| The value of a nation’s currency can tell you a lot about what investors think of the government in charge and the economy it oversees. So the US dollar’s slump in recent weeks looks like a bad omen for President Donald Trump and the American economy. But there’s another reason a weakening dollar isn’t great for Trump and his team: The world’s reserve currency is doing the opposite of what economics tells you it should when the US raises tariffs sharply. Yes, that’s a sign markets are worried about what tariffs will do to US growth. It’s also, though, undermining the argument officials like Treasury Secretary Scott Bessent are making on who really bears the economic burden of tariffs. Read More: Bessent Says Recent Decline in Dollar Is a Natural ‘Adjustment’ The argument Bessent and others on Trump’s economic team offer is that the stronger dollar you would expect to come with tariffs means other countries’ weaker denominations leave their people with diminished purchasing power. That’s what economics tells you should happen. Though Bessent goes a step further and argues that, thanks to their weaker currencies, other countries pay the real price of tariffs. Yet most economists will tell you that US importers pay the actual tariff bill collected by Customs and often choose to pass the cost on to American consumers. Slumping Confidence There are plenty of signs the US public isn’t buying the Bessent argument, which is central to the idea Trump is selling that tariffs and the revenues they raise amount to a shifting of the US tax burden to offshore villains. Take a look at consumer sentiment gauges and recent polls. - On this edition of Bloomberg’s Trumponomics podcast, we try to understand White House economist Stephen Miran’s worldview and what it could mean for currencies and the global economic order

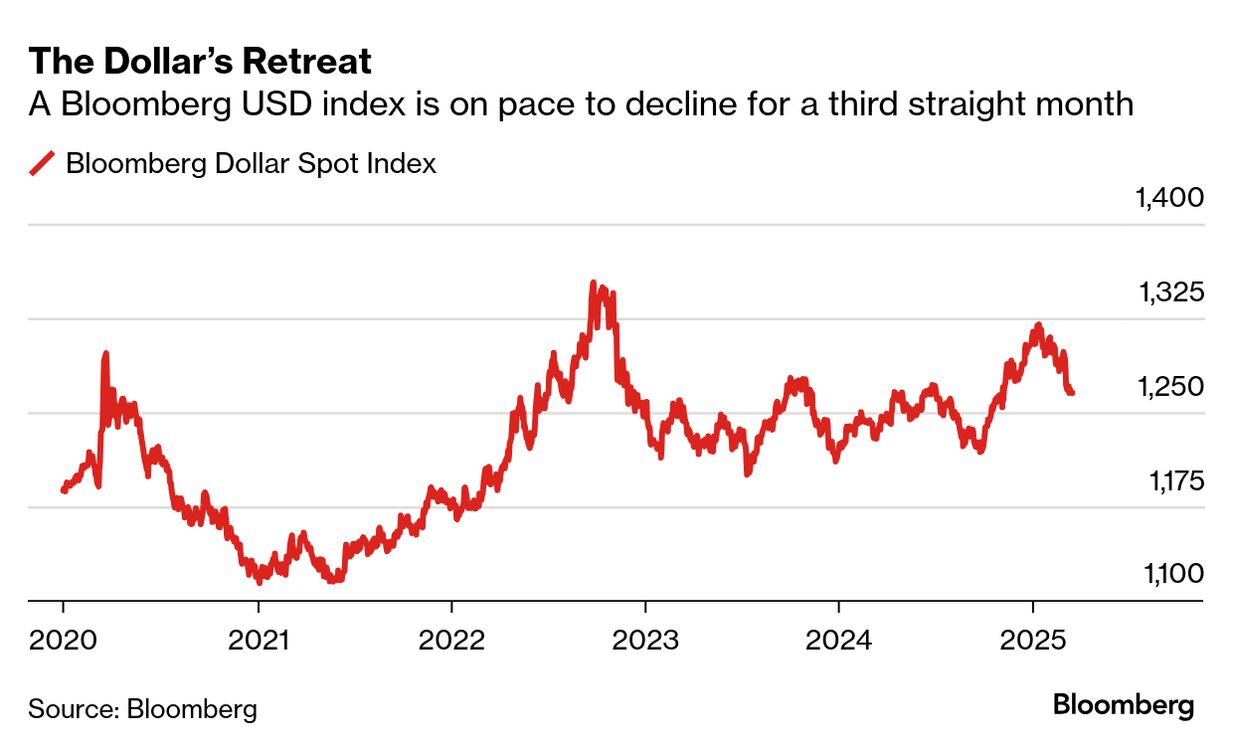

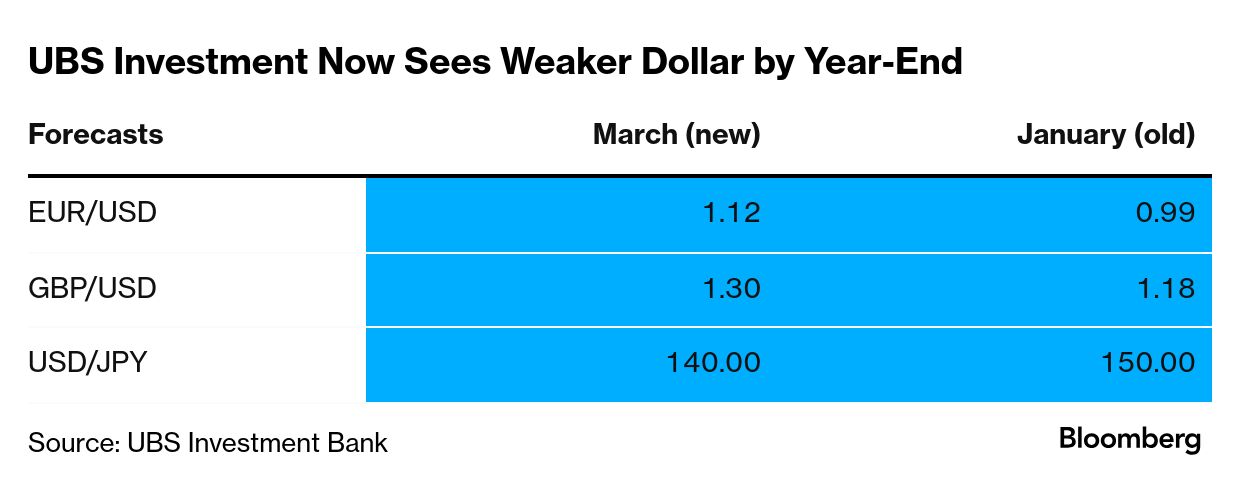

That isn’t stopping administration officials from making their case as they prepare for the rollout of Trump’s biggest tariffs yet on April 2, which Bessent on Sunday said “is going to be a big day.” “China’s manufacturers,” Bessent told NBC’s Meet the Press, will “eat the tariffs. I believe that the currency adjusts.” But what if the currency isn’t adjusting as expected? Since Trump took office the US has increased tariffs on all Chinese goods by 20%. Read More: UBS’ Weaker Dollar 2025 Forecast Resembles Pre-Election Outlook The rub is, of course, that China’s renminbi does not float freely. According to Bloomberg data, even if you go back to November and Trump’s victory, the heavily managed Chinese currency is only down 1.5%. Which means by Bessent’s definition Chinese manufacturers aren’t really eating the cost. True, free-floating currencies like the Canadian dollar and Mexican peso have weakened more. But even those currencies are down far less than the 25% headline tariffs they’ve been hit with would imply, even if you take into account the 30-day reprieve some imports have received. Tariff ‘Angst’ More broadly the dollar has been slumping. The Bloomberg Dollar Spot Index, which tracks the currency’s value against 10 major currencies, is down 1.7% in the past month. Against the Swedish krone the dollar is down more than 5%. ING head of Americas research Padhraic Garvey last week pointed to the slumping dollar as one signal of what he labeled “deep tariff angst.” Read More: Wall Street Battered Again by Trump Chaos as New Winners Emerge As Garvey wrote in his March 11 note to clients, earlier this year expectations of a 10% hike in US tariffs led to an equivalent rise in the dollar. “However, with 25%-50% tariffs we are in a very different situation and with the dollar now in fact falling against most currencies the mathematics simply don’t work,” Garvey wrote. American manufacturers have long complained about the impact of what they see as an overvalued dollar that makes US exports more expensive overseas. Trump has also at times called for a softer dollar to help manufacturing. Financial Accord That history has led to a conspiracy theory that Trump and his team are deliberately trying to weaken the dollar based on incoming economic adviser Stephen Miran’s published idea of a Mar-a-Lago Accord to do just that. But the broader suspicion of investors appears to be simply that Trump has miscalculated the cost of his import taxes. Which doesn’t bode well for April 2 as Trump introduces what he has branded “reciprocal” tariffs. Read More: Powell Faces Balancing Act Between Markets and Wait-and-See Mode The idea, as Bessent repeated Sunday, is to match with a single US duty trade barriers including tariffs, taxes and local regulations that US companies face overseas. Given Trump and his advisers have identified value-added taxes other countries collect as one target, it’s fair to expect a 20-25% number or higher. So will the dollar appreciate in response as Bessent expects? Maybe not, based on the recent evidence. Right now investors don’t seem to believe Bessent and his arguments on who will bear the real cost of tariffs. Instead, they see a slowing US economy bearing the burden of tariffs. —Shawn Donnan in Washington Click here for more of Bloomberg.com’s most-read stories about trade, supply chains and shipping. |