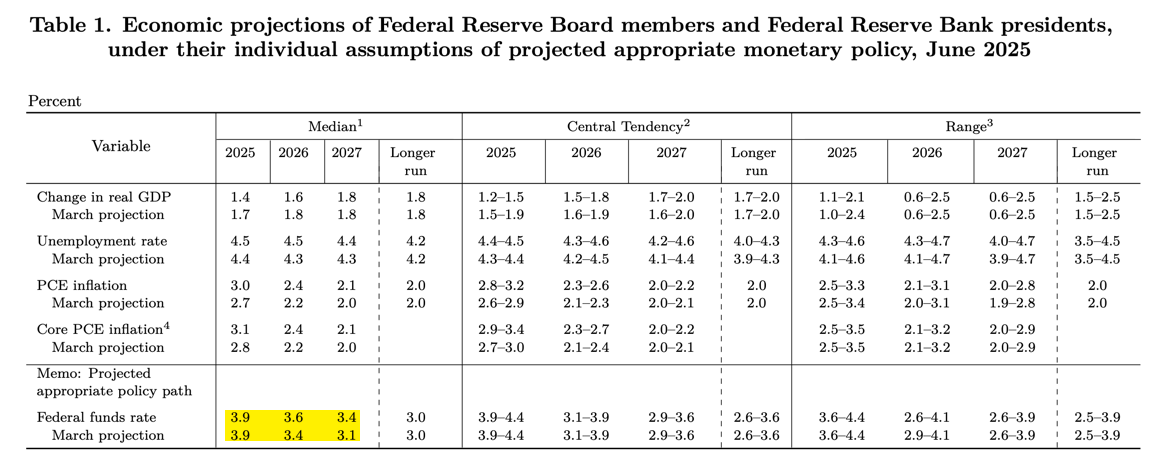

| If you combine that soft data with what the dot plot says about rate relief and Jerome Powell’s comments on Wednesday, it’s a dicey situation in terms of the economic support for corporate earnings. Given both the S&P 500 and Nasdaq 100 are near all-time highs, it’s clear US equity markets are expecting the data to improve. Since the recession scare in April, stocks had already rallied more than 20% before the Fed’s rate hold in June. Therefore, a bounce on stronger data in the near term should be muted. Still, the S&P 500 has stalled around 6000 for the last month as if waiting for a new upward catalyst. If you were to combine economic firming with tariffs in the 10-20% range for the EU, Japan and China, that could galvanize a wave of capital investment, and you have the makings of new all-time highs. Treasuries have been bid in part because of recent soft data. So, 4.50% for 10-year Treasuries and 5% for 30-year Treasuries that have acted as levels of resistance would be easy targets to hit in an upside economic scenario. The downside here is that given the market has already rallied so much, and expectations for a recession have plummeted, continued data weakness and bad tariff outcomes should trigger a considerable sell-off in US equities. We may not get the near-panic that took the S&P 500 below 5000 in April, but I would expect a correction in shares at a minimum. And all of that is very bullish for Treasuries, which should rally aggressively. July will be too early for the Fed | If we get the upside outcome that gets shares to new highs, it really won’t matter what the Fed does in July. They can continue to pause and shares will rally anyway. So what the Fed does after this week only matters if Trump brings back high tariffs. Trump’s hectoring of Powell suggests that the president is looking for policy cover. Perhaps Trump has already decided that he’s a “tariff guy” who is going to enact steep levies and needs fiscal and monetary policy easing to offset those tariffs as soon as possible. Therefore, you can picture a situation in July where the jobless claim data continue to worsen, pointing to the need for rate cuts from the Fed, but we also start the month with tariffs over 20% in some cases, more than double today’s baseline level. That would mean the Fed can’t cut for fear of inflation. That combination of rising inflation, slowing growth, and tighter policy would create a strong reversal in sentiment, and probably push the Fed to cut in September. Obviously, events surrounding Israel and Iran are a big wildcard that could keep the Fed on hold even longer, as military action there presents mostly upside risks for inflation via higher oil prices. In the downside scenario, since monetary policy acts with a lag, it would be too late to stop the US economy if it were on the way toward a recession. The best we could do is hope that lower interest rates ease the severity of a downturn and end it sooner. It would be ironic, though, if Trump’s unfailing belief in the power of tariffs tipped the economy into recession just when investors were least prepared for it to happen. |