|

No, China did not manage to avoid a crash

But there are still things we can learn from how they manage their macroeconomy.

|

Back in the 2010s, a lot of people marveled at China’s seemingly recession-proof economy. Throughout the global financial crisis of 2008 and the Chinese stock market crash and capital flight of 2015, the country never recorded a single quarter of negative economic growth. Here’s what I wrote back in 2019:

China’s government seems to have developed a highly effective new form of economic stabilization. Its extensive control of the financial system allows it to turn on a flood of bank loans when the economy looks weak, and restrain credit when the danger has passed. China’s avoidance of recession in at least the past three decades suggests that this form of credit-based stabilization is more effective than traditional, more indirect stimulation of the economy through government deficits and central bank monetary easing…When a recession threatens, the government tells banks to lend --— to local governments, construction companies and real estate developers. Then, if the credits go bad, the government swoops in and takes the nonperforming loans off of financial companies’ books. Uninterrupted rapid growth then shrinks the government debt as a percentage of gross domestic product, and the system sails blithely forward[.]

And here’s what I wrote in 2018:

China…directed banks to lend lots more money [in 2009]. The World Bank estimated that increased bank credit represented 40 percent of China’s stimulus. Much of the lending was done by China’s four large state-owned banks. The money went to infrastructure, real estate and all kinds of corporate projects, many of which were carried out by the country’s state-owned enterprises.

Basically, most countries use two types of policy to get the economy moving again when some sort of negative shock hits it:

monetary policy (e.g. cutting interest rates), and

fiscal policy (e.g. stimulus spending).

Macroeconomists disagree about why interest rate cuts give the economy a boost, but most agree that the policy usually has an effect. Although there are many other theories and interpretations, one way you can think of rate cuts is as a financial policy — by making it easier for businesses to borrow and invest, low interest rates stimulate business activity. Fiscal policy, in contrast, pretty much bypasses the world of finance and aims directly at the real economy — you build a bridge or a road, which employs some people who might otherwise be unemployed, and then those people turn around and spend their money elsewhere in the economy, igniting a virtuous cycle of spending and working.

China uses both of those, but it also uses a third policy: financial policy. Instead of simply cutting interest rates and hoping that this filters through to bank lending, China’s government uses its direct control over the banking system to push banks to lend more. In the 2010s, after the Great Recession and the 2015 Chinese stock crash, this mostly meant lending to real estate companies. This lending fueled the biggest property boom the world has ever seen.

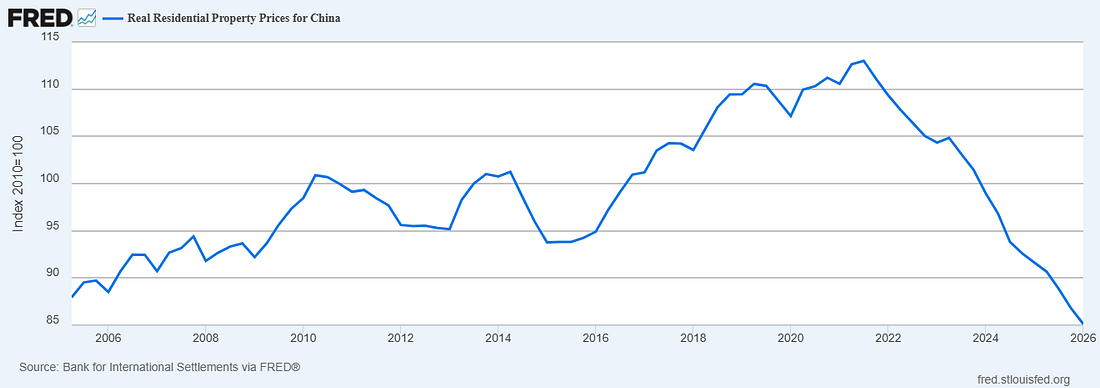

The boom ended in late 2021. The crash of the Chinese property developer Evergrande began a sequence of bankruptcies and defaults across the entire real estate sector. China’s property prices began to fall, and have not stopped falling to this day:

|

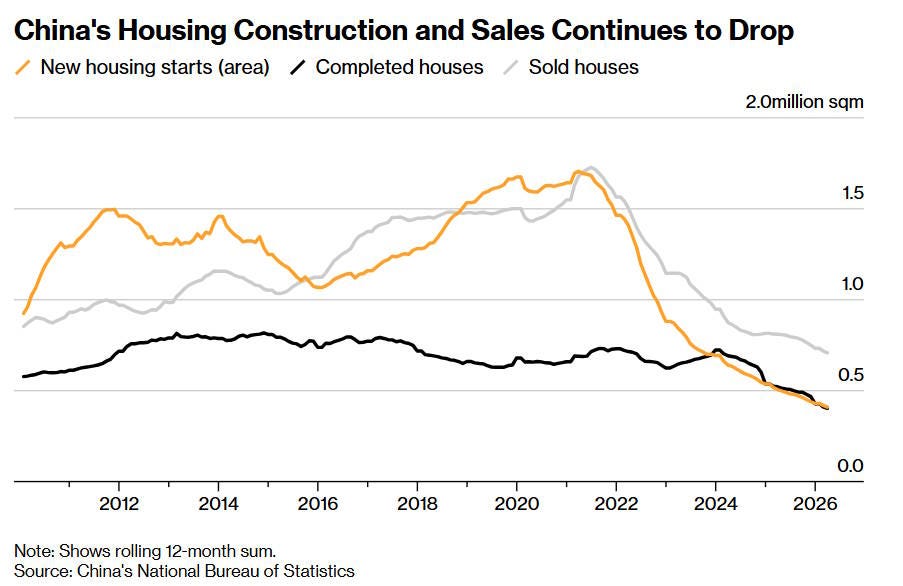

Chinese housing construction plummeted as well:

|

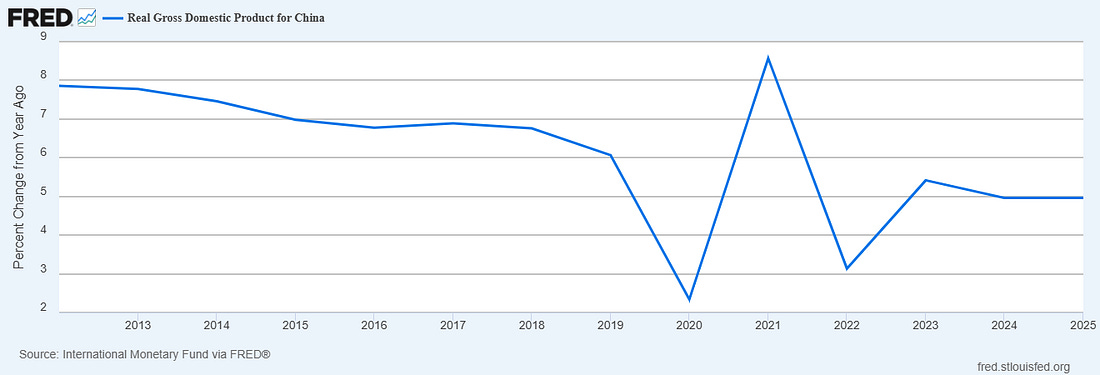

But despite the housing crash, China’s official growth rate never fell below zero — or even below 3%:

|

In fact, China did this by resorting to a version of the same playbook it used in 2009 and 2015. The Chinese party-state called up its captive banking system and told it to lend huge amounts of money to manufacturing companies. And that’s exactly what it did — industrial loans surged, even as real estate loans petered out: