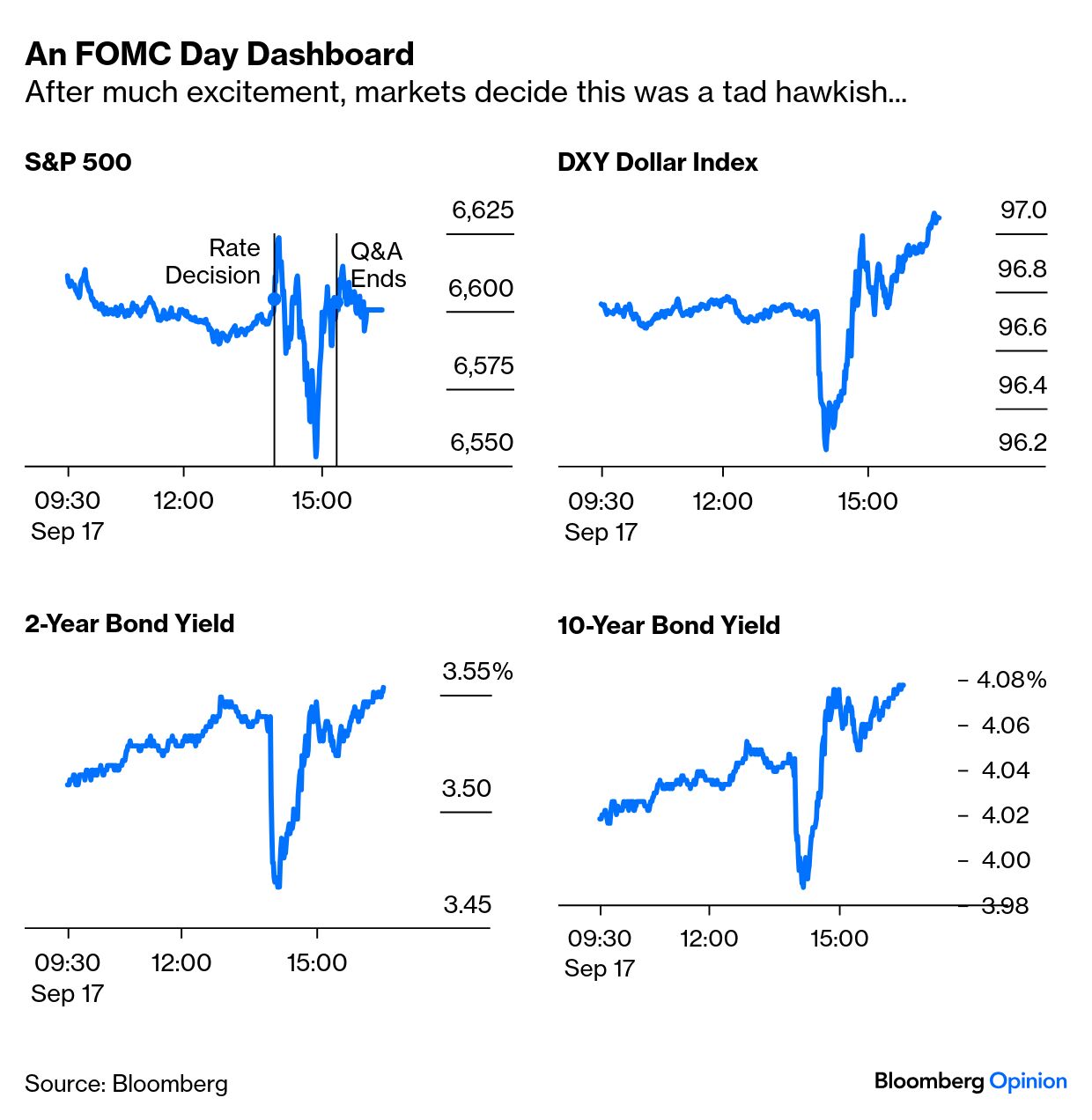

| There was no jumbo 50 basis-point cut from the Federal Reserve. More surprisingly, only one governor — new arrival Stephen Miran, who had only just gotten his feet under the desk — wanted one. Everyone else coalesced around a more moderate 25 basis-point easing. Like Sherlock Holmes’ dog that didn’t bark, that lack of dissent may be the most curious incident of one of the weirdest Federal Open Market Committee meetings in memory, and offers the most important clues for the future. By the end of trading in New York, the market had come to a collective judgement that at the margin, the Fed was somewhat more hawkish than had been expected. Traders only came to this conclusion after some wild gyrations, but stocks and two-year bond yields ended barely changed while the dollar and the 10-year yield rose a bit — classic signs of a “hawkish cut:” What they said Chairman Jerome Powell used his press conference to increase the weight the Fed gives to the employment side of the mandate, rather than inflation. With both rising, that’s a clear indication that the central bank thinks it might have to be more lenient in future. Critically, he could “no longer say” that the labor market was “very solid.” He added: Labor demand has softened, and the recent pace of job creation appears to be running below the breakeven rate needed to hold the unemployment rate constant.

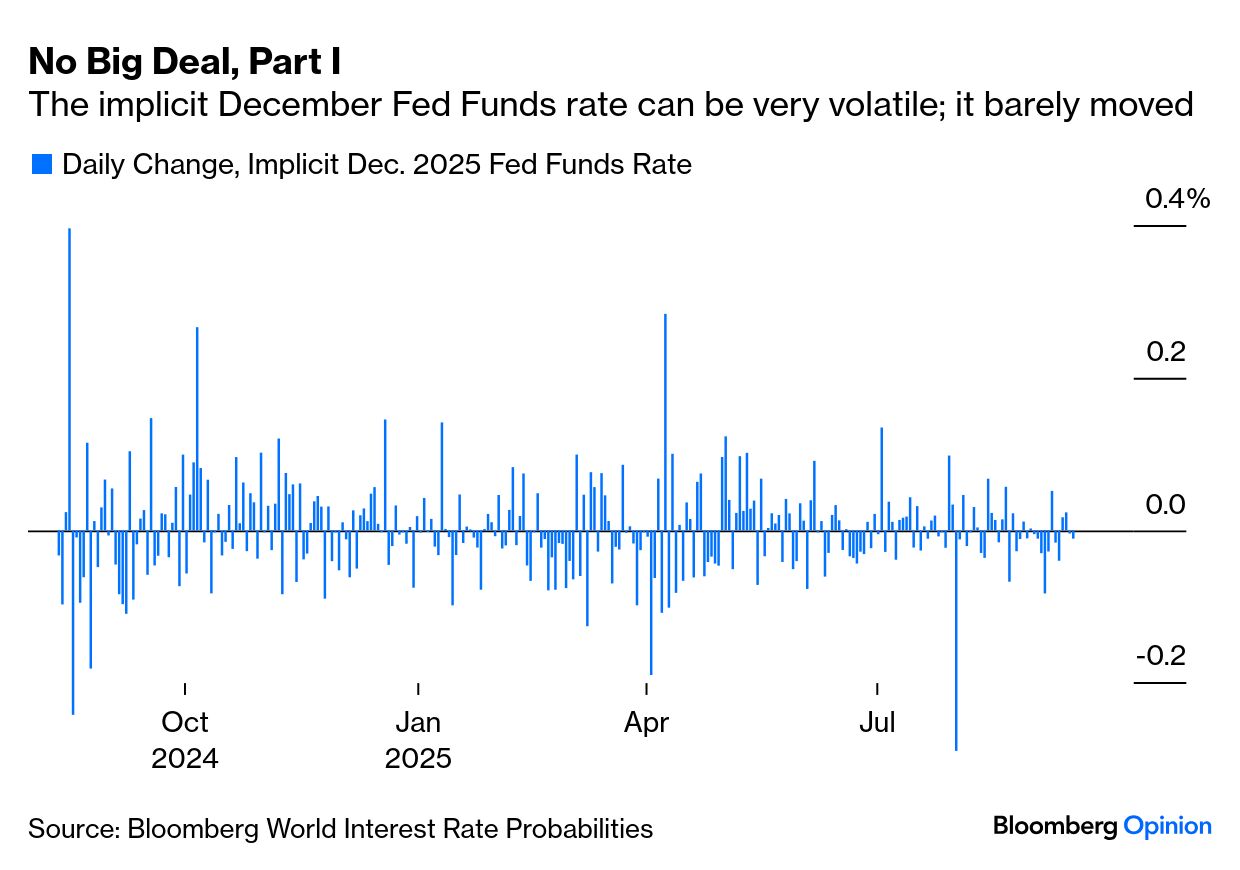

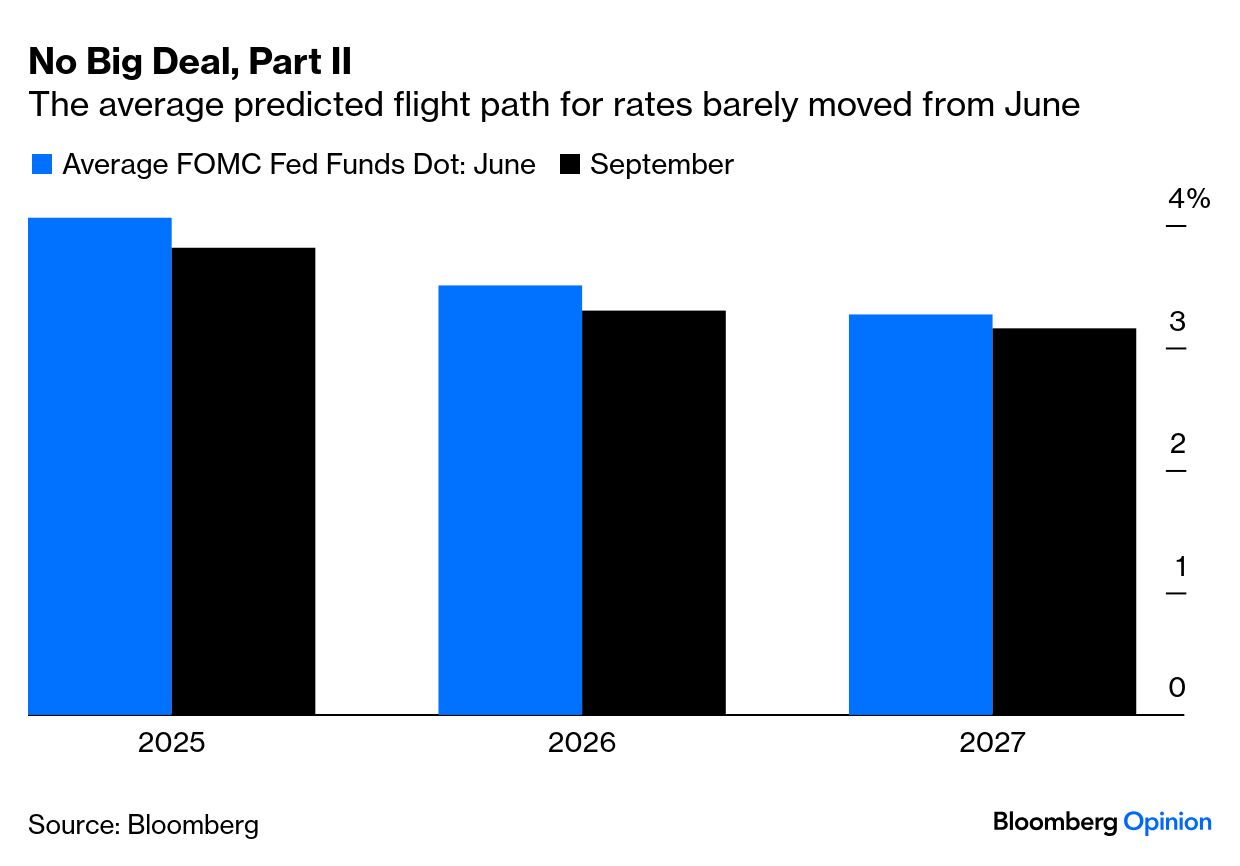

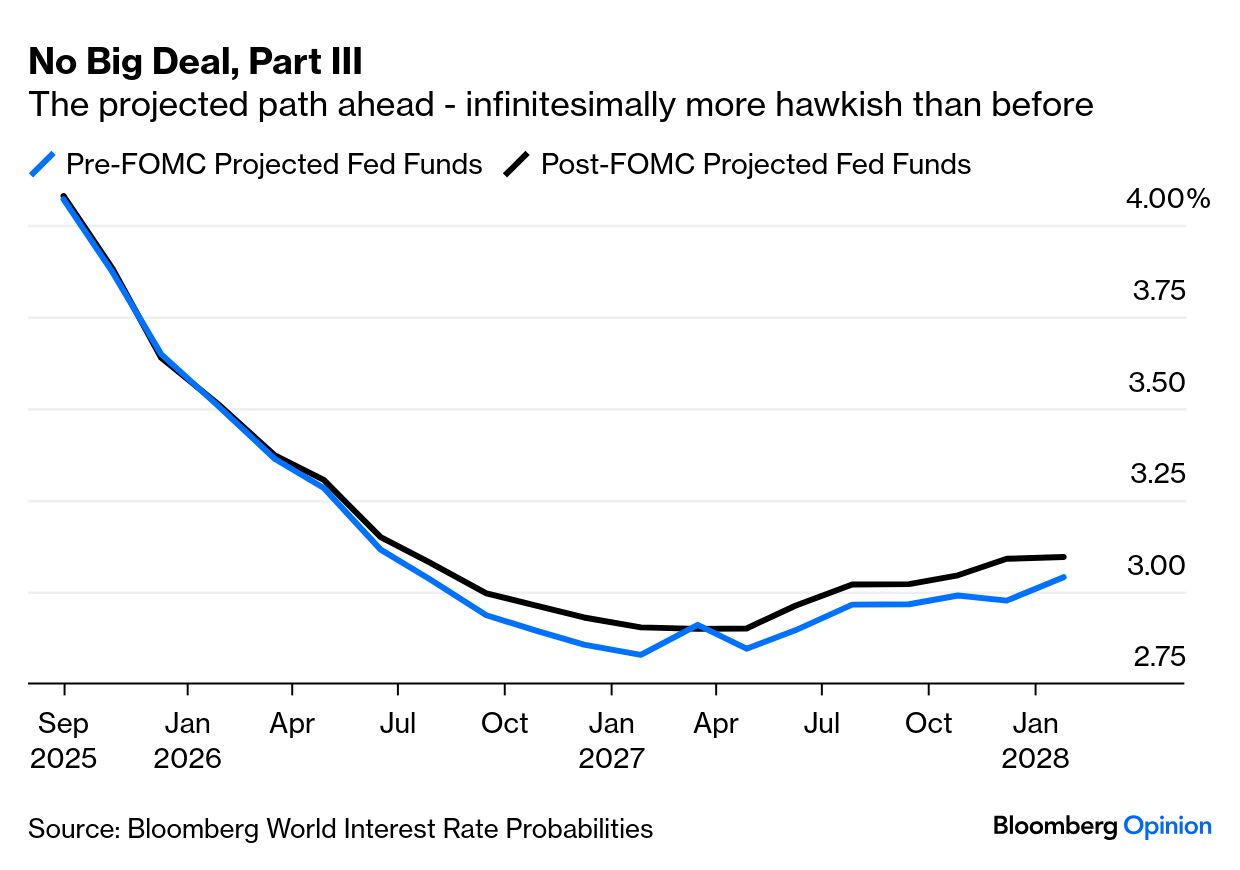

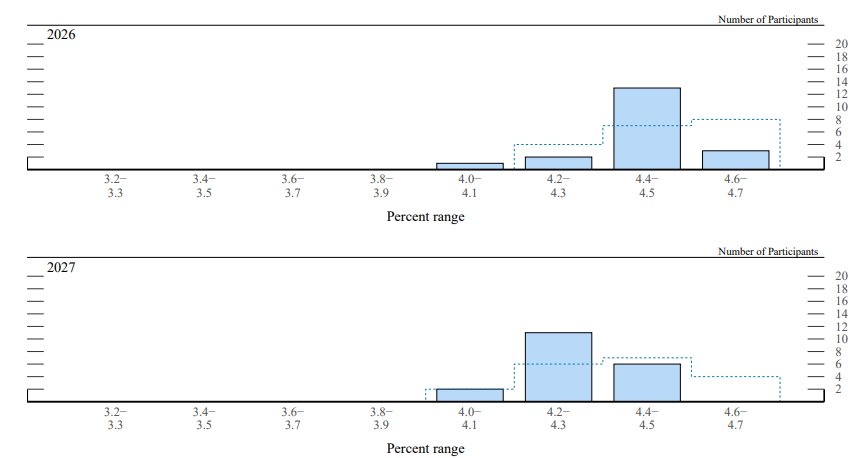

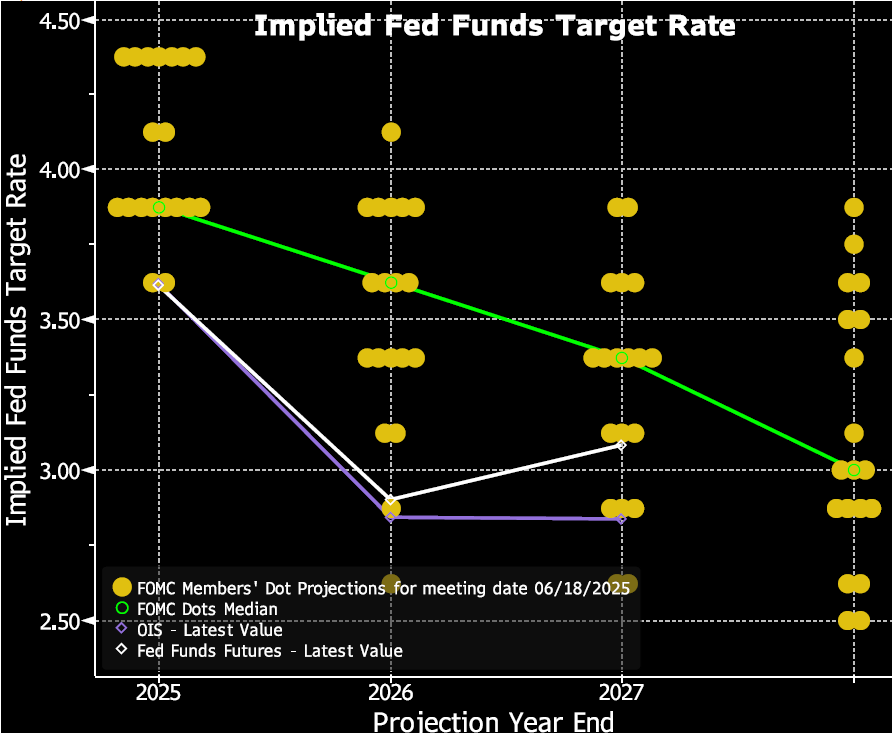

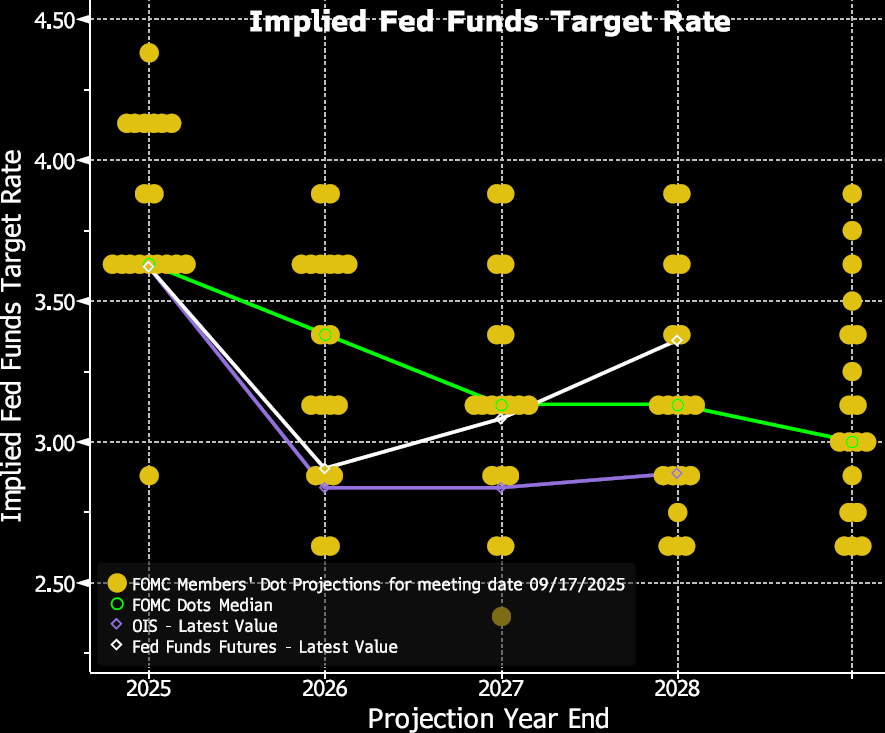

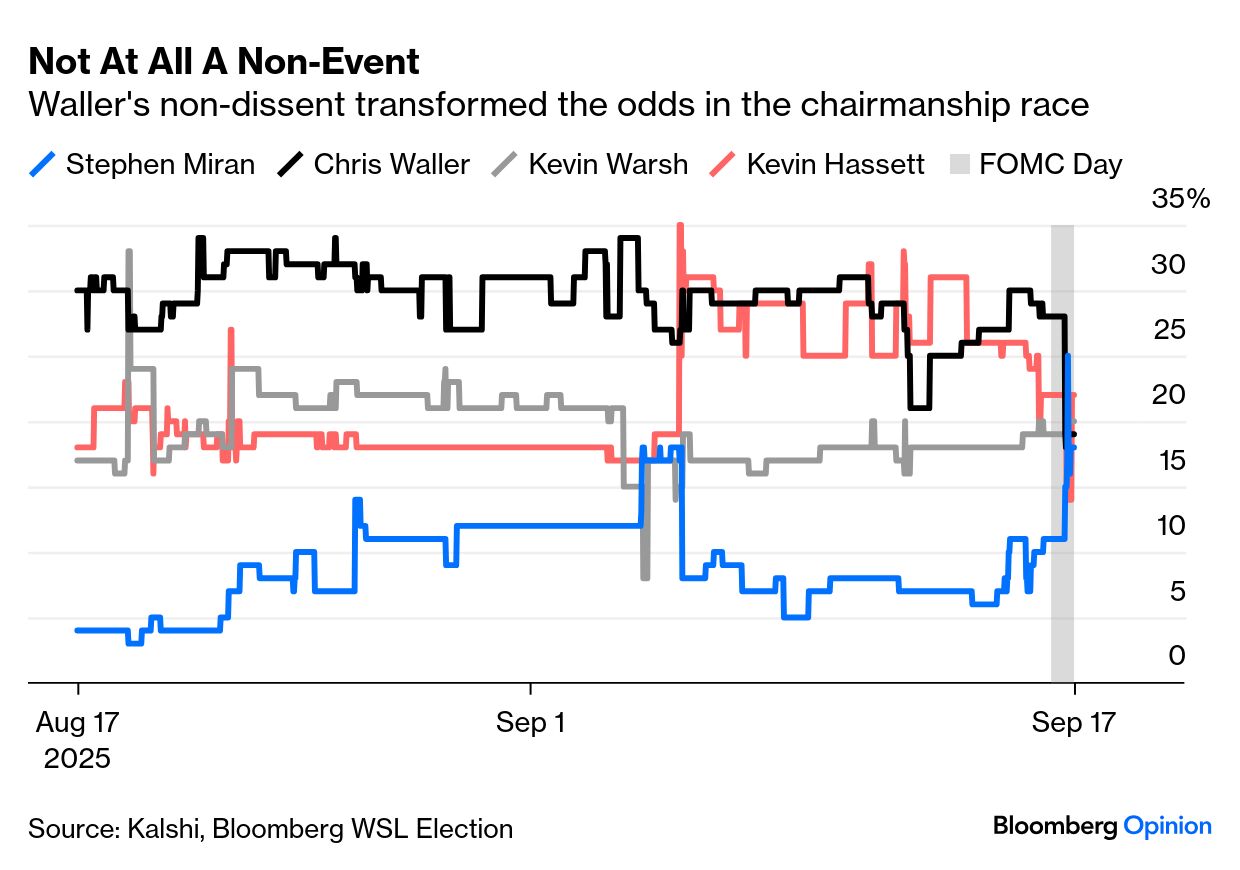

But he spent even more time ramming home that there were no guarantees. The FOMC is in a “meeting-by-meeting situation,” and this was a “risk-management cut.” In comments with which no sentient human being could disagree, he added that “it’s challenging to know what to do,” and “there are no risk-free paths now.” Why it doesn’t resolve much This meeting left little decided. That’s why key markets hardly moved. There is a shoe to drop, but it hasn’t dropped yet. Most obviously, the fed funds futures’ implicit prediction for the rate at the end of this year barely budged. It’s a volatile series, with huge moves after FOMC meetings or big data releases. This Fed Day didn’t register: Looking at the “dot plot” — the quarterly exercise in which all the Fed governors and regional presidents give their estimates for the future path of rates and for the main economic variables — again, it’s the lack of movement that stands out. This is how the mean (not the median) of the FOMC’s predictions for fed funds rates at the end of each of the next three years has shifted since the last dot plot in June: Yes, the move is toward lower rates, but it’s oh so gentle, and the majority of the committee expects its target rate to stay above 3% through to the end of 2027. Bear in mind that President Donald Trump is on record favoring 1%. Fed funds futures concur that very little changed. Traders continue to think that the FOMC will have to cut more than the dot plot implies, but this meeting nudged expected rates up slightly, not down: Those dots in detail Two other points need to be made about the dot plot. First, although the Fed is more nervous that unemployment could take off, the average governor now thinks joblessness will be slightly lower than they did in June. In the chart below, taken from the FOMC’s press release, the dotted line shows how many participants expected different rates of unemployment in June, while the solid bars show their expectations now. For both 2026 and 2027, they’re lower: They’re nervous about the labor market, but on balance don’t expect it to deteriorate significantly. Meanwhile, the single most startling revelation of the day was perhaps not as significant as it looked. There was a dramatic outlier. Although the dots are anonymous, there can be no doubt that it’s Miran. In June, nobody thought rates would drop as far as 3.5% by the end of year. This month, there is one voter who expects rates to drop below 3% by then — although the rest remained unchanged: It’s only for this year that Miran is such a clear outlier. This looks like a gesture more than anything else, and it’s hard to take seriously. Miran has complained, with some justification, that the Fed is infected by groupthink, and greater diversity of views is helpful. But he is predicting the kind of move in three months that historically only happens at times of financial crisis. He might have had more influence over his new colleagues if he hadn’t suggested something so extreme. What really mattered Governor Christopher Waller dissented in favor of a cut at the July FOMC. That helped him build a strong candidacy to take over as chairman when Powell stands down next year. Prediction markets had him as favorite. He must surely have known that his chance of getting the top job, which is effectively in the gift of Trump, would be helped by voting for a jumbo cut. But he didn’t. Neither did Michelle Bowman, another governor who dissented last time and also has a shot at the chairmanship. In consequence, one market was totally shaken up by the afternoon’s events in Washington: the betting market for the Fed chairmanship. This is how the Kalshi futures market has viewed the odds on the three leading candidates — Waller, chair of the National Economic Council Kevin Hassett, and former Fed governor Kevin Warsh — along with those of Miran, over the last month. Out of nowhere, Miran briefly took over as favorite after he dissented, but Waller did not: We can assume, given that it’s natural for both of them to want the top job, that Waller and Bowman voted the way they did because they thought it was the right thing to do. The case for drastic rate cuts from here is far, far weaker than the administration wants us to believe. Their actions have significance that goes beyond the race for the chairmanship. Waller and Bowman will still be governors next year. In February, the seven governors based in Washington have the chance to veto nominees for the presidencies of the regional Feds. That could, in theory, be the moment when a group of four Trump appointees (Miran, Waller and Bowman, and a successor for the embattled Lisa Cook) ensures a pro-Trump majority for the whole FOMC. Cook’s firing still needs to pass muster with the Supreme Court. Even if she goes, today’s events indicate that the chance of an imminent White House takeover of the Fed have been overdone. By not dissenting, Waller and Bowman showed they may not be willing to play the role of obedient political stooges. Like Holmes' dog that didn't bark, that's very significant. For those who value central-banking independence, it was a good day. |