The S&P 500 ended up 1% on Monday, though futures have since given back some of that. Asian shares were mixed again on Tuesday, with South Korea’s KOSPI rising by 2.3% and Japan’s Nikkei closing flat. The dollar has firmed after easing slightly yesterday.

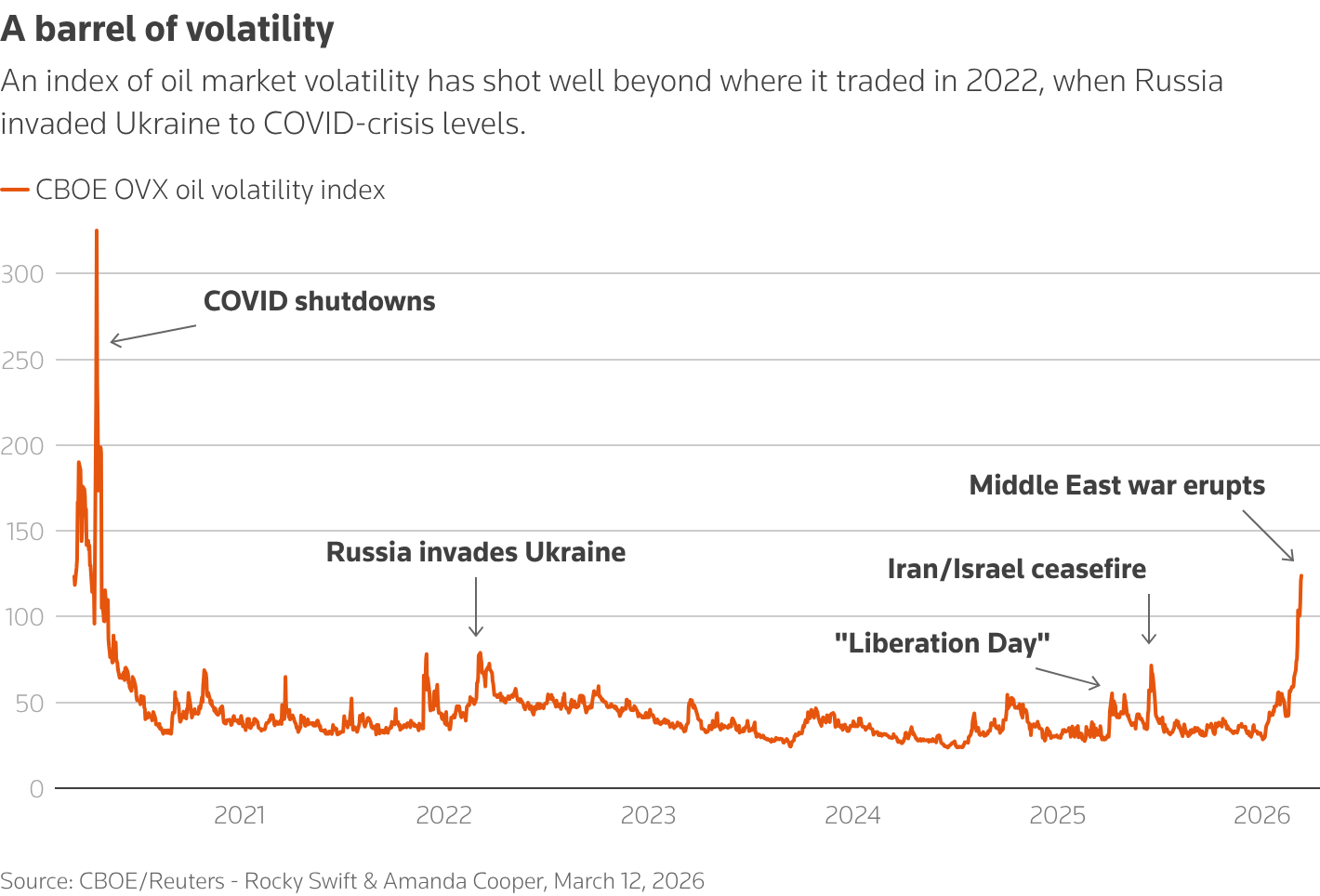

Part of Monday’s rally on Wall Street was due to a sizeable retreat in crude, as a kernel of optimism emerged about getting some ships heading to India, China and Pakistan through the Strait of Hormuz. Brent crude fell nearly 3% to settle at around $100 per barrel.

But that was short-lived. With few signs of any major breakthrough in the war and President Donald Trump struggling to draw NATO allies into a planned coalition to shepherd tankers through the strait, oil pushed higher once again on the simmering conflict, with Brent jumping to over $104 per barrel before easing slightly.

U.S.-China trade talks in Paris may also have helped improve sentiment at the margins, with the two sides holding constructive talks focused on agricultural goods and rare earths.

Another apparent cause of the lift on Monday came from the return of the AI theme to the forefront, as chipmaking giant Nvidia’s annual GTC developer conference got underway in San Jose.

The world’s most valuable company said that its AI chip revenue could potentially total $1 trillion through 2027, as it announced plans to compete more aggressively in inference computing. So far, Nvidia chips have dominated AI model training.

Meantime, South Korea’s SK Hynix warned that strong AI demand could cause the global chip wafer shortage to last until 2030.

Turning to central banks, the Reserve Bank of Australia’s unexpectedly narrow 5-4 vote to hike rates left the prospect of further tightening an open question. In response, the Australian dollar was a bit choppy on Tuesday.

Focus will now shift to policy decisions from other big central banks this week, including from the Federal Reserve tomorrow. Trump on Monday called on the Fed to hold an emergency meeting to cut rates, but the Fed’s biggest task will be showing how it can negotiate the likely inflationary spur from a prolonged oil shock.

With that, onto today's column.