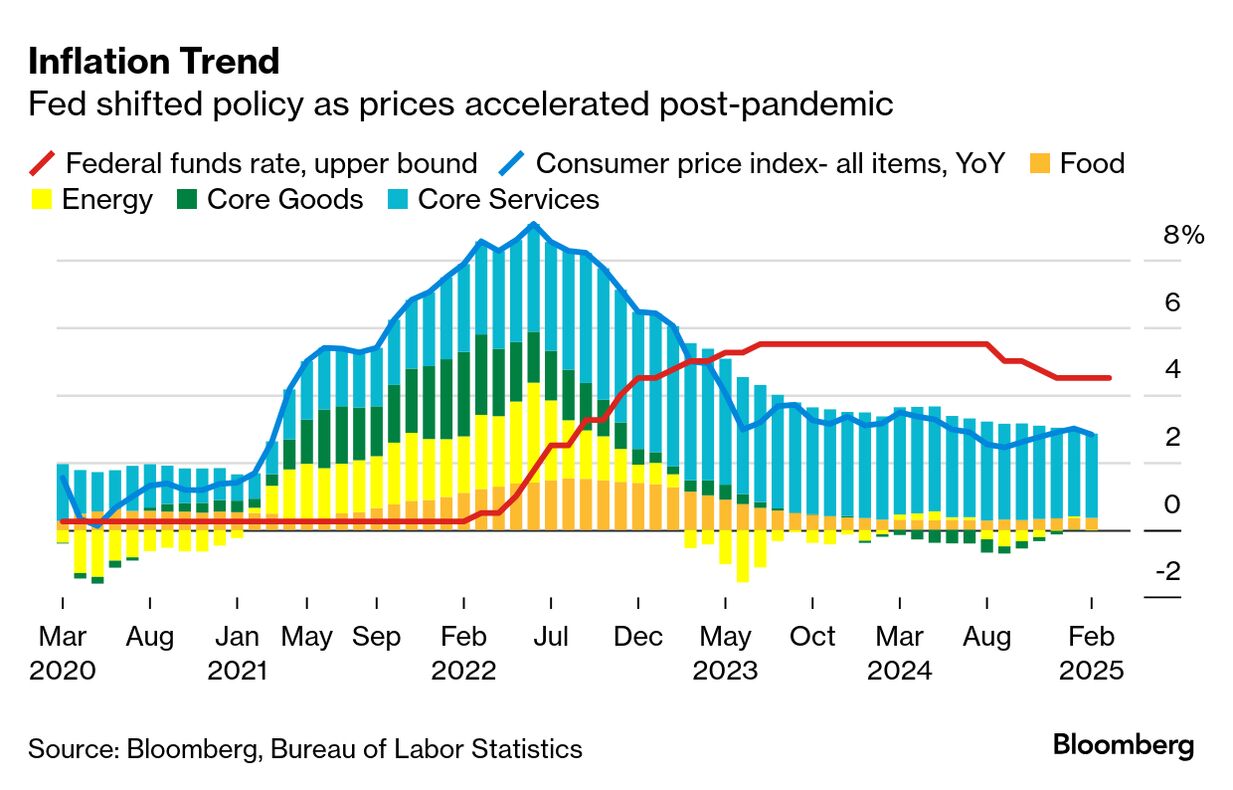

| I’m Katia Dmitrieva, Asia economics correspondent in Hong Kong. Today we’re looking at the world five years post-pandemic. Send us feedback and tips to ecodaily@bloomberg.net or get in touch on X via @economics. And if you aren’t yet signed up to receive this newsletter, you can do so here. This week marked a somber anniversary— five years ago, the World Health Organization declared Covid-19 a global pandemic. Managers may have told you to go home with a cheery outlook that things would get back to normal within a few weeks. Things did not get back to normal. In the following weeks, tens of millions of jobs were lost as businesses shuttered around the world, the S&P 500 and FTSE 100 indices plummeted the most since Black Monday in 1987. The rare plunge in both supply and demand ushered in the worst global recession in a century. While the WHO ended the pandemic designation about three years later, the effects on the world economy linger, with global output slashed by about $8.5 trillion through 2022 alone. The longer-term economic impact is perhaps most visible in labor markets, where many are still missing in action, partly due to health reasons or the increased shift to automation in the years after the pandemic hit. About 400 million people have developed long-Covid at some point in the past five years, representing about $1 trillion, or 1% of the global economy. As many as 4 million working-age people in the US alone are out of work due to these symptoms today. In some industries, workers continue to benefit from shortages, with wage increases and more job postings in retail and construction, for example. And those who hopped positions as economies reopened and employers grew desperate managed to hang onto those gains. Work also looks different now — at least in the white-collar space. Normalized during the pandemic, there are now more people working remotely, with the latest research showing about one-quarter of all workdays are now work-from-home. Those properties are also worth more now. Home price growth globally picked up, even in the first year of the pandemic, to 3.6% from 1.8% in 2019, as central banks embarked on a coordinated, once-in-a-generation easing cycle that made homeownership more affordable. Another resilient corner has been equities, particularly in the US. After the initial March 2020 dip, the S&P 500 recovered by late summer that year and has more than doubled since then. (Those gains are on the rocks recently as investors see President Donald Trump’s tariffs eroding demand and business investment just as the labor market weakens.) The boom in markets and real estate fueled the assets of the world’s richest. The top 1% of households now make up 36.2% of the world’s total wealth, up from 35.8% in 2018, according to the World Inequality Database. That’s compared to a loss for the bottom 50%. Meanwhile, five years on from first cutting rates and then reversing course as inflation soared, prices are still above where many monetary officials want them. There is one major similarity from the onset of the pandemic in 2020 and the world today, though, and that’s Trump. And just like his previous administration, his current approach is set to upend the economy and markets anew. The Best of Bloomberg Economics | - The ECB’s Lagarde warned of “severe consequences” from a trade war.

- Fewer Canadians are shopping in the United States after tit-for-tat tariff threats between the two countries.

- The US warned Vietnam to improve the trade balance between the two countries and further open up its markets, as a time of tariff risk globally.

- Japan’s unions win the largest pay hike in more than three decades, a positive sign for the central bank hoping to raise inflation.

- London’s luxury housing shortage is pushing buyers into fixer-uppers— including gut renovations.

- Two Polish central bankers think a rate cut in July is still possible, despite projections showing inflation pressures.

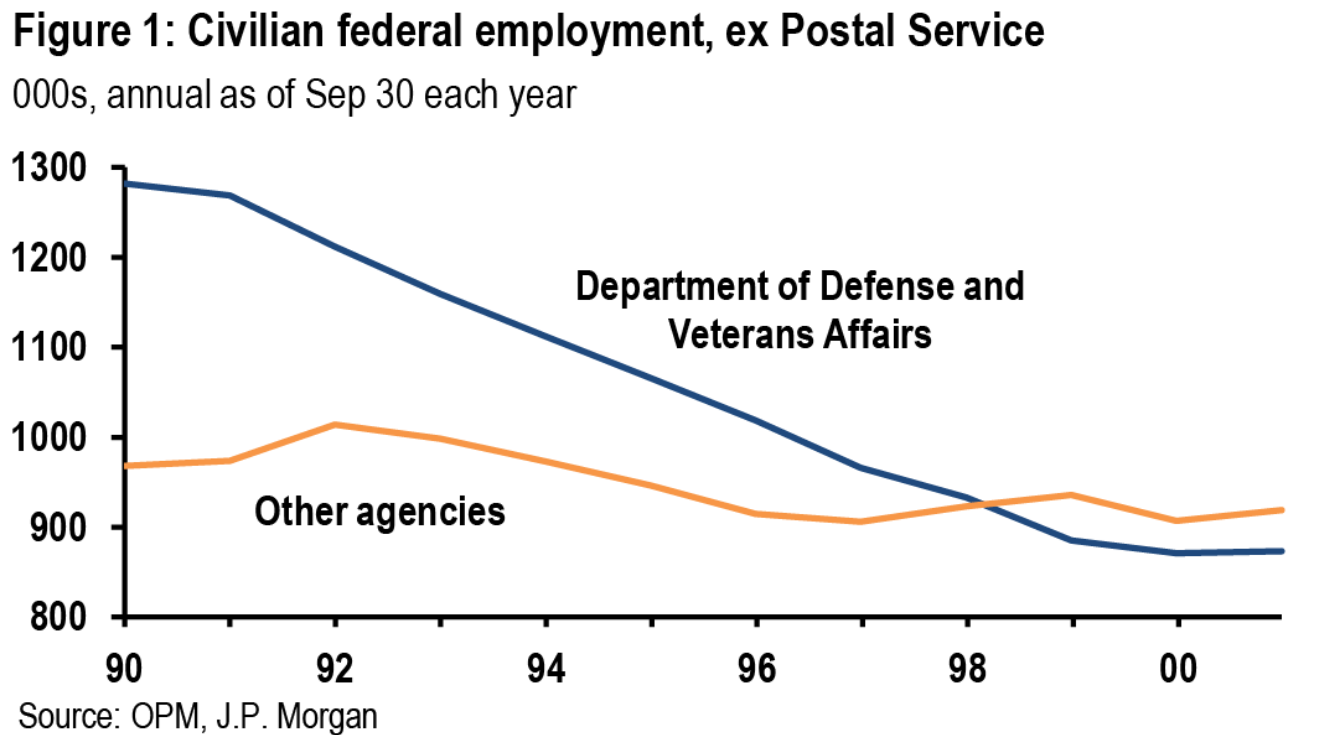

When the Trump administration began a push to downsize the federal workforce, it wasn’t the first time Washington has gone through major cuts in payrolls. As JPMorgan Chase economists highlighted in a recent note, there was also a concerted effort in the 1990s. Civilian federal employment fell by about 450,000 from 1992 to 1998, but the US jobless rate dropped steadily over that period and the economy enjoyed strong growth, JPMorgan’s US economists led by Michael Feroli wrote earlier this month. Part of the reason for the lack of impact is the reductions, by design, were spread out over time, making it easier for the private sector to absorb the workers. “Rhetoric and actions from the current administration suggests the desire to achieve cuts over a shorter timeframe and with greater use of layoffs,” they wrote. “Both of these points will make it harder for government employees to transition to other jobs.” Even then, the impact isn’t likely to be enough on its own to trigger a “major labor-market dislocation,” they said, “although this could depend on how far layoffs spread beyond government employees to contractors.” |