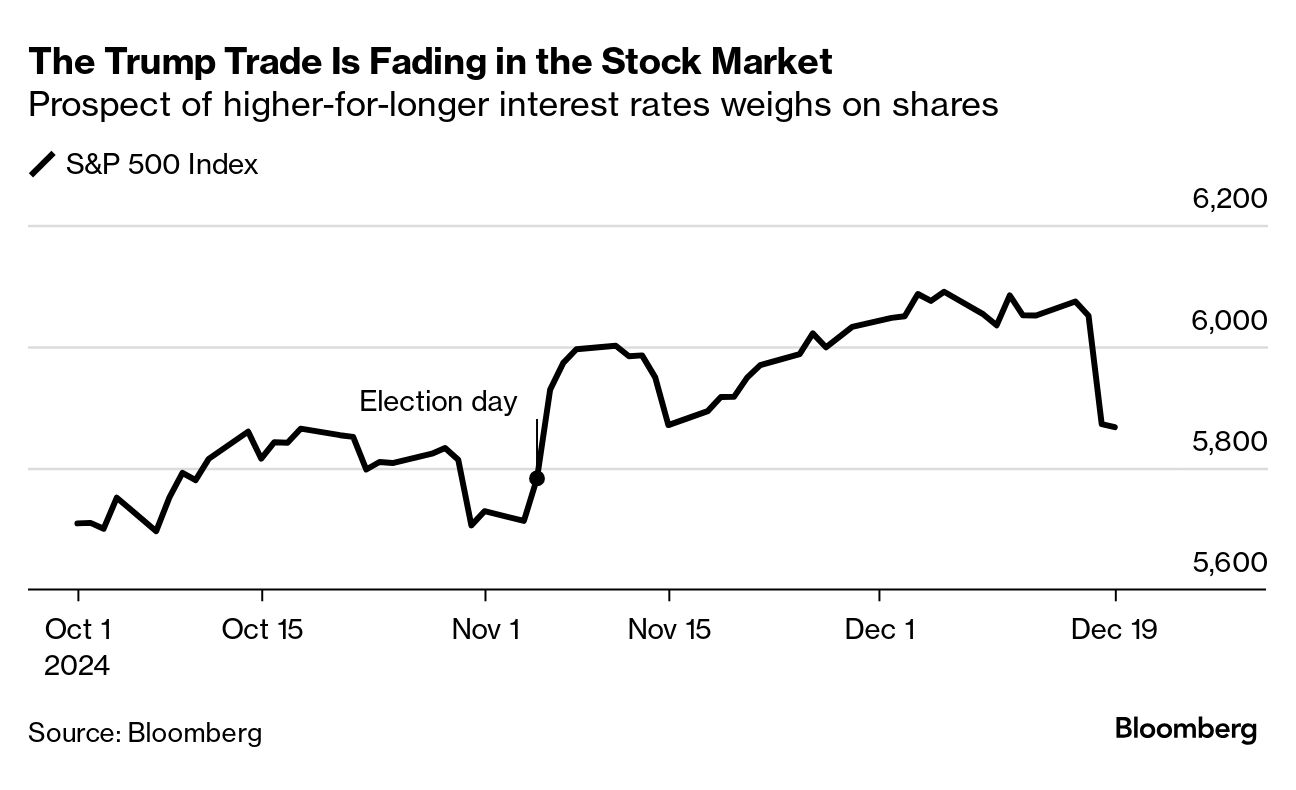

| Everyone says they support the fight against inflation. It's when they get punched in the face by the consequences that their resolve starts to waver. The price of inflation-related vigilance was on display this week when markets were sent into a tailspin by mildly hawkish posturing on the part of Jerome Powell, who -- while cutting interest rates -- indicated that future monetary easing would require improving data on prices. Stocks buckled, yields soared, and foreign currencies sold off. Investors tried and failed to stage a rally in the equity market yesterday. For the week, the S&P 500 is down 3%, heading for its biggest weekly drop in almost four months. A notable casualty from the lingering inflation threat has been the risk-asset incarnation of the Trump Trade, which saw things like value stocks and small caps surge as much as 8% in the weeks following his re-election. Those moves are effectively gone at this point. Even the S&P 500, which in early December was up more than 5% post-vote, sits just 1.5% higher now. How price action like this is apt to go down with the incoming administration is a matter of at least passing interest to investors. Conventional wisdom holds that Trump cares deeply about markets, with limited patience if the Fed creates excessive drama on Wall Street by pausing its monetary-easing program. But a report this week upended that wisdom. It cited transition insiders as saying the next administration actually wants Powell to keep up the vigilance, lest inflation revive and do to Trump what it did to Joe Biden. Right now, in that regard, bond markets at least are doing Powell's bidding -- and conceivably Trump's, if inflation is indeed his chief concern. Treasury yields of all stripes have surged, including yesterday, when the president-elect said the federal government should shut down if its debt ceiling isn't eliminated or extended.

There are two implications. First, in the event then that borrowing costs remain elevated, it would help to wring out excesses in the business cycle that continue to fuel inflation. Second, a casualty of all this would be riskier assets like technology stocks that have soared this year, benefiting from expectations that the hawkish monetary era is well and truly over.

Will investors laud this next “wait-and-see’’ chapter of Powell’s monetary campaign? Everyone says they support the fight against inflation. The question for investors is about to become: How much. —Chris Nagi |