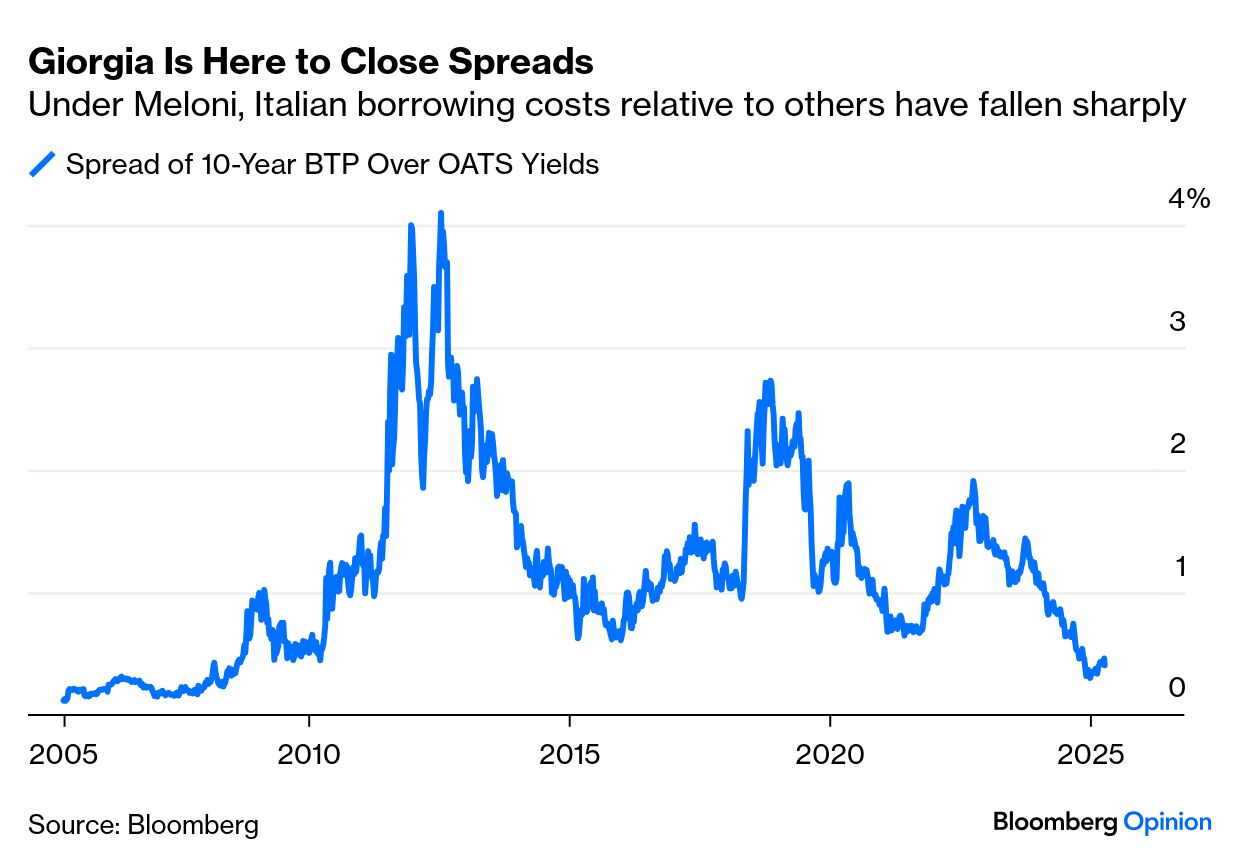

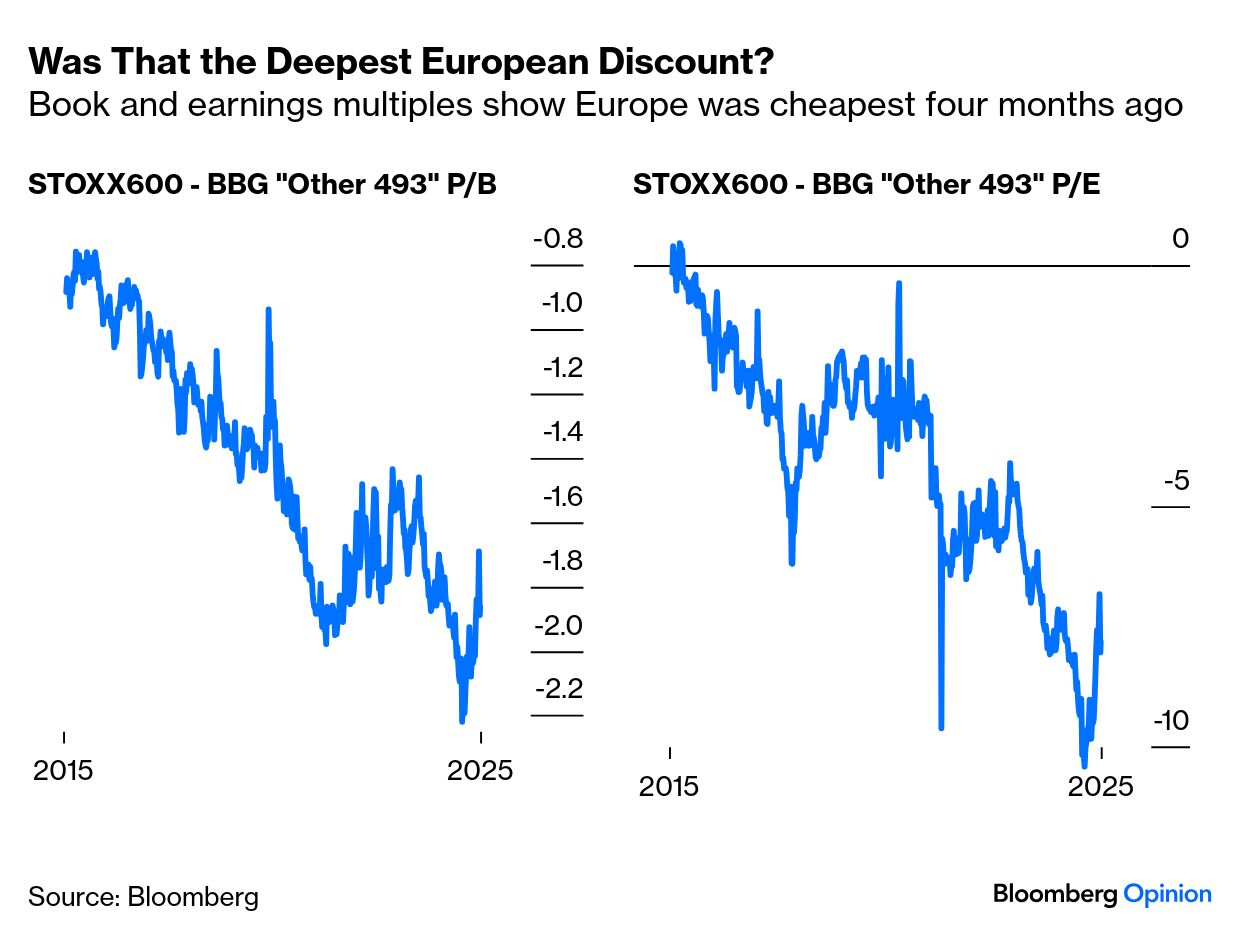

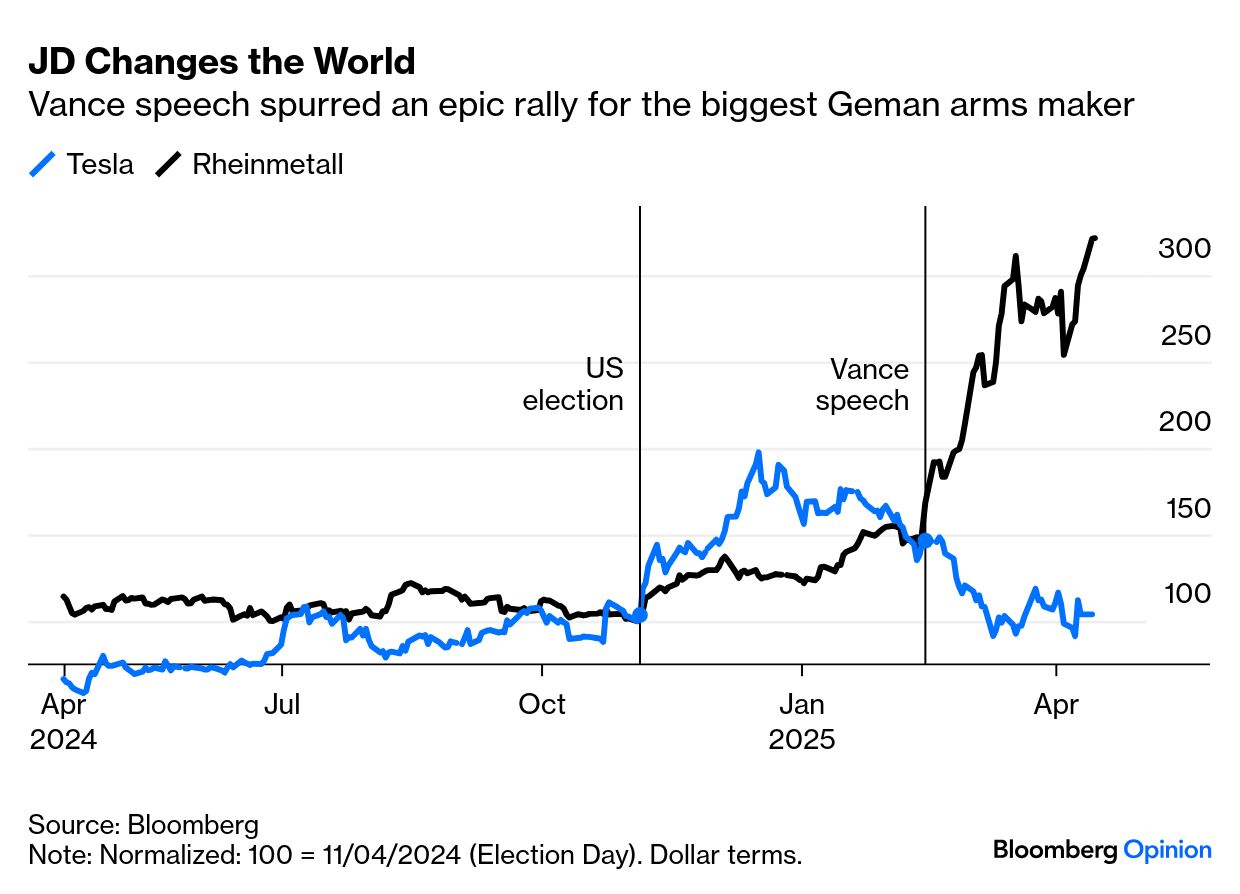

| There is no peace in the trade conflict, but there is something that might be called a ceasefire. That permitted some degree of normality in Monday trading, with US stocks ticking up (without a full-throated relief rally), while 10-year Treasury yields looked a lot less yippy, dropping 12 basis points. But the most intriguing move came in Germany, where bund yields are back where they were on the morning of March 4:  That day, Germans awoke to the news that the two traditional big parties, the Social Democrats and Christian Democrats, had agreed to amend the constitution to allow more borrowing. After many years of voluntary austerity, the sudden decision to borrow up to an extra $900 billion, in the cause of enabling independence from the US, was stunning, and it led to the biggest one-day rise in bund yields since reunification in 1990. Somehow, amid all the sturm und drang of the last month, yields have retraced all of that epic move. The bund market is essentially telling the German government to borrow what it wants, no problem. It’s also arguably healthy for the European economy that the tariff uncertainty hasn’t caused the bloc’s bond markets to fracture, as they did during the sovereign debt crisis a decade ago. Italy, with most problematic credit in recent years, received an upgrade from Standard & Poor’s last Friday. That was a big fillip for Prime Minister Giorgia Meloni, and brought the yield gap between Italy and France back down toward levels unseen since before the crisis in 2010: The market is still cautiously prepared to believe that Europe is getting its act together. The discount at which EU stocks trade to the US, measured by book or earnings multiples, hit a trough in December. The following chart uses Bloomberg’s index of the biggest 500 US stocks excluding the Magnificent Seven tech platforms: There’s also confidence that Germany — which has now thrashed out a coalition agreement — will spend much more money on arms, primarily from domestic manufacturers. Rheinmetall AG, the country’s biggest defense company, set a new high on Monday. It has trebled since the US election, going into overdrive since Vice President JD Vance’s provocative speech at the Munich security conference on Feb. 14. The contrast with the fortunes of Tesla Inc., poster child for Trumpism and the new economy, continues to be jaw-dropping: But will Europe really get its act together? That gets a critical test during the 90-day tariff delay that Trump decreed for negotiation. On issues of trade, the EU must negotiate as one — and it’s unlikely that even Meloni would break ranks — but it has to get its members to agree. Can it do so? Nico Fitzroy of Signum Global Advisors warns that this will be difficult as appetite for retaliation varies widely across the bloc, with France and the European Commission the most belligerent, and others less enthusiastic. Most don’t want to use the “nuclear option” of the Anti-Coercion Instrument, adopted in 2023 with a situation just like this in mind to allow direct action against countries deemed to be economically coercive. Other options include taxing US tech groups and other services providers. Fitzroy described the EU response to date as “extremely restrained beyond brasher rhetoric.” Its retaliation for steel and aluminum tariffs announced by Trump on March 12 has already been postponed twice — without any signs of further retaliation for the broader tariffs the US unveiled on April 2. The new German government still hasn’t taken office, which makes it harder to thrash out a position. But if a retaliation strategy is difficult, striking a deal with a US administration that believes the EU has mistreated it since inception will be no easier. Peter Navarro, Trump’s trade adviser, has said that any deal must include the bloc’s value-added taxes, which would almost certainly be a step too far. It’s possible that US intransigence over the next three months could convince reluctant Europeans into countermeasures. But at present, it’s hard to see how the EU can agree on either a decent deal or an effective punch back. European assets might well rally further, but they’ll need to pass this test first. |