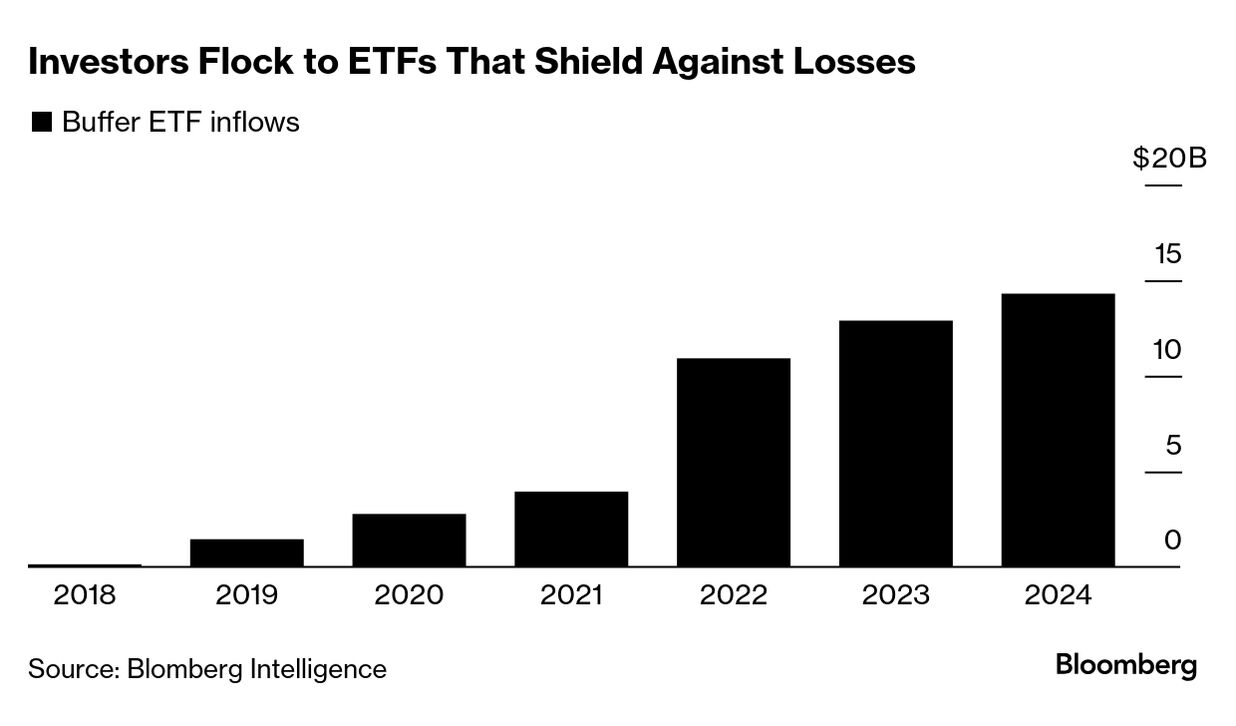

| We’ve spoken before about the boom in buffer ETFs, which use derivatives to cushion investors against downside in exchange for a cap on upside potential. The category has attracted an interesting new fan: the University of Connecticut’s $634 million endowment. As reported by Bloomberg’s Emily Graffeo, the UConn Foundation sold almost all of its hedge fund exposure during the most recent fiscal year and bought so-called buffer ETFs, said David Ford, chairman of the investment committee. Hedge funds have become a “victim of their own success,” with many growing so large that returns have suffered, Ford said. Instead, he says buffer ETFs are a cheaper and easier way to lessen portfolio volatility relative to using a hedge fund or structuring a bespoke trade, and come with the benefit of improved liquidity. “This takes the complexity out of hedging, or most of the complexity,” Ford said. “Instead of having to go to an institutional desk and say, we want to design the following options trade, it’s already prepackaged and trading.” UConn has purchased buffer ETFs overseen by Innovator Capital Management, where the average fee for the products is 0.8%, according to data compiled by Bloomberg. Compare that to the typical fee structure of top hedge funds, which have historically charged clients 2% of assets managed and 20% of profits. Anita Rausch, AllianceBernstein’s global head of ETF capital markets, said that to see endowments step into the industry is a natural evolution of the wrapper. “It’s a huge moment but it’s something to be expected. It’s what the ETFs are revered for. They’re revered for cost efficiency, they’re revered for liquidity, they’re revered for ease of ease,” Rausch said on Bloomberg Television’s ETF IQ. “They’re going away from the hedge fund, getting that same risk-management strategy in the ETF wrapper at a cheaper cost.” |