| I’m Malcolm Scott, international economics enterprise editor in Sydney. Today we’re looking at how China’s improving economic and market outlook contrasts with growing uncertainty over the US policy path. Send us feedback and tips to ecodaily@bloomberg.net or get in touch on X via @economics. And if you aren’t yet signed up to receive this newsletter, you can do so here. - US President Donald Trump’s aggressive trade policies have abruptly set the world onto a path of slower growth and higher inflation that could worsen notably if tensions escalate, the OECD said.

- The Federal Reserve faces a tricky task of both assuring investors the US economy remains on solid footing while also conveying policymakers stand ready to step in.

- The Bank of England is about to deliver its most hawkish decision since September as policymakers start to fret about building price pressures.

The “Trump put” is faltering right as the “Xi put” gathers momentum in what could prove to be a dramatic reversal in fortunes for the world’s two biggest economies if markets are correctly pricing in their respective outlooks. Goldman Sachs strategists see two key shifts across global markets in the past month: - A sharp re-rating lower of US growth in stocks, interest-rates and the dollar on the back of tariff volatility and policy uncertainty

- A sharp re-rating higher in the fiscal impulse in Germany fueling bets of quicker growth — a trend that’s playing out more modestly in China too.

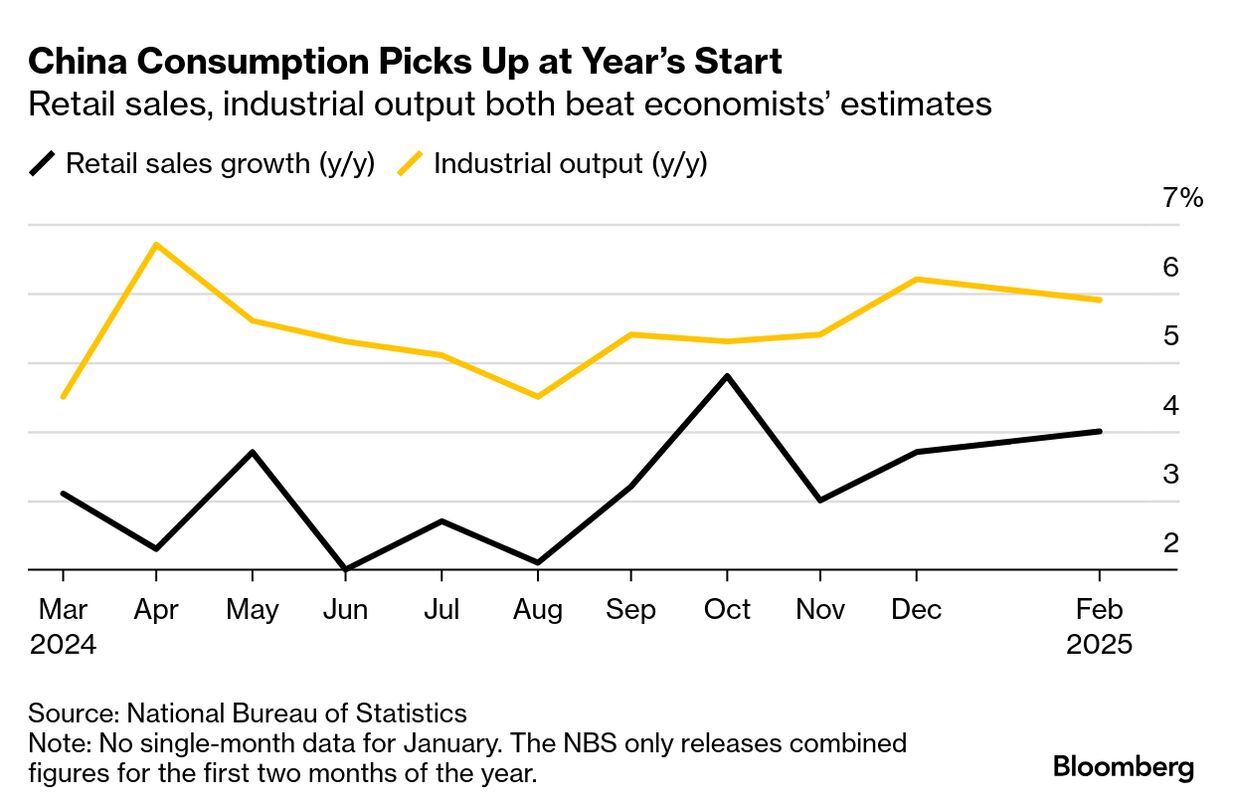

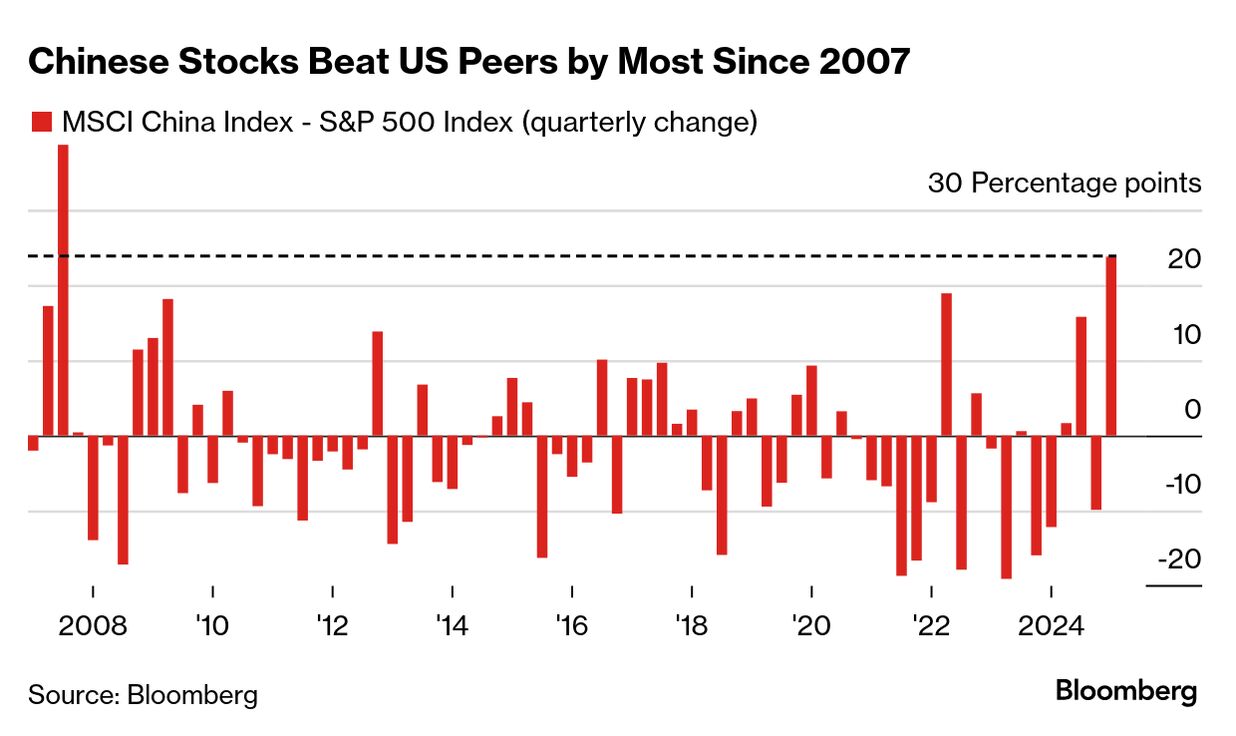

“Together, these two shifts pose a significant challenge to the narrative of US exceptionalism,” strategists Dominic Wilson and Kamakshya Trivedi wrote. Hours after that note dropped into inboxes, the latest rash of data from China showed the improved conditions seen in the last quarter of 2024 continued into the start of this year. Retail sales and industrial output both beat economists forecasts in January and February, prompting economists at ANZ Bank to push up their 2025 GDP call. Lifting consumer spending is key to countering the threat posed by Trump’s tariffs and their potential drag on Chinese exports, which contributed to nearly a third of the country’s economic expansion in 2024. To that end, Beijing has unveiled an action plan aimed at reviving consumption. The guidelines from a State Council report set out measures such as stabilizing the stock and real estate markets and offering incentives to raise the country’s birth rate. At a press conference Monday, a deputy head of China’s top economic planning agency said efforts to boost consumption will rely on measures that boost households’ income and boost their spending power, without providing specific details. The idea of a “Xi put” has been gaining traction in recent weeks as President Xi Jinping and his government have taken a more pro-market and pro-business stance. The latest example: reports that Global CEOs including Qualcomm’s Cristiano Amon and Saudi Aramco’s Amin Nasser will travel to Beijing for an annual gathering of top executives, with some expected to meet top leaders including Xi. Meantime, bets on a “Trump put” have faded amid a bruising selloff in US stocks that pushed the S&P 500 into a correction last week. Treasury Secretary Scott Bessent said he’s not worried about the recent downturn and remains fixed on the longer term. “I’ve been in the investment business for 35 years, and I can tell you that corrections are healthy, they are normal,” Bessent said Sunday on NBC’s Meet The Press. “I‘m not worried about the markets. Over the long term, if we put good tax policy in place, deregulation and energy security, the markets will do great.” But this year, it’s Chinese stocks that have been doing great. The MSCI China Index has soared about 20% in 2025; the S&P 500 Index has shed about 4%. Of course, stock market moves are just one of many barometers of economic health. But their gyrations also feed into both consumer and business confidence, so they can’t be ignored completely — especially if recent trends continue in months ahead. The Best of Bloomberg Economics | - The European Central Bank will lower rates two more times, according to analysts surveyed by Bloomberg who no longer expect borrowing costs to go below 2%.

- Japan’s largest labor union group said its workers secured the highest pay deal in more than three decades, supporting the case for further gradual rate hikes.

- Trump’s “Buy American” is supposed to alter consumer habits and bolster domestic manufacturing, but its long history reveals darker motivations.

- The Irish government is mounting a St. Patrick’s Day diplomatic offensive to try and calm Trump’s anger at “massive” trade surplus.

- Switzerland’s central bank is about to take another cliffhanger decision as officials weigh whether to use up one of their last rate cuts before reaching zero.

- Turkish authorities are using AI to track down money earned by psychics and fortune tellers as part of a broader drive to combat the informal economy.

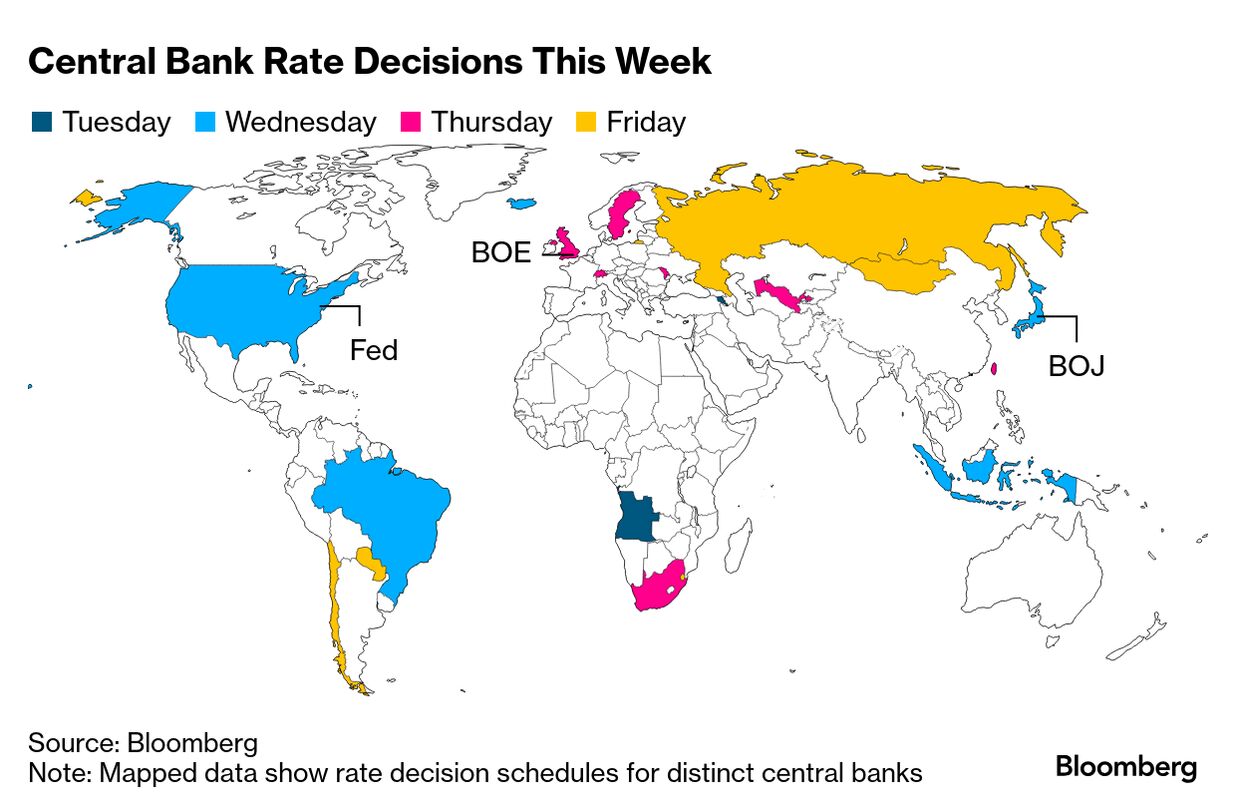

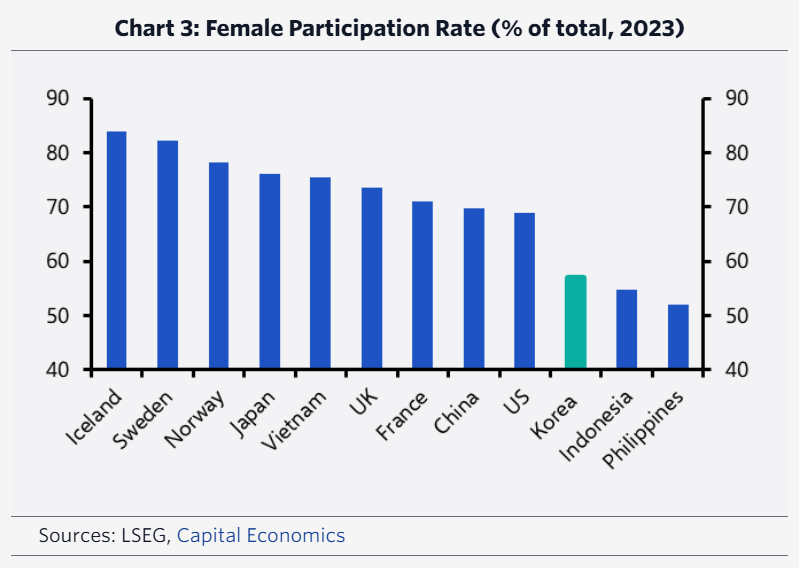

An anxious sense of wait-and-see may emerge from central banks in the coming week, in their first collective assessment of how US trade policies are impacting the world economy. With global tariffs now in place on steel and aluminum, and with Canada, China and the European Union all further suffering Trump’s ire, what were unrealized threats a few weeks ago have now emerged as full-blown hindrances to commerce. In all, officials responsible for half of the world’s 10 most-traded currencies, along with other Group of 20 peers, are poised to set rates over the coming days. See here for the rest of the week’s economic events. Asia’s fourth-largest economy, South Korea, has the world’s lowest fertility rate, leaving it on a dire long-term course, the nation’s central bank chief warned last week. But it’s at least making some progress in bringing more of its existing population into the workforce, Capital Economics notes. “The country is making important progress in bringing more women into the labor force as well as getting older workers to remain in employment for longer,” wrote Gareth Leather, the group’s senior Asia economist. “These developments are helping to offset a decline in the working age population” that Capital Economics has estimated will help send trend economic growth below 1.5% by 2050 from around 2.5% today. The share of Koreans aged 60+ in the labor force is now high by developed-nation standards, leaving little scope for further gains, but the female participation rate remains low, offering scope for improvement, Leather wrote Friday. “We expect the female participation rate to continue to rise over the coming years, which should ease the drag from the fall in the working-age population.” |