| The Federal Reserve is always powerful. For decades, and certainly since the Global Financial Crisis, it has probably been the single most important driver of the world economy and markets. It hasn’t lost that role, but for the coming few months it is out of the driving seat. What happens next at the Fed is contingent on what happens on a number of other fronts. Thus, as Points of Return suggested last week, in deference to the Beach Boys, we need to wait all summer long for clarity on where monetary policy goes from here. The Fed left rates on hold, as universally expected and justified in the opening sentences of its statement: Although swings in net exports have affected the data, recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated.

As to where the Fed thinks it’s going next, the latest “dot plot,” in which each member of the committee gives an estimate of future fed funds, created the most interest. The median member still expects two cuts during the last four meetings of this year. That was hailed as good news initially by markets, but it’s difficult to make much of it. This is how the terminal breaks down the shift in the dot plot; gray dots are from the March meeting and the yellow dots are the most up to date. There are some subtle changes in there, but the obvious first reaction to this chart is accurate; it really hasn’t changed that much despite all the drama of the last three months: As might be expected, forecasts diverge more as we look further into the future. The rates market, as gauged by Bloomberg’s World Interest Rate Probabilities function, has consistently predicted that fed funds will be somewhere between 3.0% and 3.25% by the end of next year. That implies a couple of more cuts by then than the Fed currently predicts, which in turn suggests that traders are more worried about growth than the central bankers are: When it came to economic projections, the dots showed the central bankers growing slightly more negative about growth prospects for next year, while also expecting slightly higher inflation — so stagflationary at the margin, and neutral when it comes to the direction of the next rate move. Somehow, all of this was taken as dovish enough to prompt a lot of people to buy two-year bonds, which are sensitive to the fed funds rate. But the press conference by Chair Jerome Powell, which started 30 minutes later, reversed almost all of it: The critical passage from the Powell remarks that moved bond yields back upward was this one: Ultimately the cost of the tariff has to be paid, and some of it will fall on the end consumer. We know that’s coming, and we just want to see a little bit of that before we make judgments prematurely.

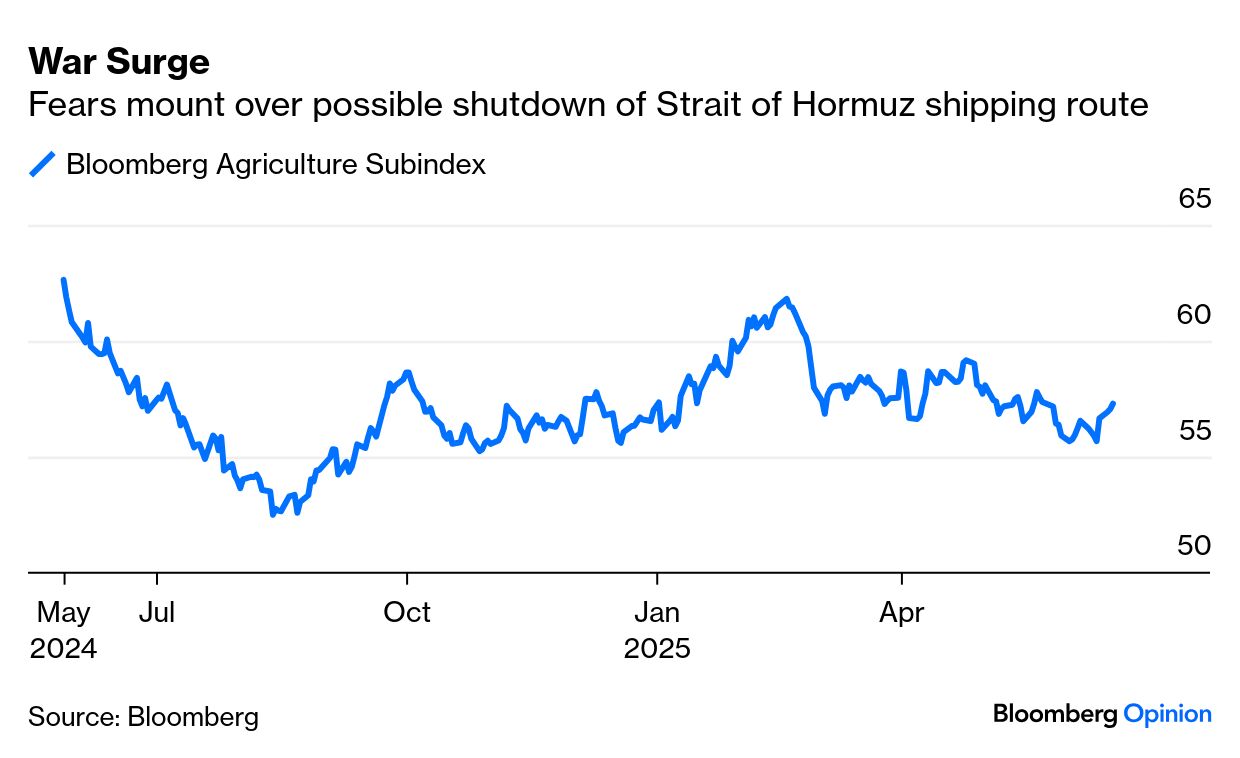

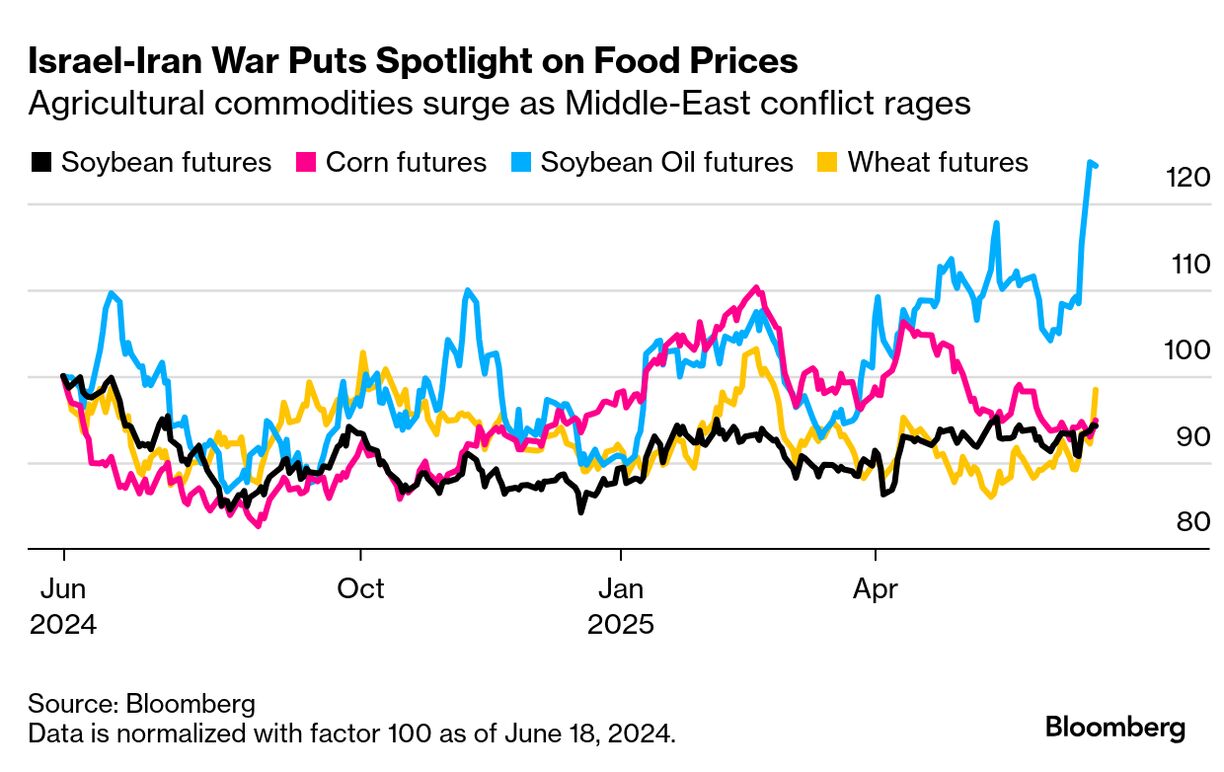

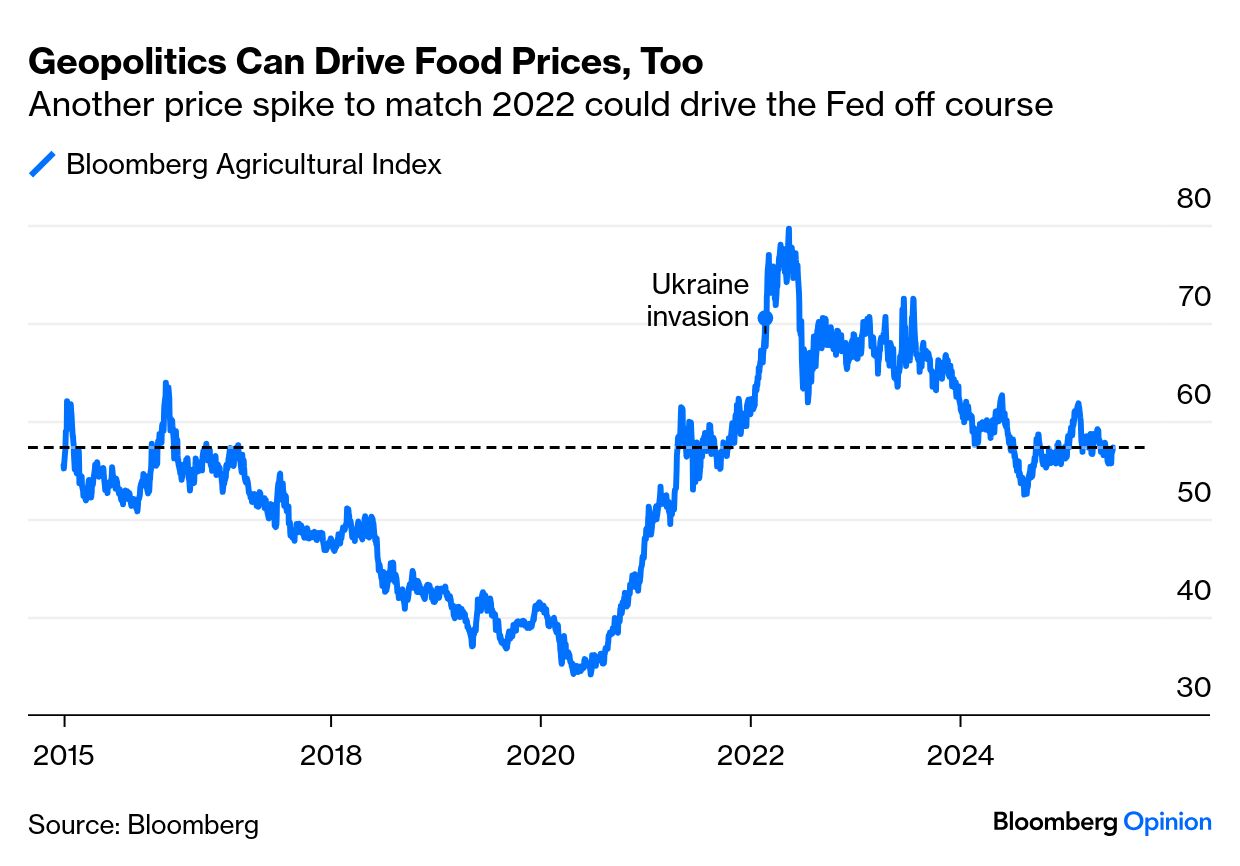

Until the Fed is really confident that tariffs haven’t triggered a significant bump in inflation, in other words, it’s going to have to stay on hold. The risk of a commodity price spike created by the Middle East conflict adds to the arguments to wait and see. To quote Standard Chartered Plc’s Steven Englander, we should “take the summer off.” Englander also suggests that Powell is implicitly arguing for fewer than two cuts this year: Given the absence of references to softer activity, and how frequently he referred to price increases from tariffs, we think it is possible that Powell was among those who saw zero or one cut.

The Fed chair is only very rarely outvoted, so it’s significant if he is now one of the hawks. All of this, however, goes beyond the broad outline that nothing the FOMC announced made any change of any significance to the likely course of rates ahead. The committee obviously didn’t want to move the needle, and it succeeded. Once there is clarity on the Middle East and on tariffs, then it can be more active. For now, it’s overseeing low unemployment, declining inflation and booming asset markets, despite everything. For both stocks and bonds, this was an unusually quiet FOMC day, with the S&P 500 closing down 0.03%, and the 10-year bond yield unchanged. Oh for such calmness and predictability in the Middle East. |