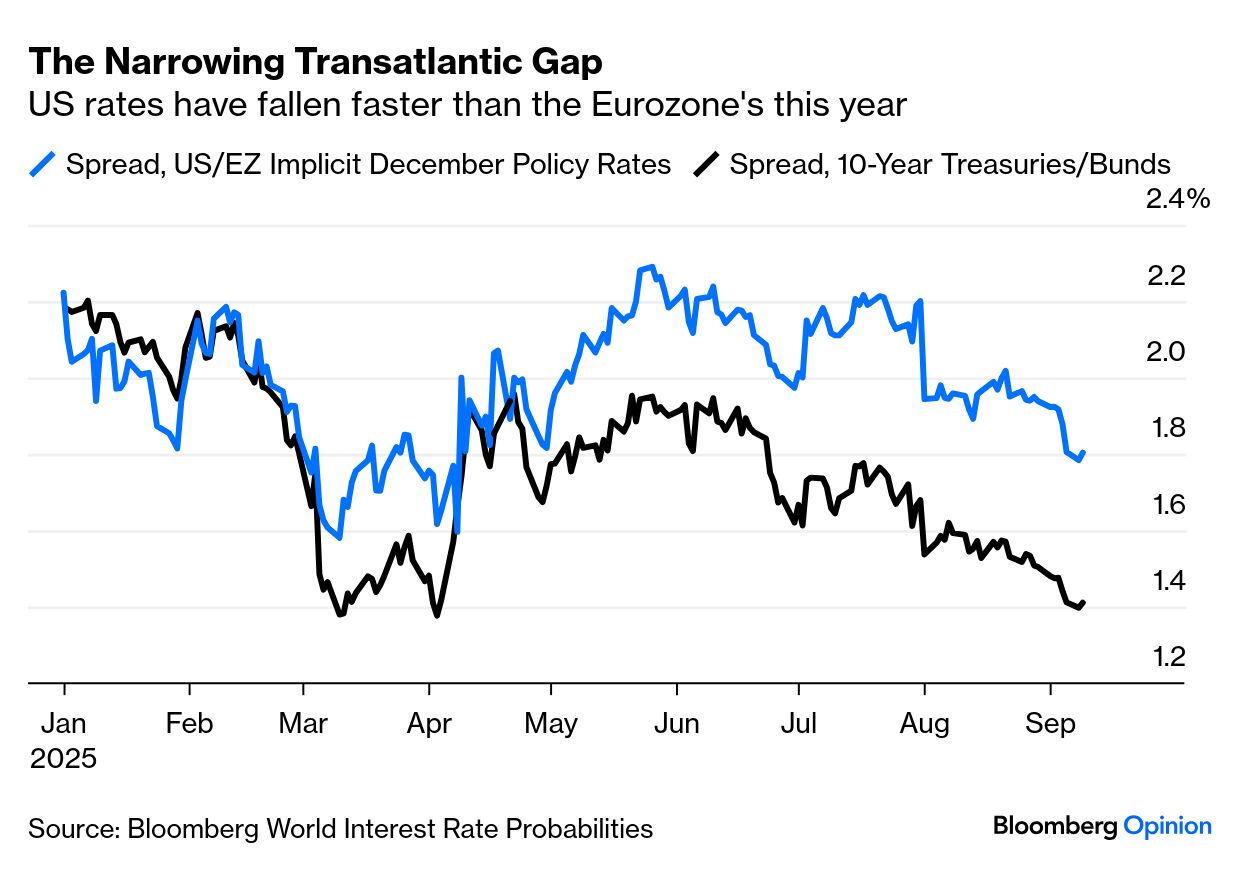

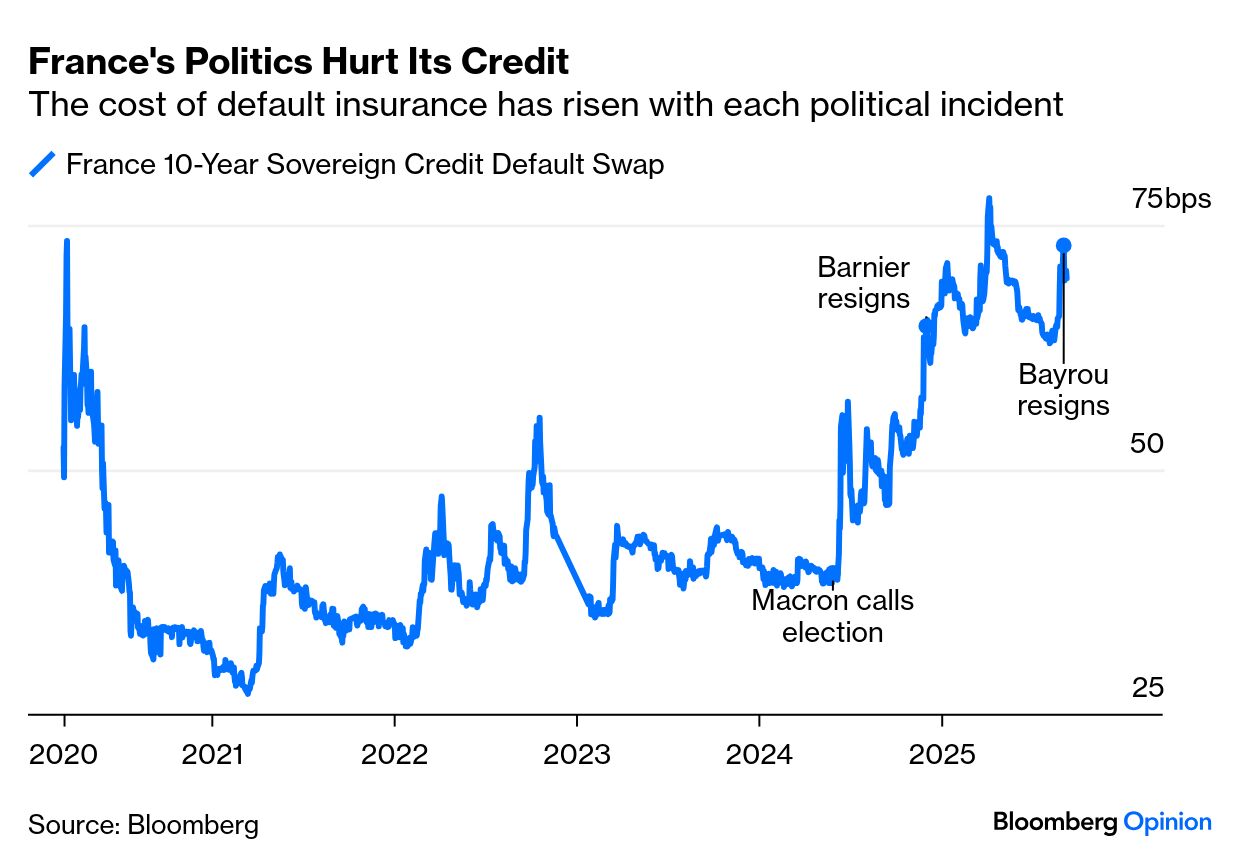

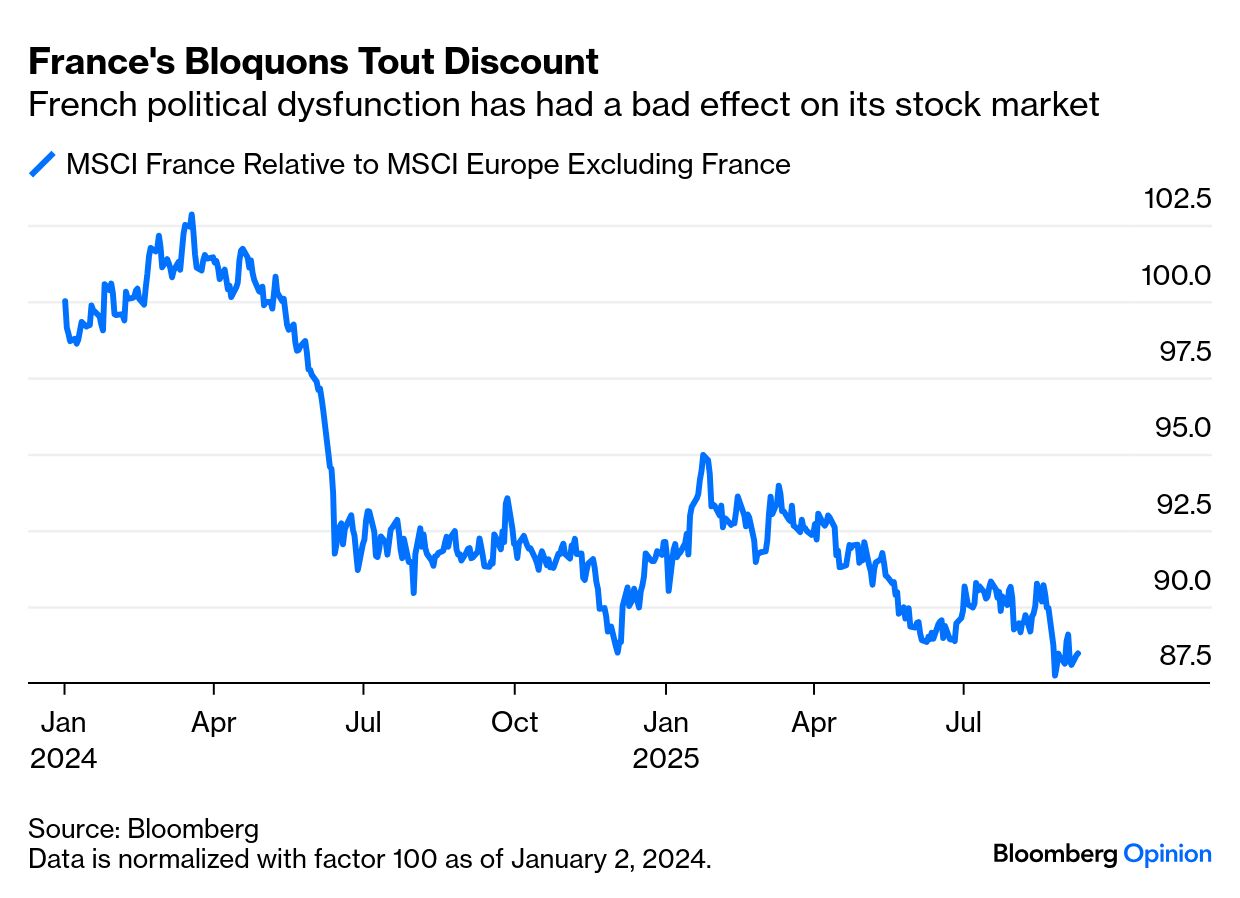

| While the furor over the Federal Open Market Committee’s next meeting reaches an ever greater crescendo, Thursday’s European Central Bank gathering has long seemed done and dusted. It’s finished cutting and now it’s on hold. Anything else would be a black swan. Market estimates for the policy rate at the end of this year took a dive after Donald Trump’s “Liberation Day” tariffs on April 2, but they’re now barely changed from Jan. 1: Many want the ECB to cut further, given the political and fiscal mess in France, but a hold would reflect an important and underestimated truth. It looks like the central bank has engineered a soft landing. This is the classic misery index — a combination of the inflation and unemployment rates: That’s helped by another easy-to-miss positive development. Europe’s banks languished after the Global Financial Crisis far longer than US counterparts, but have finally regained investors’ confidence in the value of the assets on their balance sheets. For the first time since the Greek crisis broke out in early 2010, eurozone banks are priced at more than their book value: Further, inflation expectations have been slain. This is the norm for Germany, but market forecasts surged briefly and exceeded US breakevens during the energy crisis that followed the invasion of Ukraine in 2022. German 10-year breakevens are back comfortably below 2%, and below the US: Meanwhile, US rates are falling. That’s narrowed the gap between US and European 10-year yields back to the levels seen before “Liberation Day,” when the dramatic German plan for fiscal expansion ignited optimism: All this sounds Pollyanna-ish when France is in a full-blown political crisis. President Emmanuel Macron has appointed his defense minister, Sebastien Lecornu, as his fourth prime minister in less than two years. With a seemingly intractable fiscal problem, the cost of insuring French debt has risen with each step in the political turmoil: With widespread street protests by a group called Bloquons Tout (“Let’s Block Everything”), successors to 2018’s gilets jaunes, and France’s legislature split between three roughly equal but incompatible political blocs, Lecornu’s chances of finding a meaningful fiscal resolution look minimal. And yet the negativity might create an opportunity. Since the beginning of 2024, French stocks have lagged the rest of the continent by 12%: There is a deep bench of international French companies for whom domestic politics have little relevance. This degree of underperformance therefore looks overdone. To quote Vincent Deluard, macro strategist for StoneX Financial: French equities have already underperformed their German peers by 25% since 2024, wiping out almost all of the relative gains they achieved during Germany’s post-2015 economic slump. The French luxury groups that dominate the CAC-40 index derive less than 10% of their revenues from France, and most of them trade at a lower multiple than US fast-food chains. The caretaker government and its likely right-wing successor after the 2027 general election are unlikely to raise corporate taxes, so French stocks should catch up in the coming years.

Using the brutal logic of markets, French stocks look like a buy. And the rest of Europe looks more investable than it did a few months ago, and well positioned to benefit if the Fed cuts rates as hoped. |