| The conflict between Israel and Iran continues, despite Monday’s emphatic market bets that it was over. But the focus has changed. Initially the great fear involved Iran closing the Strait of Hormuz, a critical bottleneck for global oil supply. Following Donald Trump’s early departure from the G-7 summit in Canada, and presidential social media posts calling for civilians to evacuate Tehran, and then for “UNCONDITIONAL SURRENDER!,” the question has changed. Will the US expand the war by involving itself directly? And also, what would intervention aim to achieve? Another post suggested that the purpose might have shifted from preventing nuclear proliferation to attempting regime change: We know exactly where the so-called “Supreme Leader” is hiding. He is an easy target, but is safe there — We are not going to take him out (kill!), at least not for now.

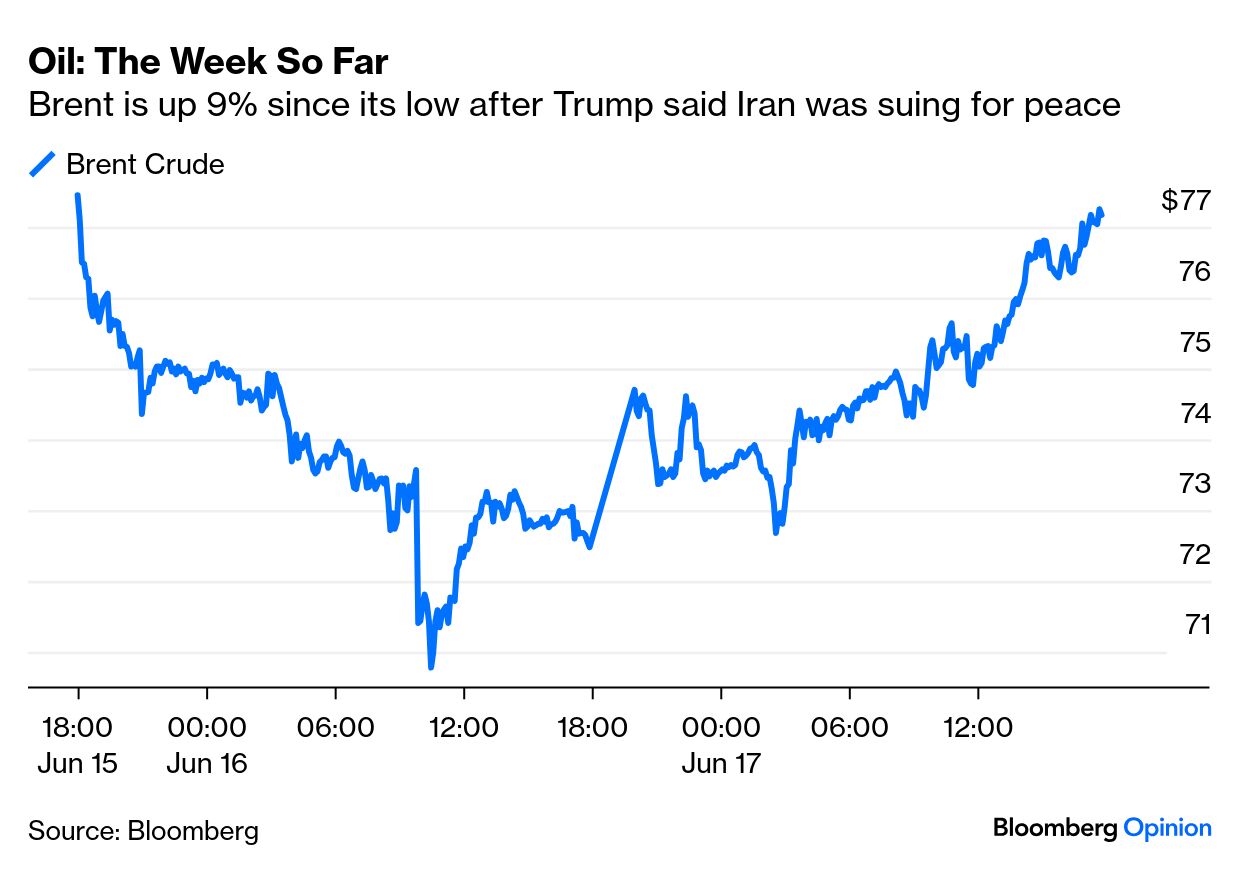

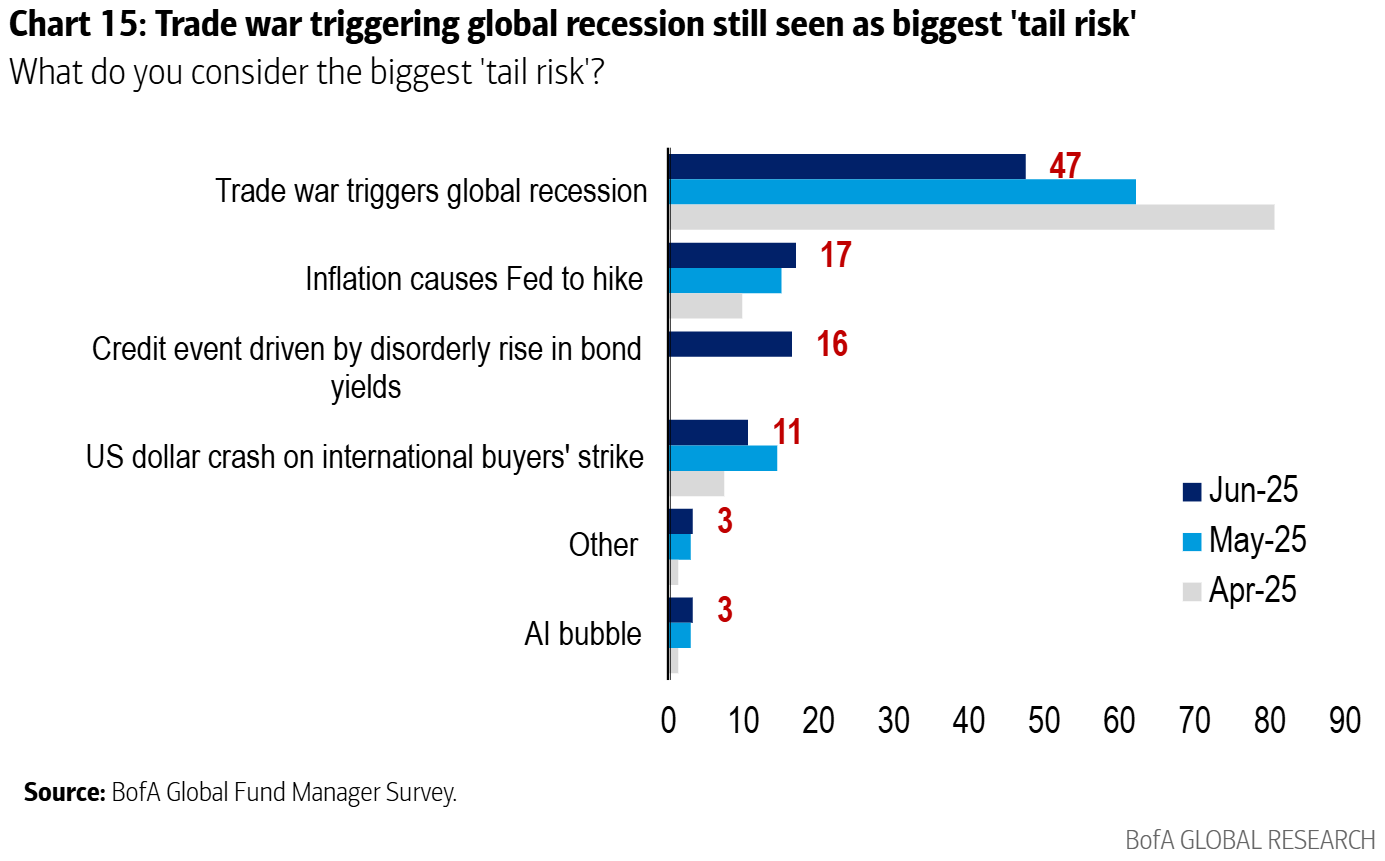

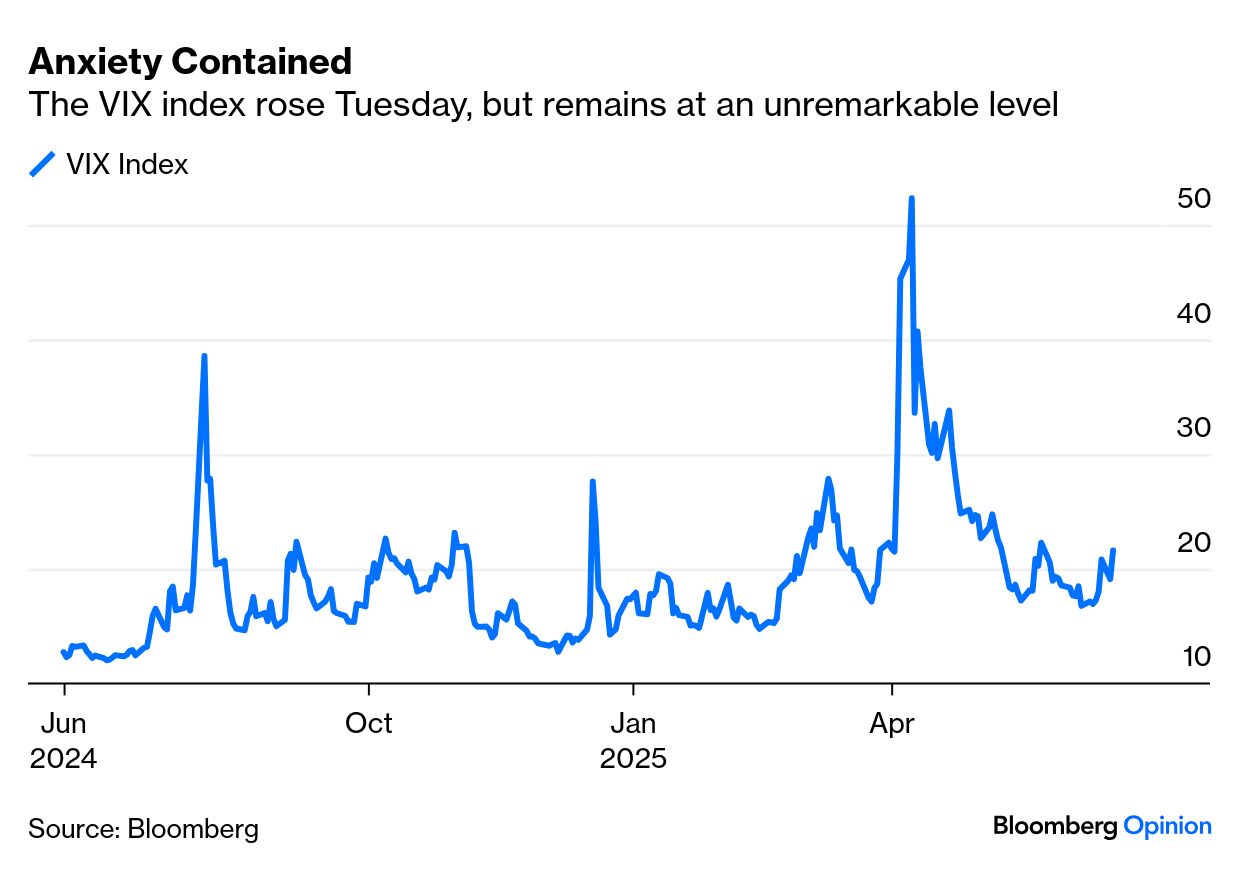

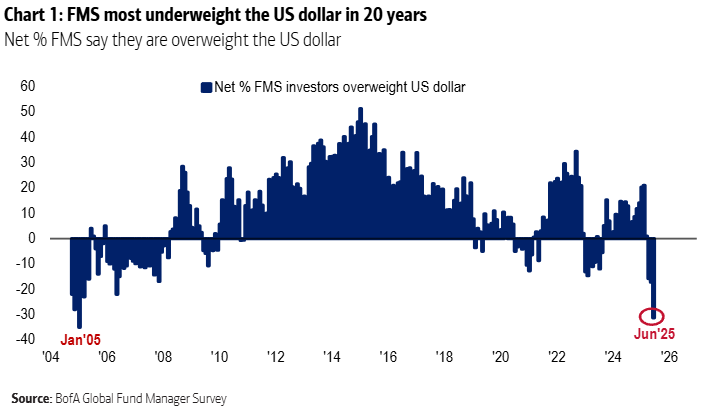

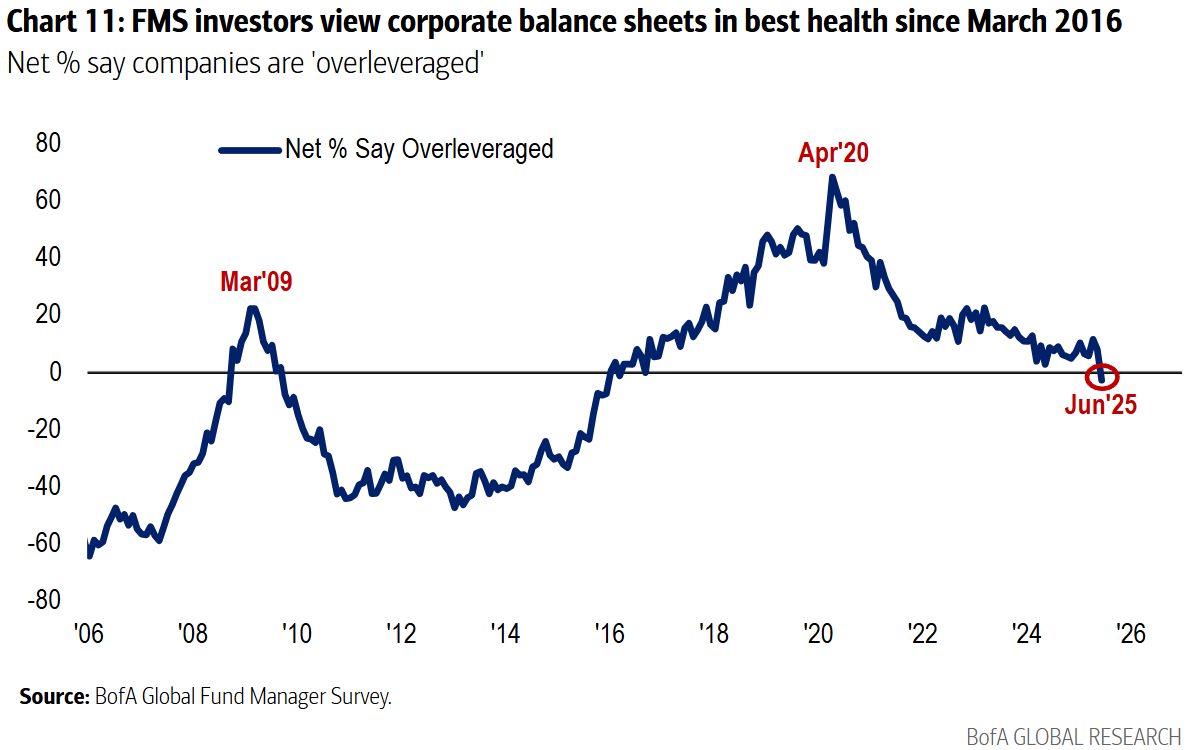

Multiple news reports now suggest that the administration is considering direct action. The main reason would be that destroying the remaining Iranian nuclear facilities, deep underground, would require huge bunker buster bombs (formally known as Massive Ordnance Penetrators) which only the US possesses, and would need to be delivered from US heavy bombers with US pilots. This appears to be the backbone of the contention by Israel that American involvement will be needed if Iran’s nuclear threat is to be neutralized. Without any physical escalation actually happening, yet, the composite effect was for the oil price to go right back to where it closed at the end of last week. In the process, any trader who bought at the bottom Monday netted a 9.25% profit in barely 24 hours: Another factor driving the volatility is that this development came as an almost total surprise. Fund managers had been worried about lots of things, but not about an attack on Iran. We now have the latest survey of global fund managers by Bank of America Corp., based on responses completed the day before Israel’s attack begin. Such an event wasn’t even mentioned when they were asked to name the greatest tail risk of the moment: Equities dipped on Tuesday, although not dramatically — the S&P 500 shed 0.84% — while equity volatility as measured by the VIX index jagged higher. These gyrations have happened with no obvious concrete new developments, driven instead largely by the news flow produced by the president on social media. Is this a sensible way for markets to try to deal with the risks? Christopher Granville of TS Lombard suggests that traders are too focused on attempts to handicap different outcomes, when the situation is more fluid than that. He argues: Day Five of the war (16-17 June) suggests a different perspective would be more useful – one that focuses less on outcomes and more on the process of attrition. This points to a pure volatility play, with frequent sharp (oil) market moves getting promptly reversed.

To show how this works, Tina Fordham of Fordham Global Foresight suggests that the market is treating the situation as an effective choice for the Iranian regime over its mode of demise: “Blaze of glory or humiliating capitulation?” This may not be a useful framework. Granville argues that the stakes on either of the two polar outcomes are so great that “much more military degradation and social tension on both sides will be required before one or other outcome goes live.” As the “blaze of glory” is suicidal for the regime, he says that “it would first have to be mortally wounded.” Capitulation would contend with regime infighting and the lack of any trust in the US as a counterparty. “Unconditional” presumably means giving up the ability to enrich uranium, and would be such a drastic defeat that some change to the regime would seem inevitable. For Tehran, it would be a last resort. There are further problems that go beyond the salutary lessons from Iraq and Libya. Fordham points out that the potential consequences of a fallen Iranian government were still not priced by markets. For example, as Europe and Turkey would have to absorb the fleeing masses, as happened during the war in Syria, “so the political risks aren’t limited to the oil price or the Gulf.” Andrew Bishop of Signum Global Advisors further argues that if regime change is truly on the agenda, it cannot happen for a while, and not until hostilities are over: The most salient impact of the war for Iran’s leadership and regime is likely to come after the war ends — with precedents suggesting that both autocratic leaders and regimes are particularly vulnerable to ouster in the months following a military defeat.

A final issue with regime change, if that is the aim, is that it will be hard to find one that is more palatable to Israel or the US. The National Security Institute’s Karen Gibson, a former general, told an event organized by Academy Securities that the prospect of a “US-aligned regime in Iran is really small,” as younger generations tend if anything to be more radical than their elders. “I don’t know how a non-Islamist regime would rise up.” It’s a complicated and deeply scary situation. The odds remain that this conflict will continue to generate enough twists and turns to make money for traders. That is little comfort for most of us. |