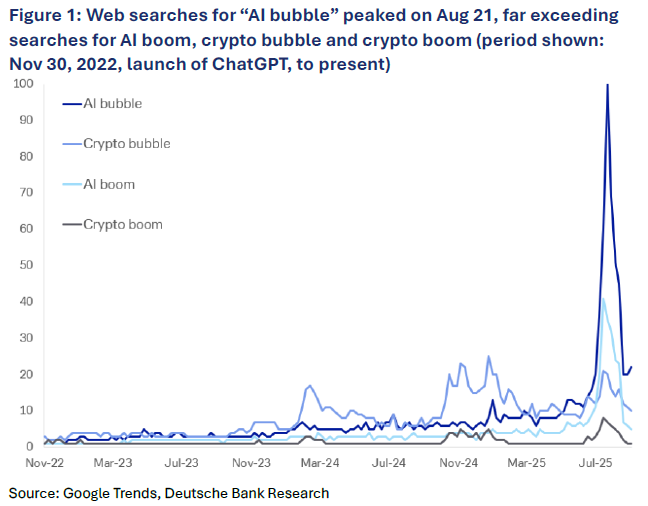

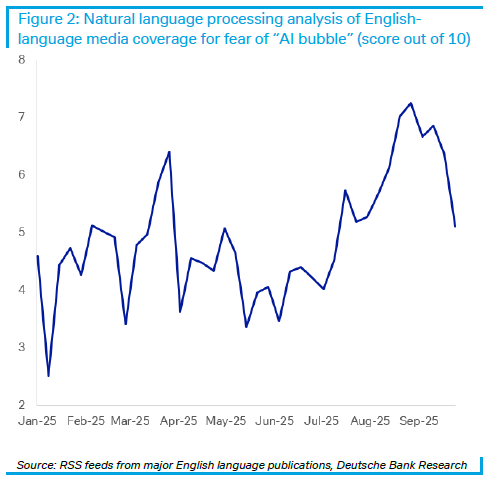

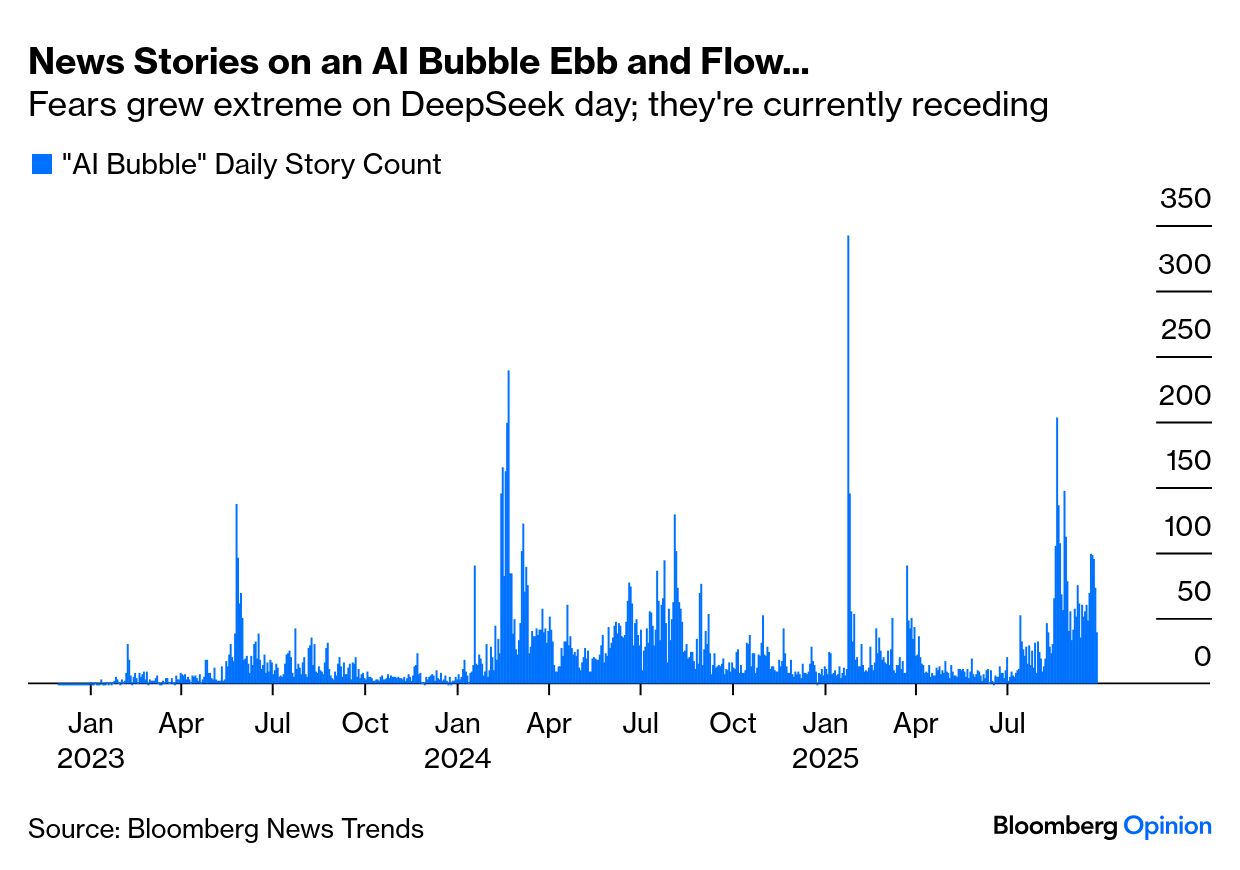

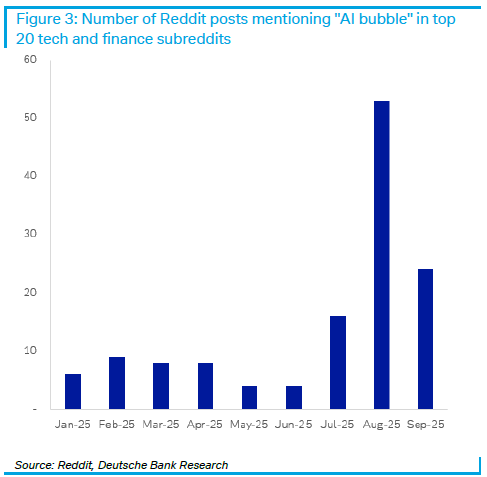

| It’s an impossible question to ignore, so let’s make another attempt to answer it. September saw the publication of at least two widely read analyses suggesting that what is going on in artificial intelligence is indeed a bubble: Is AI a Bubble?, published on Exponential View by Azeem Azhar, and Dotcom on Steroids by GQG Partners. And in line with classic bubble psychology, these serious attempts to diagnose the investment climate have appeared just as popular fears of a bubble have subsided. Adrian Cox of the Deutsche Bank Research Institute uses a battery of measures to show that the “AI Bubble” Bubble has now burst. This is how searches for the term have moved on Google Trends since the launch of ChatGPT in November 2022. There has always been more interest in the risk of a bubble than in the prospect of a boom: Crunching through major English-language media also found a peak of interest in an AI bubble last month, followed by quick descent: A search of the term on Bloomberg News Trends, which covers all stories from all sources that are published on the terminal, finds a series of waves of concern about bubbles, with the peak coming for a few days after the DeepSeek shock in late January: One final measure from Deutsche, looking at posts on Reddit, where all those most fascinated by finance are to be found, shows a peak in August followed by a decline: Cox argues that this is wholly consistent with a burst bubble lurking in the near future: “While there may be a bubble, the moment everyone spots it may be the moment it is least likely to burst.” In the run-up to the epic dot-com implosion, he points out that the Nasdaq Composite index suffered seven separate corrections of more than 10% before finally reaching its peak in 2000. 1999 and All That... This raises the issue of the most obvious parallel for the AI excitement. A quarter-century has now passed since dot-com bombed; does this mean that its lessons have not been learned? The GQG report suggests that it does: It may be hard for investors to face the uncomfortable reality that the trade that worked for over a decade may be over. After all, most money managers today do not carry the scars of the dot-com era. Of the approximately 1,700 active large-cap US portfolio managers, just 4% invested through that period. There is a difference between living through a downturn and merely reading about it.

As someone who also lived through the dot-com bubble and burst, I agree with this, but with two caveats. First, I have probably been too ready to see other imminent disasters in the years since. We are all prisoners of our own experience, and while most active managers don’t have direct experience of dot-com, the commentators they read generally do. Second, this episode feels different from 1999 and 2000. At that point, before de-industrialization had begun in earnest, before Vladimir Putin had arrived in Moscow, and while the Twin Towers of the World Trade Center were still standing, the US and its economy seemed invulnerable. Optimism and excitement were everywhere and frothed over. This time around, the excitement over AI feels more like a collective grasp for a lifeline. Psychologically, it’s different. A further specific issue with benchmarking to the dot-com era is that it was by most measures the most excessive stock market speculation there has ever been. Finding that the AI bubble isn’t as bad can miss the point, as nobody should want speculation to grow anything like that extreme. Stocks fell some 70% after the top in 2000; that doesn’t mean that anyone would be happy with a fall of 60% from here. Symptoms Irrational exuberance, as famously diagnosed by Robert Shiller ahead of the dot-com bust, is not the same as stupidity. Bubbles are hard to diagnose, but in hindsight the biggest were in technologies that proved to be revolutionary — canals, railroads, cars and the internet. They do, however, rely on cheap money. Robert Kindleberger, in his classic Manias, Panics and Crashes, produced a schema followed by all the great bubbles. Here it is, as summarized by Chris Watling of Longview Economics: i) cheap money underpins and creates the bubble; ii) debt is taken on during the bubble buildup, which helps fuel much of the speculative price increases (e.g. buying on margin); iii) once a bubble is formed, the asset price has a notably expensive valuation; iv) there’s always a convincing narrative to “explain away” the high price.

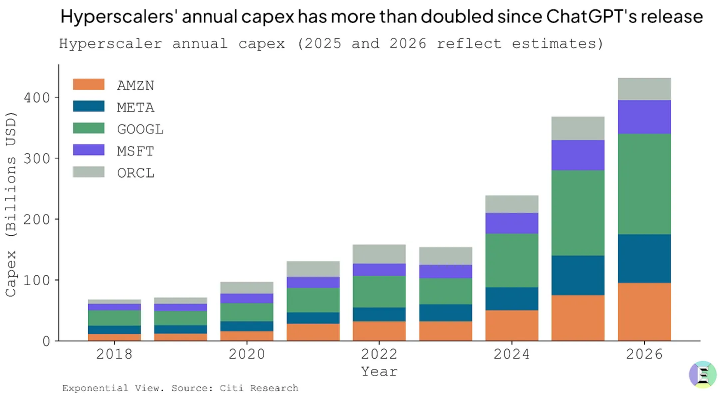

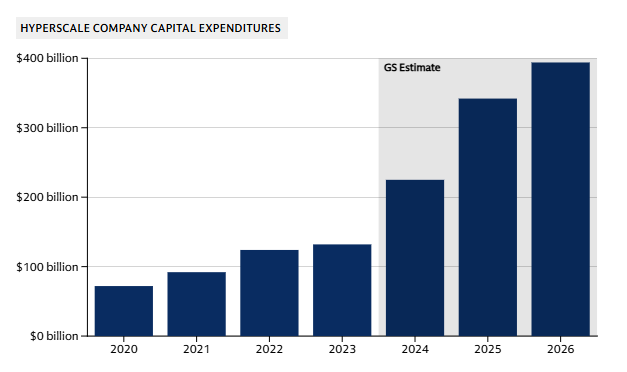

Humans find it difficult to extrapolate trends into the future, and once easy finance is available, justified excitement about something transformative can turn into wasted money. Valuations already look overdone, as Points of Return covered yesterday, and financing is cheap, even with complaints that the Federal Reserve is too hawkish. And the narrative, we’re all aware, seems mighty convincing. The symptoms of an imminent burst are there. GQG points out that companies previously regarded as invulnerable are suffering a steady derating even as their earnings continue to grow. They offer Adobe’s performance over the last five years as a clear example: The money being spent on capital expenditures also suggests that many have already taken extreme risks. Azhar offers this chart of hyperscalers’ expenditures, using data from Citi: Such a rate of increase looks unsustainable. It is the spending sparked by the bubble, rather than the share prices themselves, that looks dangerous. To quote GQG: Big tech CapEx as percentage of Ebitda is now running at 50%-70%, which is similar to AT&T’s 72% at the peak of the 2000 telecom bubble and Exxon’s 65% at the peak of the 2014 energy bubble. Historically, companies experiencing higher capital intensity tend to be structurally poor investments. In both the telecom and energy bubbles, an exciting new technology (internet for telecom, shale for energy) justified unprecedented levels of investment. Eventually, supply outstripped demand, and the companies never earned a return on their investment… However, customers benefited massively from cheap internet and energy.

Consequences The dot-com bust happened before Google had gone public. Facebook and Twitter did not yet exist. Netscape Navigator and Microsoft’s Internet Explorer were still fighting to be the dominant browser. The money lost by the irrationally exuberant back then did not stop the internet from transforming society and the economy. And several of the leading companies from that era remain in the lead today. However, Ian Harnett of Absolute Strategy Research makes this important point: The lead players today are still some of the best supported companies from that era — Microsoft/Apple/Oracle/Amazon. However, that didn’t stop each of those mega stocks falling -65%, -80%, -83% and -94% respectively vs their Tech bubble peaks to their troughs. Another salutary lesson is that they took 16, 5, 14 and 7 years respectively to regain those 2000 peak prices!

If you are shareholder, then, a burst bubble could be really bad news. However, the fact that this bubble, like the dot-coms, has been funded primarily by equity is good news for everyone else, as the economic impact should be reduced. Harnett suggests that the correction when it comes will be more like the fallout from the dot-coms than from the financial crisis of 2008, which was driven by defaults on debt and was far more serious for the economy. It should also mean that central banks need do less in response.

AI probably will have profound consequences on the way we all work. But Schumpeterian creative destruction being what it is, there will be some pain ahead before we all enjoy the businesses that are being built. |