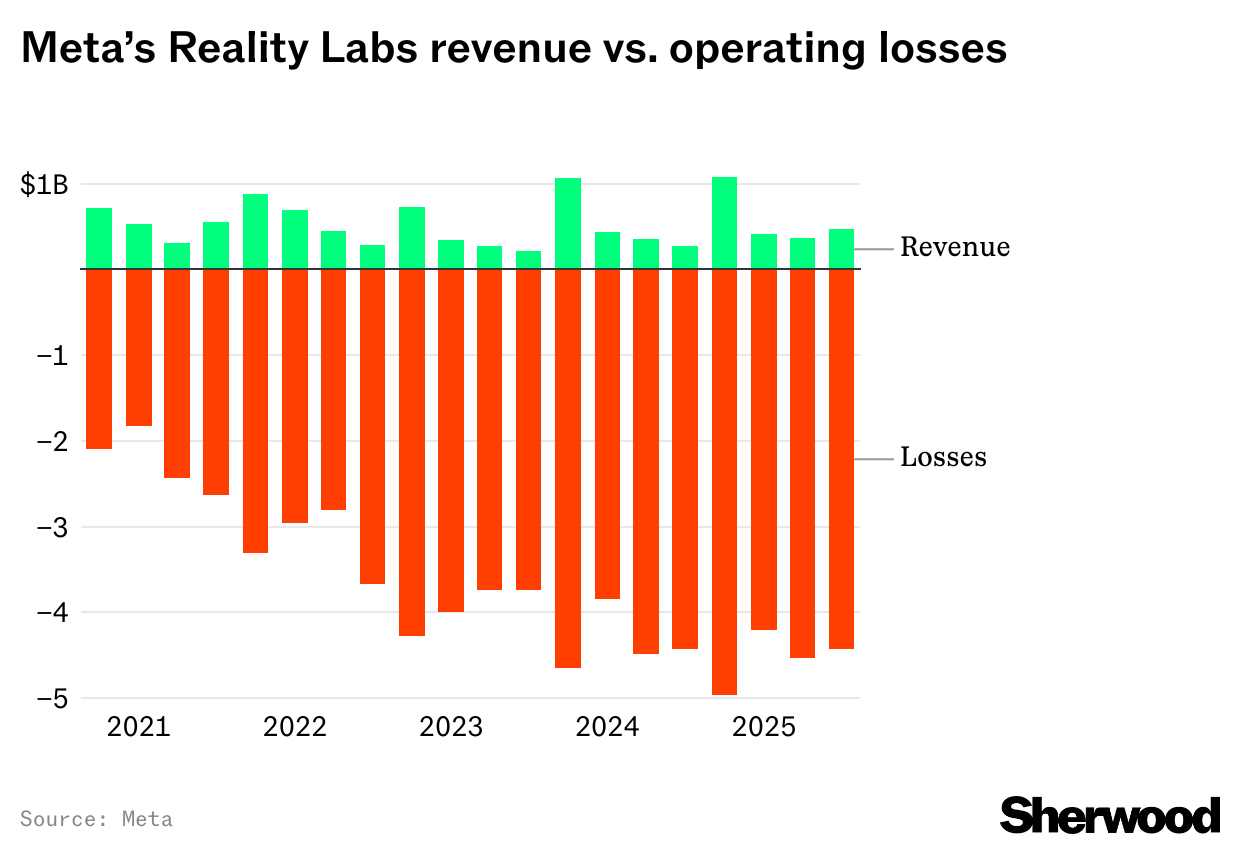

- Since the company started reporting those losses in late 2020, it’s totaled more than $73 billion.

- For Meta, the expense is worth it, as CEO Mark Zuckerberg believes the segment plays a key role in the company’s future. To put it simply, Meta doesn’t want to miss its iPhone moment again.

-

“Certainly, the investment here is not just to build just the device. It’s also to build these services on top,” Zuckerberg replied to a question during Meta’s earnings call last week. “Right now, a lot of people get the devices for a range of things that don’t even include the AI even though they like the AI. But I think over time, the AI is going to become the main thing that people are using them for and I think that that’s going to end up having a big business opportunity by itself.”

|

In other words, Meta isn’t just betting on selling hardware. It’s betting that its AI services built on top of those devices will generate a new stream of revenue — much like Apple’s ecosystem of services layered on the iPhone. |

|

|

Here, Meta — which (as Facebook) once tried and failed to build its own smartphone — is hoping history will rhyme rather than repeat. The difference this time is that Meta wants to own both the devices and the software that runs on them.

Like Apple, which has turned its Services segment into a reliable profit engine even as hardware sales have wobbled, Meta wants to ride that same train: hardware as a gateway, software as the payoff. |

|

|

Of all the many ways to measure investor sentiment — surveys, futures positioning, and more — one of our favorites might be through the answer to this question: how much are traders willing to pay for options that offer upside in stocks compared to those that protect against downside? |

- Cboe’s head of derivatives market intelligence, Mandy Xu, noted that about three weeks ago, skew in the S&P 500 spiked amid renewed market jitters over the fraying of America’s trade relationship with China.

- Skew, in this case, tracks the ratio between the implied volatility of puts versus calls, a proxy for the relative demand for bearish versus bullish options. Now that’s completely flipped on its head, for the index in general and for its largest components in particular.

-

“The number of stocks in the S&P top 100 trading with inverted call skew (a sign of extremely bullish sentiment where the OTM call trades at a higher volatility than the ATM call) has surged to a high of ~20% (vs. historical average of just 3%),” she wrote.

|

So, what does that mean for the bull market? |

|

|

Zooming in on a similar measure, Goldman Sachs analyst Cullen Morgan showed that sentiment is particularly ebullient for the so-called Magnificent 7.

“Coming into earnings this week, put-call skew in the Mag7 complex inverted for the first time since December of last year (i.e. implied volatility of calls traded over puts),” he wrote on Friday. “This phenomenon has only happened a handful of times. The move implies investors are overwhelmingly positioned for continued upside. Historically, such low skew readings have tended to coincide with short-term consolidation or reversals as optimism peaks.” |

|

|

The Texas Stock Exchange (TXSE) — a Dallas-based challenger pitching itself as a “pro-business” alternative to Wall Street — announced an investment from JPMorgan last week, bringing its total funding above $250 million ahead of its planned 2026 launch. More than 70 investors have joined so far, and TXSE’s debut marks the first SEC-approved exchange in decades that will eventually be able to both list as well as trade public companies’ shares.

|

|

|

|