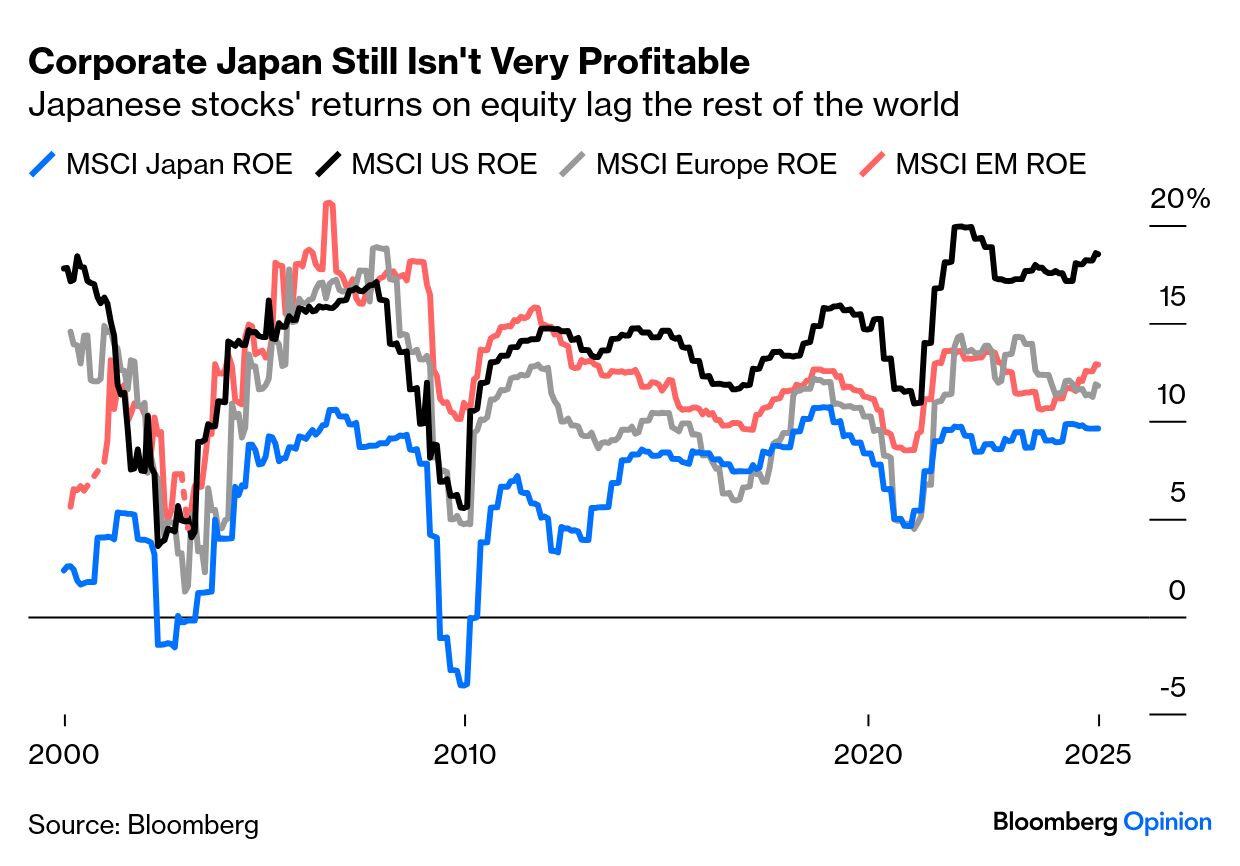

| It’s just possible that Japan is back; Gearoid Reidy goes into great detail on this question in the latest Bloomberg Markets. But at least as far as investors are concerned, two nagging questions remain to be answered: Can Japanese companies operate profitably? While Corporate Japan has produced admired companies that make great products, they tend not to make big profits. That has been true this century throughout waves of reform attempts, and continues to be the case.

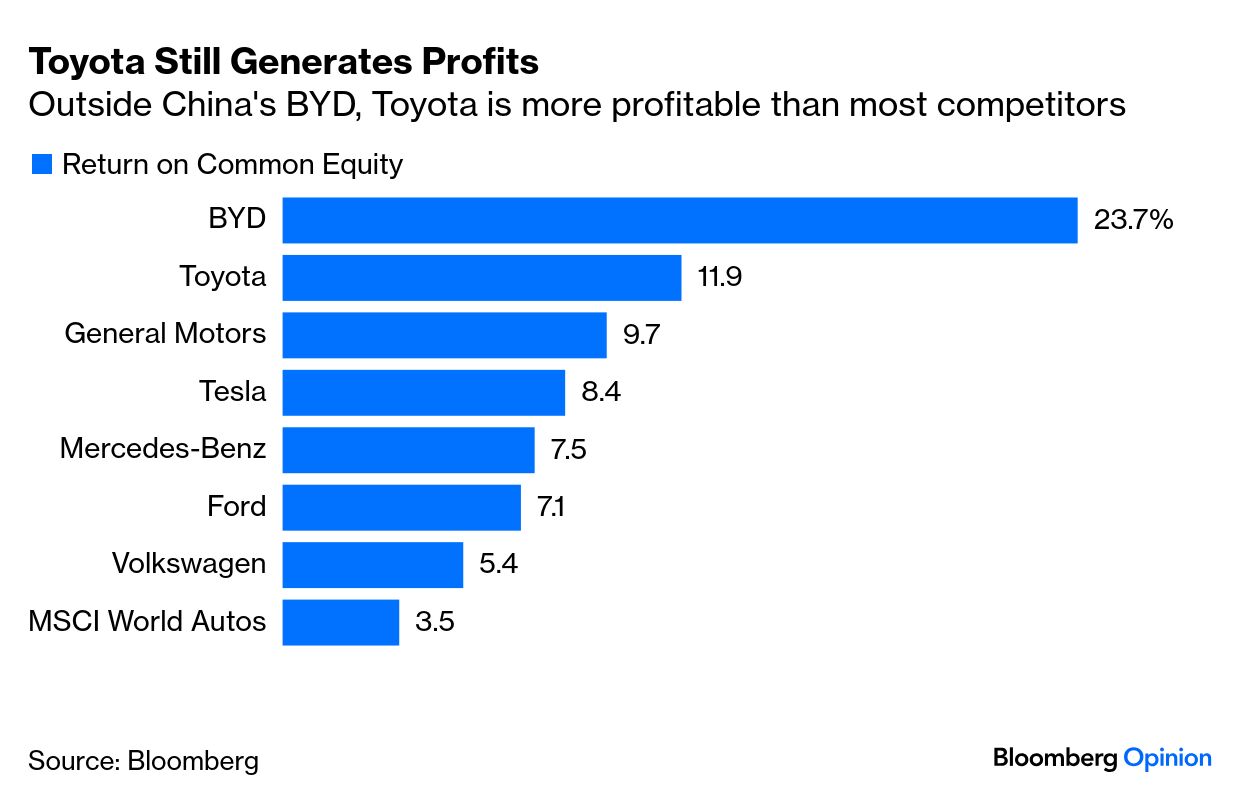

Return on shareholders’ equity, the simplest measure of profitability, and MSCI’s regional indexes show that Japan is significantly less profitable than the US. That might be expected. The rise in US margins since the pandemic is a phenomenon of the age. Less obviously, Japanese ROE lags both Europe and the emerging markets: There are some honorable exceptions, but mostly with companies that long ago established themselves. Toyota’s ROE has been overhauled by BYD, China’s dominant electric vehicle manufacturer, but remains well ahead of most of its global rivals (including Elon Musk’s Tesla Inc.): The status quo persists despite changes in corporate governance that have seen independent directors take up almost half the seats on Japanese boards, while foreign buyers concentrate their minds.

Nicholas Smith of CLSA Securities in Tokyo offers a barrage of reasons for the continuing lackluster profits. One is that Japan is instinctively cohesive and egalitarian. This is good for social harmony and makes the country the reverse image of the increasingly divided US. Unfortunately, the distinction also applies to company profits. According to Smith: US CEO compensation is 7.2x Japan’s, and even France’s is 3.0x. Worse, Japanese compensation has a higher fixed-pay component, incentivizing riskless attendance over bold excellence. Terms in office are short and fixed, with the period rarely tied to performance.

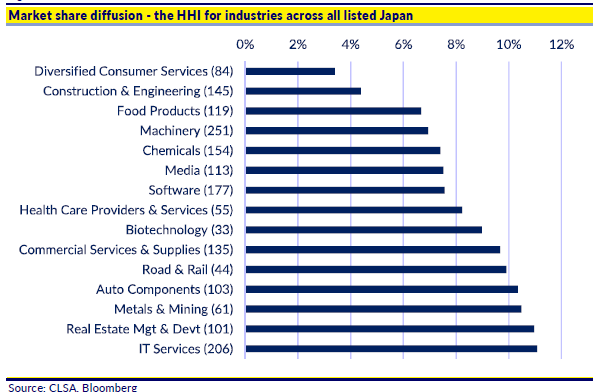

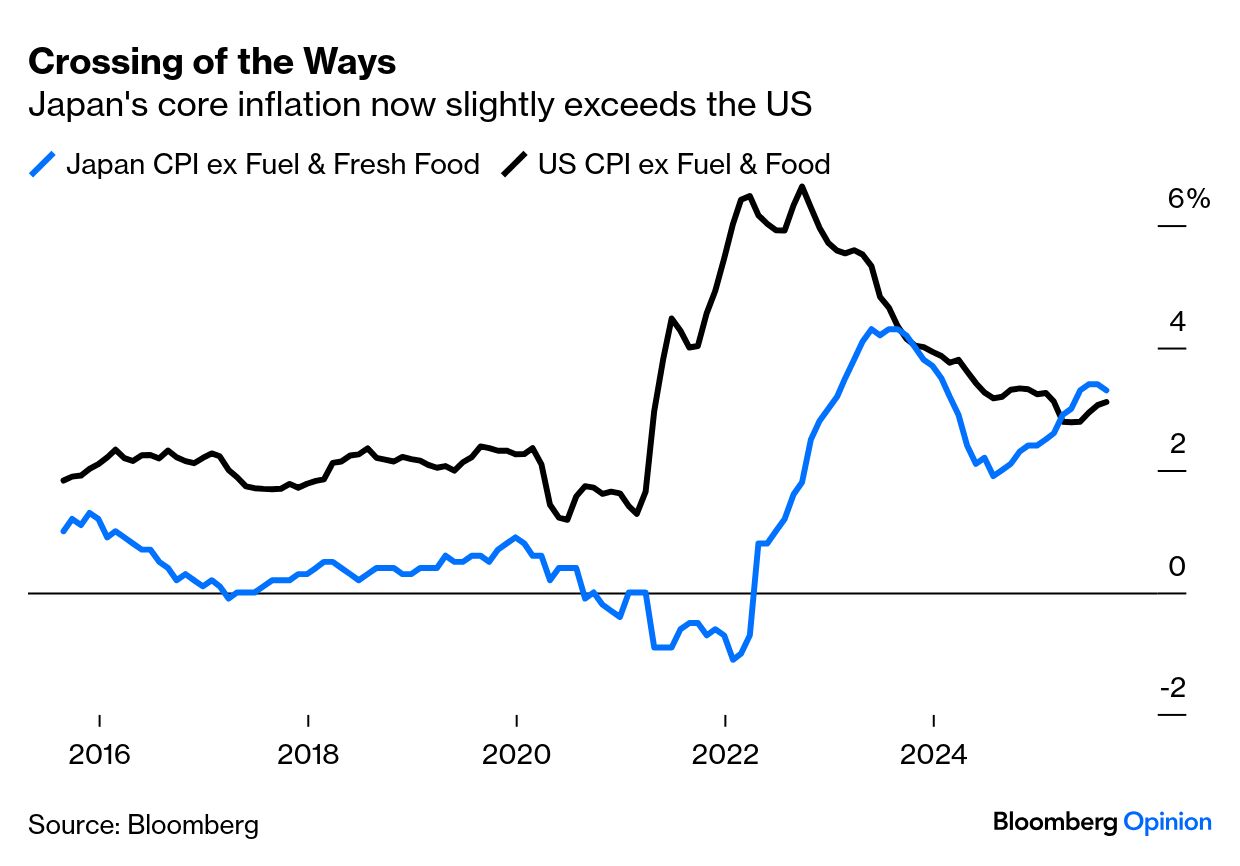

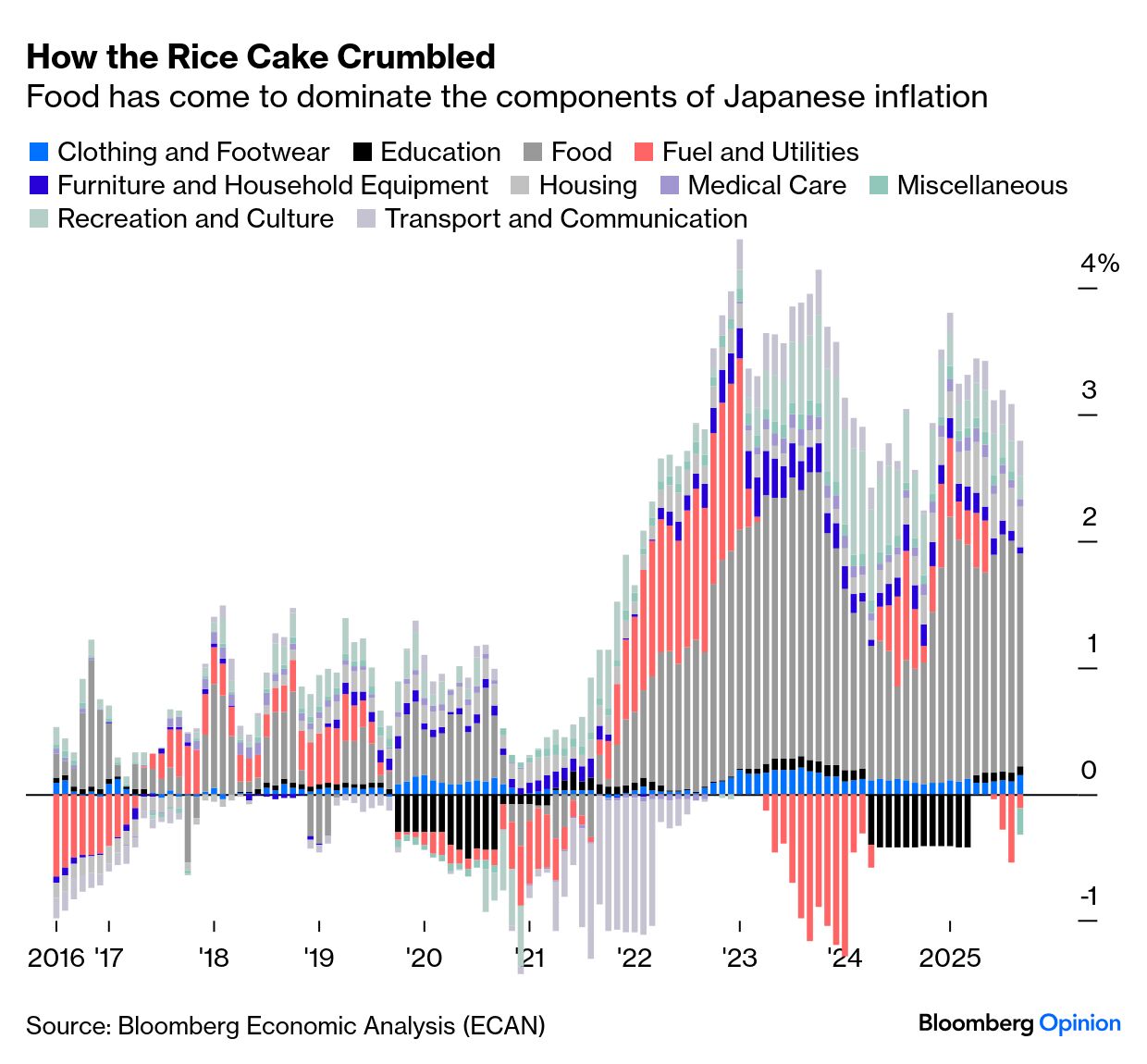

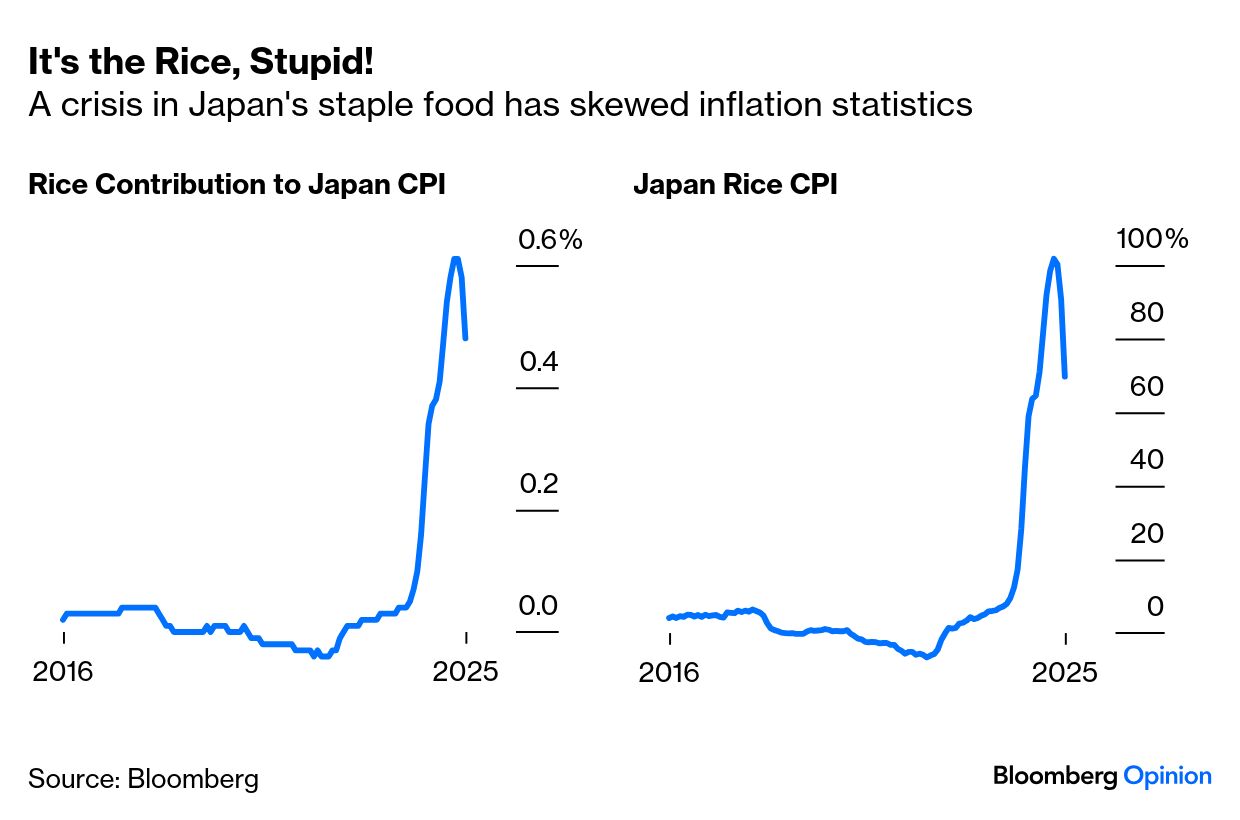

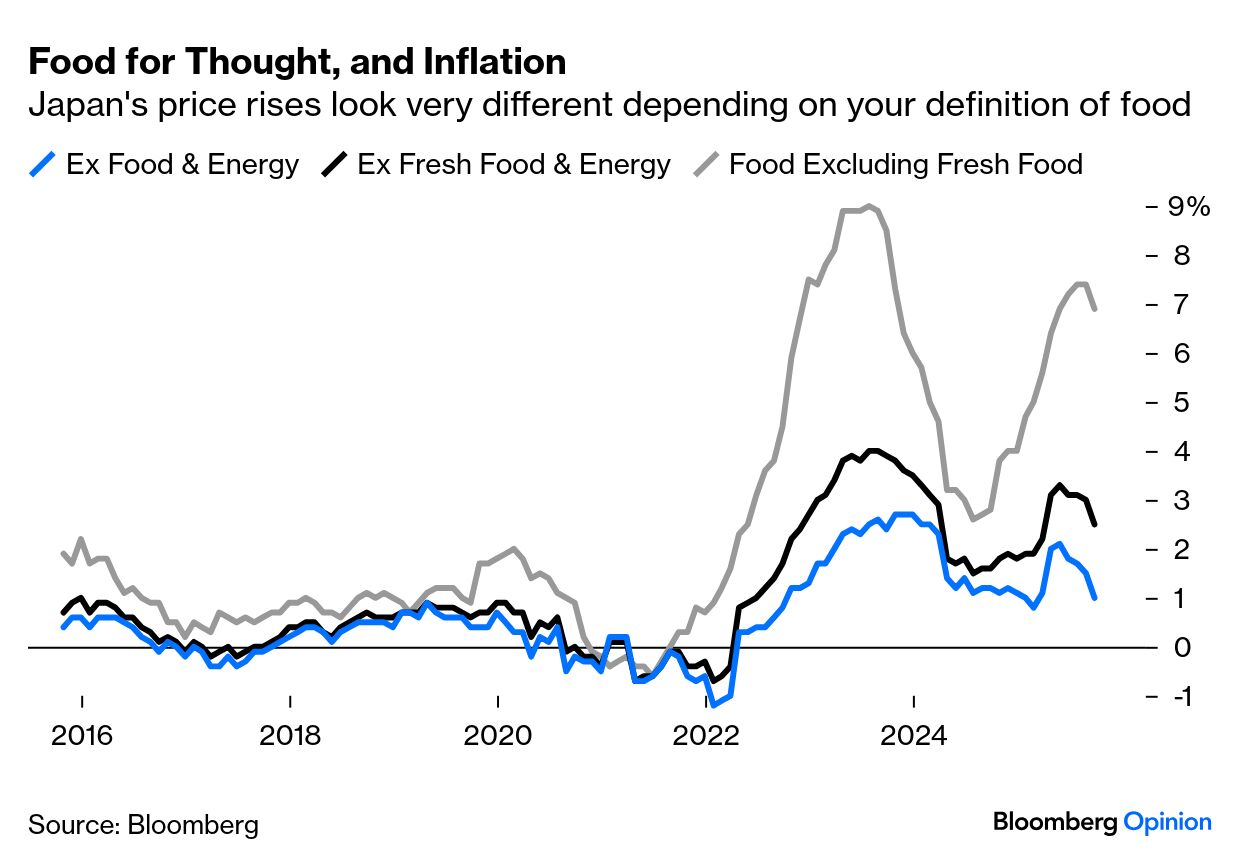

If US CEOs get too rich, Japan’s don’t have the chance to be rich enough. A further problem is that many companies are burdened by non-core units that don’t make money. Labor laws make it expensive to fire people, so the response has been to create divisions to house those who were no longer useful to the core business — and that now act as a lead weight on earnings. Then there is the issue of competition. If US industries are too concentrated, Japan has the opposite problem, leading to price competition that makes profits harder to come by. This CLSA chart shows the least concentrated Japanese industries, measured by the Herfndahl-Herschel index, where smaller figures show more competition: The way to deal with this, ultimately, is to push up profit margins, which is a bloody and difficult business. It does mean that there are gains to be made for any strategic or private equity buyers who think they can do this. Has deflation finally been beaten, or hasn't it? Look at Japan’s standard definition of core inflation, and it’s actually exceeded US CPI of late. It would seem that the decades of deflationary slump are over. As the Bank of Japan is still holding overnight rates at only 0.5%, normalization should be able to proceed apace: But it’s not as simple as that. Breaking down the consumer price index into its main constituent parts using the Bloomberg Economic Analysis (ECAN <GO> on the terminal), reveals that inflation is dominated by food prices. No other category is particularly elevated: The current high inflation, on closer inspection, owes almost everything to exceptionally steep rises in the price of rice, which has doubled inside a year. The harvest has became a political issue, with the agriculture minister receiving plaudits for beginning to bring the problem under control. But rice still contributes a full half percentage point to inflation on its own: Now the definitional issue. Japan’s core inflation excludes energy and fresh food. Adjust this to exclude all food, and it no longer exceeds the US core. Indeed, it drops to 1.6%, still well below the BOJ’s 2% target: Beyond the rice issue, there’s the currency. As detailed earlier this week, the yen is currently spectacularly weak, and has been since the central bank opted to keep monetary policy very easy as other countries started raising rates in 2022. “Before then, the dollar was at 105 yen; that’s fair value. Then it went to 160 yen and everything became expensive,” says former member of the BOJ’s policy board Sayuri Shirai, now a professor at Keio University in Tokyo. “We import almost everything.” A normalization should reverse that effect. The Bank of Japan has been described as “behind the curve” by US Treasury Secretary Scott Bessent, but Shirai says “he doesn't understand that it’s almost all food.” As US politicians can attest, the serious pain that people feel from food inflation is hard to ignore. But the BOJ doesn’t want to take responsibility for a resumed deflationary slump. The market currently puts a 57% chance of a hike later this month, which shows that the policy dilemma is evenly balanced — but those odds look too high. |