While policymakers aren't expected to change the federal funds rate for now, markets will pay close attention to how Warsh himself votes and the language he uses at the press conference this afternoon.

President Donald Trump, who appointed Warsh, repeatedly called for dramatic rate cuts under previous Fed Chair Jerome Powell. Trump has since reiterated his preference for looser policy, though he has indicated that he will give Warsh room to act as he sees fit.

The problem for Warsh is that markets will likely view his words and actions through a political lens regardless, making effective communication that much harder.

The big question today is whether Warsh leans against the market's more hawkish tilt in recent months. The Iran war-driven energy squeeze and relatively healthy turn in U.S. economic data have upped bets for rate hikes this year - something individual policymakers have signalled an openness to down the line.

Of course, the preliminary deal between the U.S. and Iran will impact projections for inflation and rates - though by how much remains to be seen.

On that note, bond yields fell on Wednesday as oil prices slid in early trading, with global benchmark Brent crude hovering around $79 a barrel. The catalyst for this latest drop appears to be reports that the U.S. will waive sanctions on Iranian oil for a defined period of time, with all U.S. and UN sanctions on Iran expected to be lifted if a final deal is signed.

Still, it's far too early to say how much oil and gas will be coming out of the Strait of Hormuz in the coming months, given all the unknowns about the deal itself and the damage to energy facilities caused by the war in the Gulf. This suggests that we could see some volatility ahead as the market finds its new balance.

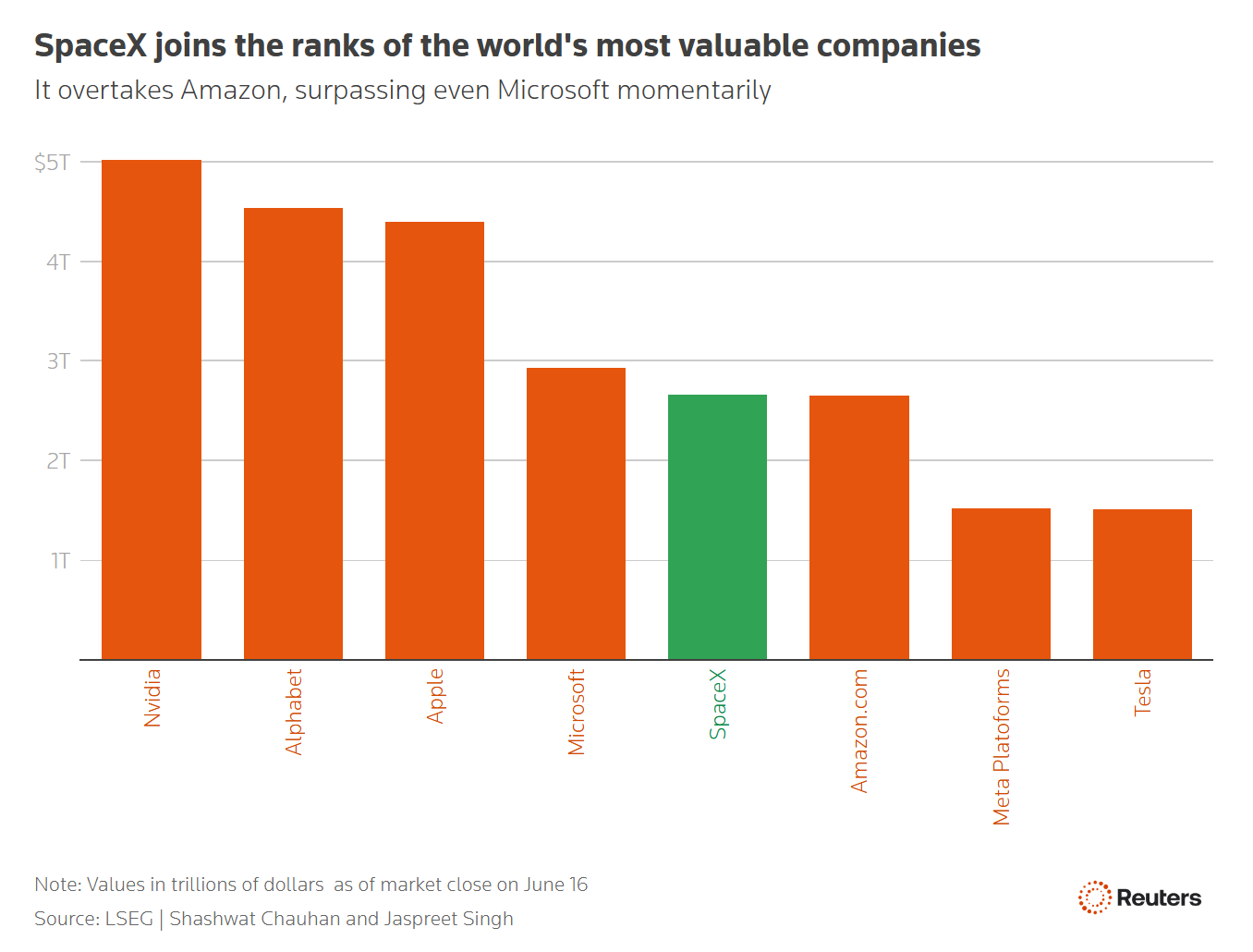

Meanwhile, pressure on U.S. tech stocks yesterday dragged the S&P 500 and Nasdaq lower, while the Dow closed at a record high for a second straight day. Despite that, Elon Musk's SpaceX continued to rise, closing up nearly 5%, surpassing Amazon's market valuation - and even briefly eclipsing Microsoft's. Wall Street futures are pointing up slightly before the bell.

Elsewhere, a cooler-than-expected UK CPI print on Wednesday showed that inflation there unexpectedly held at 2.8% in May. Coming one day before the Bank of England meets, this print provides more justification for keeping rates steady, which is what the BoE is widely expected to do.