MAIN FEATURE

The Five Decisions That Derail Portfolios

Smart people don't lose money because they make dumb decisions.

They lose money because they're forced to make decisions.

Almost every wealth failure I've ever seen shows up in one of these five moments.

1. Your income takes a hit

A client leaves. A business slows down. A job change takes longer than planned.

If an income drop forces you to sell investments just to pay bills, you didn't just have a bad month. You permanently damaged compounding.

Because once you sell, that money never gets the chance to keep working for you again. And this almost always happens at the worst possible time.

2. A large, unexpected expense shows up

Medical issues. Family situations. Taxes that come in way higher than expected.

If the only way to handle those moments is touching long-term investments, then your assets were doing the wrong job.

Assets are meant to grow. Not get eaten every time life throws a curveball.

3. Markets drop at the wrong time

Markets going down isn't the problem. They always go down.

The problem is when they go down and you need cash.

That's when selling feels unavoidable. That's when panic creeps in. That's when years of progress get undone by one decision.

Markets didn't force the sale. Cash pressure did.

4. You cross the "retirement line"

Most people are taught that once you retire, you start selling a little every year. Four percent. Five percent. Whatever the model says.

But think about that.

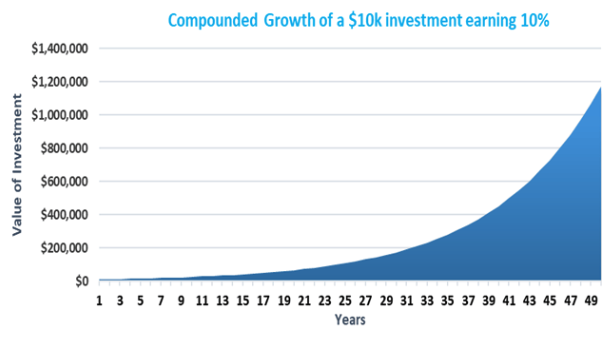

That's the exact moment when compounding is most powerful... and that's when people are told to shut it off.

That's not retirement. That's managed depletion.

5. You're asked to decide while emotions are high

Watching balances swing. Reading headlines. Feeling like you should "do something."

If your plan requires you to stay calm forever, it's not finished.

Nobody stays calm forever.

Real systems don't rely on perfect behavior. They're built so emotions don't matter.

So here's what I actually want you to do.

Take a piece of paper. Write these five things down:

- Income drops

- Unexpected expense

- Markets fall

- Reach retirement

- Emotional decision

Now go through them one by one and answer a single question:

What is my plan here that does not involve selling my investments?

Not what should happen. Not what you hope happens. What actually happens.

- If income drops, where does the money come from?

- If an expense shows up, what gets used?

- If markets fall, what do you live on?

- When you retire, how do you get paid without liquidating?

- When emotions are high, what decision has already been made for you?

If you don't have clear answers for these, my point isn't to freak you out. It's just this: let's start coming up with answers now.

While we're not in panic mode.

Don't wait until one of these things happens to you to figure out what the answers are.

The whole goal is to figure that out right now so that when those things arise, we're already prepared to weather that storm.

|