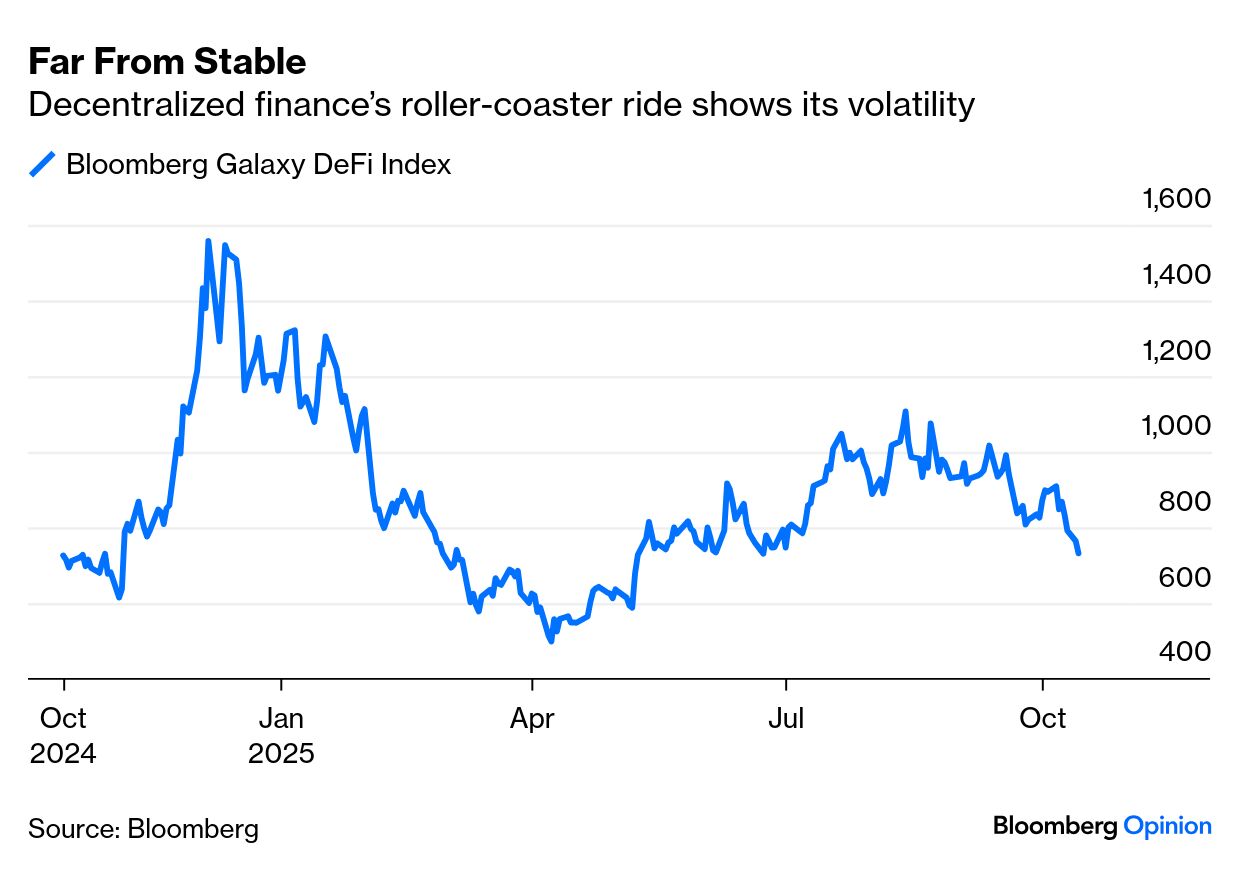

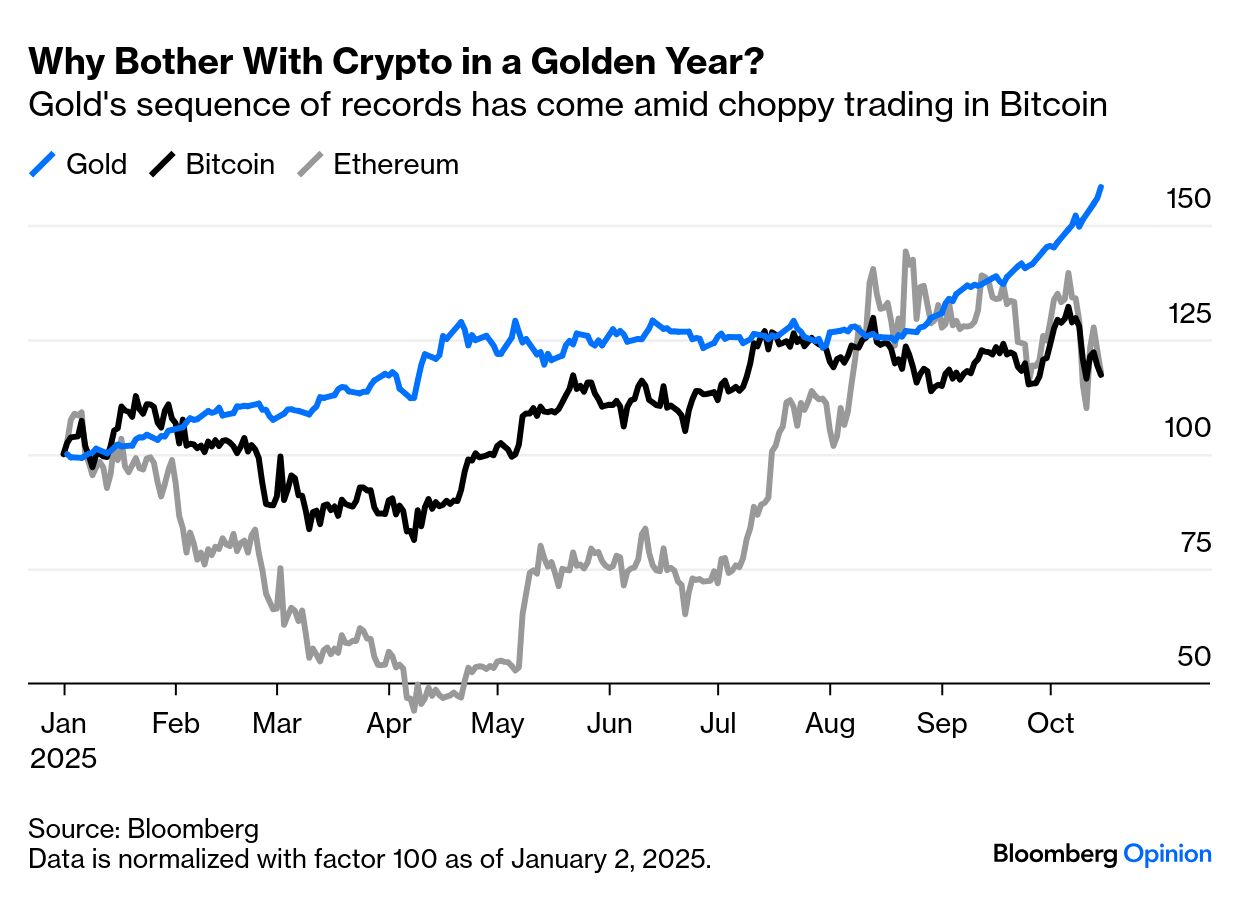

| The dawn of the stablecoin era, ushered in by the US GENIUS Act, carries the promise and peril of earlier financial innovations, from credit cards to derivatives. Anchored to fiat currencies and backed by liquid assets such as Treasuries, stablecoins are the crypto world’s closest approach to calm. To some, it’s a revolution in monetary efficiency; to others, every leap in finance brings its own risks. That has grown ever more apparent at this week’s annual meetings of the World Bank and International Monetary Fund in Washington. The IMF warned in its financial stability report that the $305 billion stablecoin market poses a systemic threat to the global financial system. Stablecoins face the risk of runs, like banks. Fire sales of assets against which they’re backed — like cash deposits and government securities — could spill into banks, government bonds, and repo markets. That would mean contagion and a self-fulfilling selling cycle, forcing central banks to intervene. Such risks are hard to ignore. The last wave of new financial products, like collateralized mortgage obligations, had just this effect nearly two decades ago during the Global Financial Crisis. The Basel-based Financial Stability Board, chaired by the Bank of England’s Andrew Bailey, argues that without clear regulatory frameworks — such as those envisioned in the Clarity Act that the US House of Representatives passed in July — stablecoins could undermine financial stability and thwart the development of a resilient digital-asset ecosystem. The European Stability Mechanism’s managing director Pierre Gramegna even said that “if they’re not guaranteed as central bank money, then obviously there’s a risk to the whole financial system, not just in Europe, but the whole world.” Such warnings may be weighing on performance. The Bloomberg Galaxy DeFi Index, which tracks the market performance and health of decentralized finance, has been having a tough time: And with great irony, this burst of crypto activity comes as the “barbarous relic” of gold enjoys a historic rally: Despite the skepticism, stablecoins’ promise is undeniable: They can be the bridge between crypto and the conventional payments system. Bitcoin was created to disrupt traditional banking but has so far barely had any effect on it. Now, Dante Disparte of Circle Internet Group Inc. argues that stablecoins have broken through into global payments and are drawing serious institutional interest. It is probably the first time in a very long time, if not ever, in the United States, that we have a technology-neutral, pro-competition piece of legislation that… reconciles the FinTech federalism that for many years has sort of held payments innovations at bay. Now the US is starting to take its place at the table.

Since the passage of the GENIUS Act, he says, “You've seen this wave of institutional interests come to play… embarked on this kind of Cambrian explosion of interest and innovation in this market.” The SWIFT network, backbone of global money and securities transfers, is also pushing stablecoins into the mainstream. It recently unveiled plans for a blockchain-based ledger to handle digital-asset transactions, including stablecoins. This would expand digital finance across more than 200 countries and territories. Banks such as JPMorgan, Bank of America, and Deutsche are providing feedback on the prototype. The financial system needs to be resilient. A brief outage, or anything to shake trust, could be disruptive in a really bad way. Unease about moving on from a system that does work is natural. But SWIFT’s Tom Zschach says the network is responding to customer demand: This is not really about disruption. It’s about choice. If you’re happy with the banking relationship you have, or you’re served very well as a corporate treasurer, you don’t have to do anything. Or you might say, there’s a better way to do that. There’s another service offered to me that’s faster and cheaper and safer. It’s kind of moving past this idea of this parallel universe. And people can see both tangible evidence of it working with some of the early use cases.

Stablecoins are already giving central banks a monetary-policy migraine. Jessica Renier of the Institute of International Finance notes that emerging markets’ growing use of dollar-backed stablecoins raises red flags about dollarization. As the coins can be moved swiftly across borders and skirt traditional channels, they might undermine capital controls. That’s a delicate challenge for central banks trying to preserve their monetary sovereignty. Crypto is an alternative to the dollar, but stablecoins might increase its power as a reserve currency. None of this justifies “overregulation” out of abundance of caution, argues Eugene Ludwig of Ludwig Advisors — who as comptroller of the currency at the US Treasury in the 1990s took a leading role in peeling back the Depression-era Glass-Steagall banking regulations. He argues that the Dodd-Frank Act after the Global Financial Crisis created an overly constrained financial sector in which banks are reluctant to innovate: By working with a new invention, you never know exactly what the steam engine would do, or the car would do, or whatever it is. It doesn’t mean to stop them, but when there are problems with them, you have to be prepared to jump in, solve those problems, and move on with what’s good about the technology, not what turns out to be problematic.

The crisis, which followed the deregulation of the 1990s, demonstrated just how difficult it is to distinguish the good and bad aspects of innovation in real time, but this appears to be the approach regulators are trying to adopt.

At best, the risks of decentralized finance can be mitigated — but eliminating them entirely isn’t realistic. The pragmatic approach is to embrace the technology while managing its challenges in ways that don’t choke off innovation. It’s a difficult and hazardous path but the one the technocrats in Washington will try to follow.

—Richard Abbey in Washington |