| I’m Walter Brandimarte, managing editor for Latin America economics and government. Today we’re looking at turmoil in Brazil. Send us feedback and tips to ecodaily@bloomberg.net or get in touch on X via @economics. And if you aren’t yet signed up to receive this newsletter, you can do so here. - President-elect Donald Trump threatened the European Union with tariffs.

- The Bank of Japan warned against FX speculation after the yen hit a five-month low.

- Russia’s central bank unexpectedly held its key interest rate at a record-high.

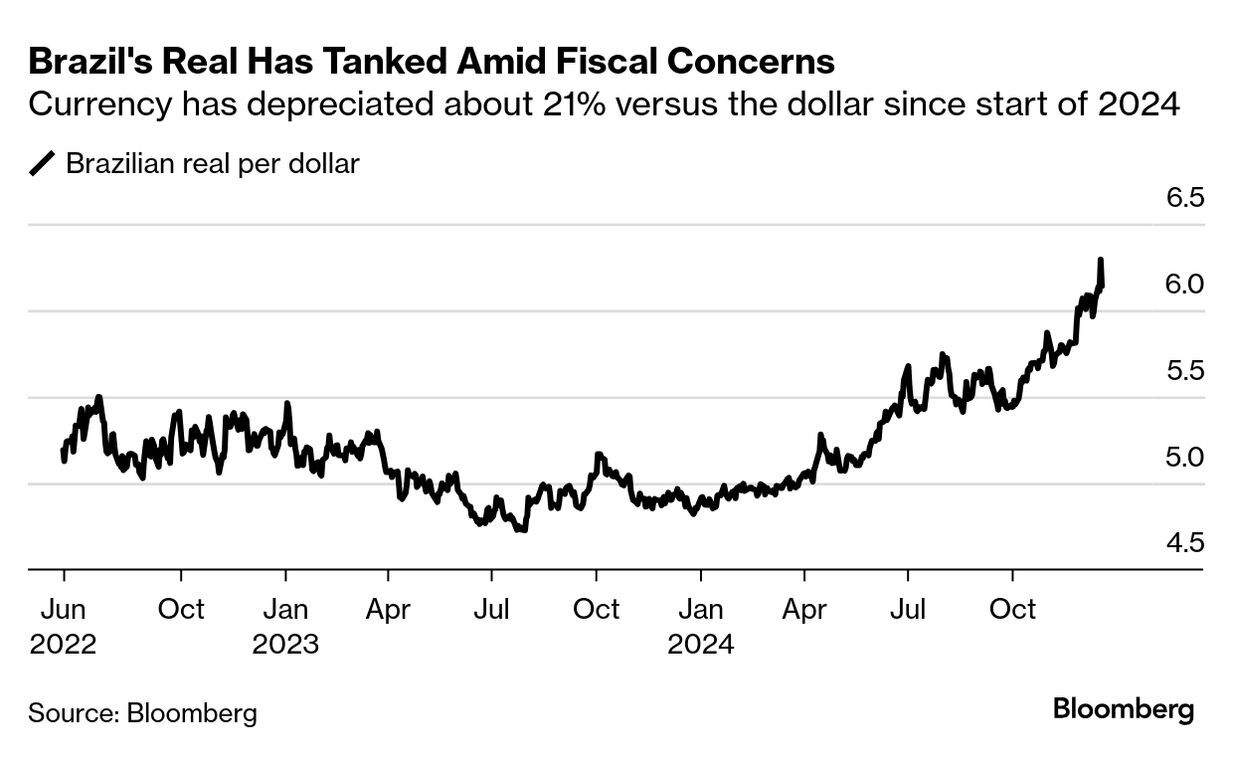

As 2024 kicked off, there was a lot to feel good about in Brazil. Latin America’s largest economy had weathered a Federal Reserve tightening cycle with flying colors, and could look forward to US interest-rate cuts. Inflation was within target. An export boom was underway. The year is ending altogether differently. After two years of President Luiz Inacio Lula da Silva’s pursuit of fiscal expansion, investors this month appeared to have had enough, dumping Brazil’s currency en masse. The crisis of confidence has even sparked a question over whether monetary policy — regarded as having been well managed in Brazil in recent years — can even be effective. Fiscal dominance, the term economists use for the condition where public borrowing is so big it “dominates” a central bank’s intention to contain inflation, has suddenly become Brazil’s big buzzword — from trading desks to Wall Street banks’ research notes to comments from influential figures like investor Luis Stuhlberger and ex-central bank chief Arminio Fraga. Both outgoing central bank Governor Roberto Campos Neto and his successor Gabriel Galipolo reject the doubters. But the sequence of events speaks for itself: on Dec. 11, the bank took the bold step of jacking up its benchmark interest rate by a full percentage point, and surprised with a pledge to deliver two additional hikes of the same size by March. After the move won initial praise and spurred a rebound in the real, markets turned before the following morning was over. Since then, the monetary authority has scrambled to arrest a depreciation that threatens to escalate inflation pressures. It’s sold dollars from its reserves, and offered currency swaps and credit lines in greenbacks — the impact of which has all been temporary. The underlying challenge is that Lula and his team remain committed to public largesse, having stepped up welfare distributions even at a time of record unemployment — fueling inflation. Brazil’s central bankers argue that they’re not done yet, and that high interest rates will eventually slow down the economy and bring inflation back to target. Whether that proves right, and what the ultimate economic cost will prove to be, will be answered in 2025. The Best of Bloomberg Economics | - UK retail sales grew more slowly than expected in November suggesting Christmas shoppers might not boost the economy in the crucial final months of the year. Meanwhile, the Bank of England is shifting its focus from reacting to wage and price data to relying on its own forecasts.

- Some of China’s wealthiest cities are struggling as economic malaise spreads.

- Giorgia Meloni keeps managing a feat that her predecessors as Italian prime minister long struggled with: earning ever greater trust from investors.

- The Philippine central bank may ring in a new year with a rate cut, according to the governor.

- Emerging markets including Indonesia ramp up currency defense after the dollar surged following the Federal Reserve’s revised rate cut path this week.

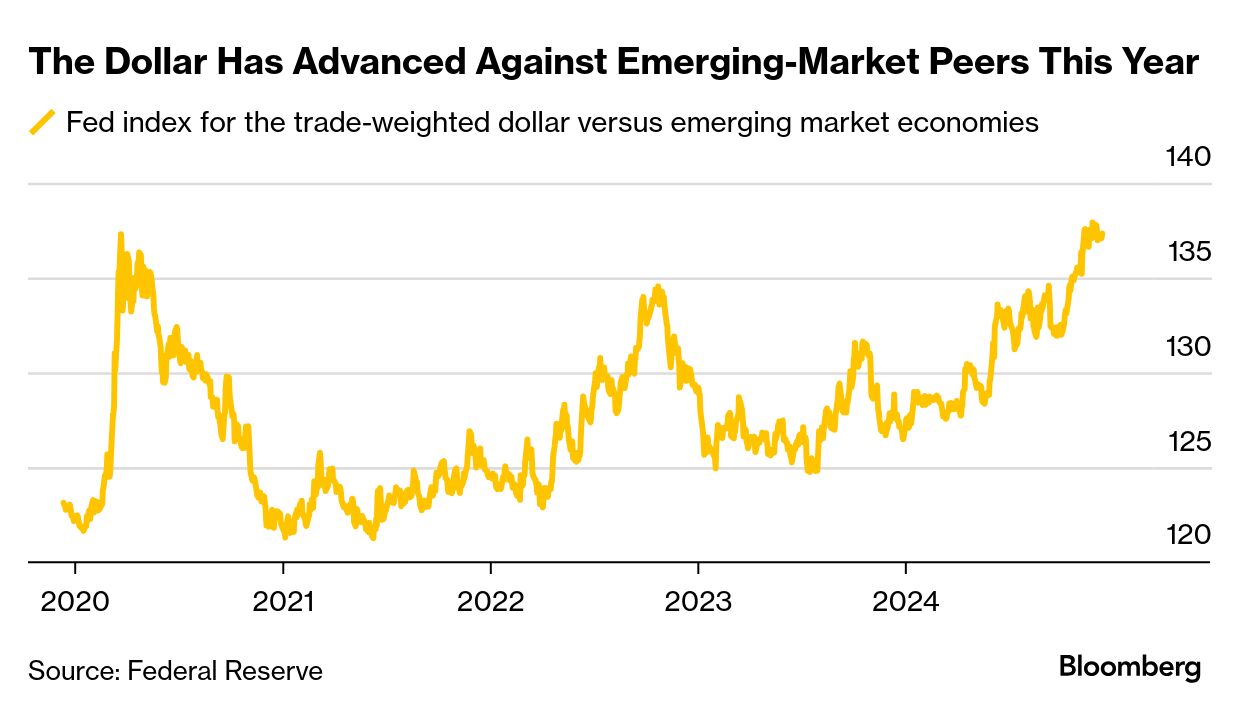

The Institute of International Finance cautions that emerging market central banks may find themselves under further pressure next year as policies adopted by the incoming Trump administration put upward pressure on the dollar — and downward pressure on their own exchange rates. “The Trump administration’s expected infrastructure spending, tax cuts to corporations, re-affirmation of the 2017 personal income tax cuts, trade tariffs, and tighter immigration rules — all pointing to higher interest rates — would reinforce the dollar’s strength,” IIF economists Marcello Estevão and Jonathan Fortun wrote in a note Thursday. That could “intensify global financial tightening,” they said. “For emerging markets, the risks of capital flight, inflationary shocks, and fiscal constraints will require innovative policy strategies in 2025 to navigate the challenges posed by a persistently strong dollar,” they wrote. |