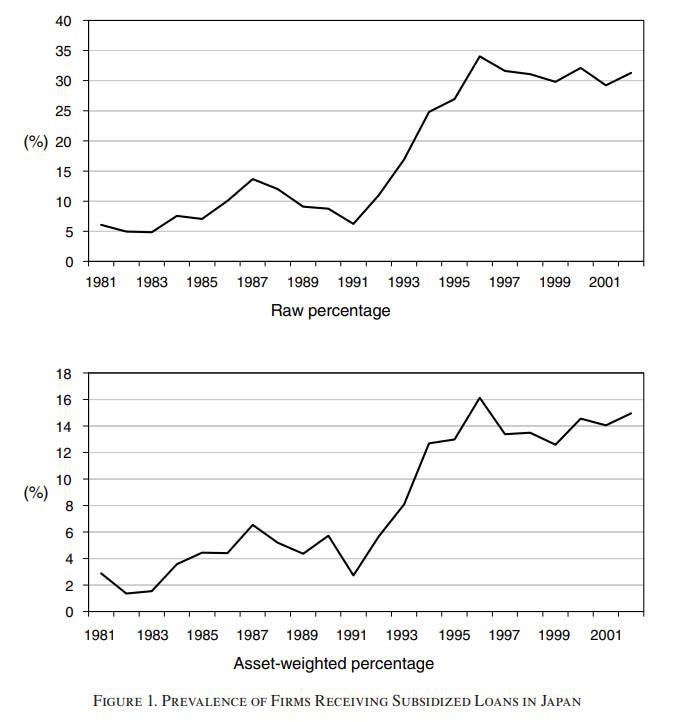

|

|

The photo above is not from China; it’s from Japan. In the 1970s, Daiei was Japan’s top retailer. But after Japan’s asset bubble burst around 1990, it became Japan’s most famous “zombie” company — staggering along unprofitably, kept afloat by a constant stream of below-market-rate loans from UFJ Bank and other big Japanese banks. Eventually the company was acquired by Aeon, a more successful retailer, and its once-storied brand is slated to be retired for good in the next few years.

I tend to be very skeptical of comparisons between post-1990 Japan and post-2021 China, because there are just so many differences between the two economies (and between the global economic environments at the time). Their industrial policies are different, their trading relationships are different, their bubbles and busts happened for very different reasons, and so on. But in the case of “zombie” companies, there may be some important parallels.

What’s important about Daiei is not how it failed, but why it didn’t fail much sooner. Caballero, Hoshi, and Kashyap wrote a paper in 2008 arguing that “zombie” companies like Daiei held the Japanese economy back during the 1990s (and, in some cases, even beyond the 1990s).

The basic story is that after 1990, the Japanese economy slowed down, and lots of companies that used to be profitable — especially in the construction, retail, and trading sectors — were no longer profitable. These companies owed a lot of money to banks. If they stopped being able to pay back their loans, the banks would be forced to recognize bad debt on their books. This would get them in trouble with regulators (because of capital requirements), and it would also get them in trouble with the Japanese public.

So what the banks did was to lend even more money to the failing companies that already owed them a lot of money, at very cheap interest rates. The new loans were used to pay back the old loans, and the new loans would be classified on the bank’s books as “good” debt. This process — known as “evergreening” — kept banks from ever having to acknowledge their losses:

|

Peek and Rosengren (2005) document this empirically as well.

Evergreening kept a bunch of companies afloat — like Daiei — that had utterly broken business models. Theoretically, the companies could have eventually pivoted their business models and recovered, or Japan’s economy could have started booming again, etc. In practice, this never happened.

Caballero, Hoshi, and Kashyap argue that evergreening was very bad for the Japanese economy, because it hoovered up scarce resources that better companies could have used to grow. With all of those crappy loans clogging up their books, Japanese banks couldn’t lend to healthier companies. With big zombies like Daiei still able to employ large amounts of Japan’s best managers, young scrappy upstarts were deprived of talent. The authors argue that keeping all of this labor and capital locked up inside doomed companies contributed significantly to Japan’s long productivity stagnation.

Why did the Japanese government allow this to happen? Preserving employment at the zombie companies was probably a big part of it. Japan had a strong tradition of job security at that point in time, and to throw so many people out of work — even if they could have gotten new jobs eventually — would have been seen as cruel and unfair. Social unrest was a possibility. Bank bailouts may also have been deeply politically unpopular. In any case, whatever the reason, throughout the 1990s the government supported banks with various capital injections and regulatory forbearance, without forcing banks to cut off the zombies.

Anyway, that’s Japan. The question is whether something like this will happen in China.

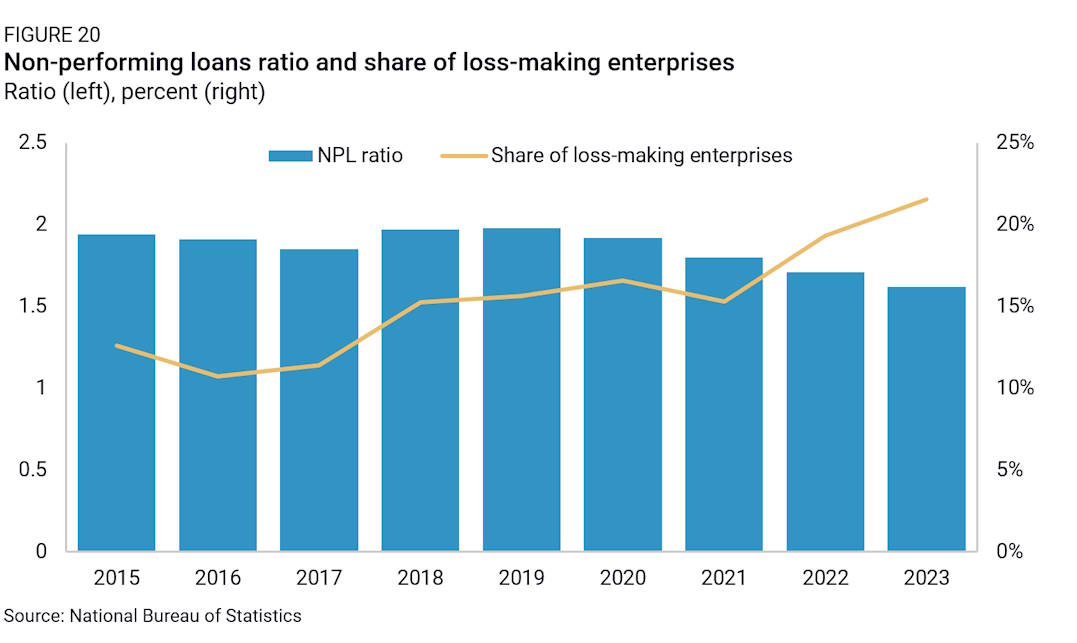

China’s experience with its real estate bubble and bust doesn’t exactly parallel Japan’s, but there are some broad similarities. Since 2021, there has been a broad economic slowdown (probably more severe than the official numbers suggest), and a long-lasting chill in real-estate-related industries. This has predictably led to a rise in the number of loss-making companies:

|

You’ll notice on this chart that the share of non-performing loans has actually gone down since 2021, even as fewer companies are turning a profit. That suggests that lots of Chinese companies are being kept on life support by cheap bank loans. Here’s the Rhodium Group:

Some concrete data points suggest that China’s evergreening of debt is more widespread than is commonly the case in most market economies. The ratio of banks’ reported non-performing loans has decreased over the past years, while the share of loss-making enterprises increased…This would indicate Chinese banks have been sitting on large volumes of NPLs that have not yet been fully recognized. This is an open secret: The National Audit Office recently claimed in an annual audit report to the NPC that 16 of 43 audited banks last year had NPL levels that were double the officially reported figure…

Loan rollovers are a pervasive phenomenon in China…[T]he financial system…served as a shock absorber, channeling resources to enterprises facing losses to maintain output and prevent the defaults and bankruptcies that occurred in market economies.

Another Rhodium report finds that the proportion of loans made below benchmark rates has risen significantly since 2021, even though benchmark rates are lower than they were back then: