|

|

Welcome, everyone, to this week’s edition of Receipts. Kevin Warsh finally got his dream job, having been confirmed to the Fed chairmanship this week. He’s been positioning himself to get the gig for the past decade, after having been passed over during Trump’s first term because (in Warsh’s own words) “I did not put my ambitions ahead of my principles.”

Warsh just squeaked through this time after a long-running, reality-TV-style Trump selection process, which was followed by the narrowest confirmation-vote margin since the requirement for Senate approval for the role was established in 1977.

There’s a real wish-upon-a-monkey-paw vibe to Warsh’s story, though. Sure, he won his prize—but it’s far more treacherous than he may have initially calculated. Although presumably Jay Powell could have warned him.

The outlook for Warsh, an inflation hawk who nonetheless promised to cut interest rates, is the subject of today’s newsletter. Do you have suggestions for other routes he might take in the months ahead, if the inflation picture worsens? Drop them in the comments. And if you’re not already a Bulwark+ member, I hope you’ll consider joining. Your support helps give us the time and space to nerd out on markets and makes all our other work possible. Sign up today and get your first two weeks FREE:

–Catherine

Congrats on the Gig, Kevin Warsh. You’re Cooked.

He wanted to win the Fed chairmanship so badly. But what did he actually win?

|

IN ECONOMICS, THERE’S A CONCEPT called the “winner’s curse.” It means that the person who ends up winning an auction has often overpaid for the prize. It’s a good way of characterizing the fate of the newly confirmed Federal Reserve chair, Kevin Warsh.

Warsh has been auditioning to lead the Fed for over a decade now, muscling out competitors and massaging his public image. The main way Warsh finally got the gig was by pledging to cut interest rates, which was Donald Trump’s litmus test. Unfortunately for Warsh, he will not be able to deliver on that promise for reasons that are clear to everyone except, perhaps, Trump. This means that Warsh is hurtling toward a reckoning with his benefactor.

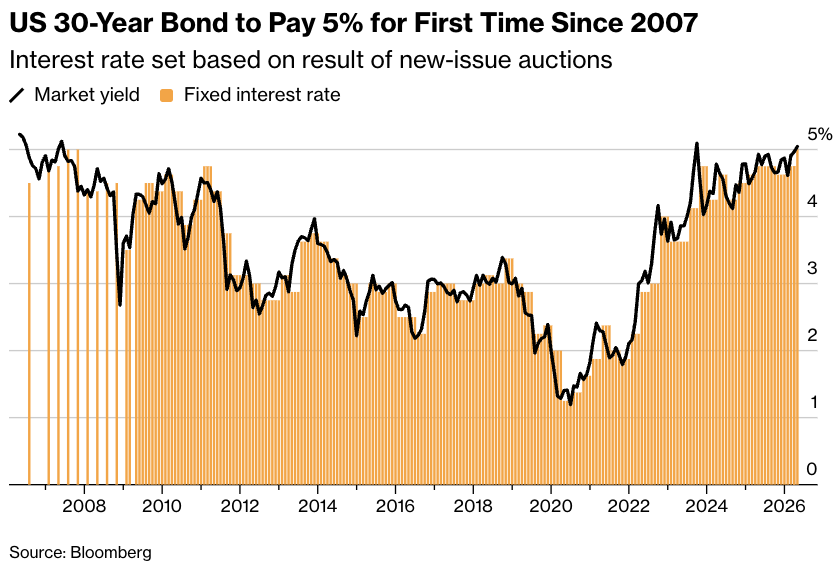

This is all related to the scary little chart right here:

|

Yesterday, for the first time since 2007, rates on new 30-year Treasury bonds surpassed 5 percent. And look, I realize that was possibly the most boring sentence you will read today.¹ So let me explain what it means, why it matters to the economy, and why it suggests Warsh is very, very cooked.

IT STARTS WITH TRUMP’S economic policy agenda.

Inflation had been drifting downward in recent years, at least roughly until “Liberation Day” in April 2025 when Trump announced global tariffs. The rate of price growth soon started ticking back upward.

Then the Iran war happened. And, as was evident in new reports this week on consumer and producer prices, inflation has been supercharged. With consumer prices reaching 3.8 percent growth in April from a year earlier, we’re likely seeing only the earliest glimmers of the war’s effects on prices for energy, food, manufactured goods, and so forth.

Even worse, this one-two punch of tariffs and war threatens to reset expectations for how bad inflation will get. What this means is that instead of these shocks being temporary (dare I say “transitory”), we could be at the start of a vicious cycle in which companies that are fearful of getting surprised by higher prices in the future raise their own prices preemptively today. If everybody does this at once, you get more inflation. It’s a self-fulfilling prophecy.

Companies and consumers aren’t the only ones who worry about inflation. Anyone who lends to the government worries about it, too: They don’t want the interest they receive on those loans to get eaten up by inflation. They want to make money!

This brings us to the infamous 30-year bonds. This week, there was an auction for Treasuries, which are the debt instruments the U.S. government sells so it can pay its bills. And buyers demanded higher interest rates on that government debt as compensation for the very real risk that inflation will run higher for a while. They demanded it both for shorter-term Treasuries and longer-term ones, as well. That’s why you saw 30-year bonds selling at their highest yield in nearly two decades.

If those bonds stay around 5 percent (or higher), a few things can happen.

First, obviously, is that the debt load the government carries becomes more expensive. U.S. debt was already on an unsustainable p