- The euro-area economy will pick up less momentum next year than previously foreseen and only expand slightly more strongly than in 2024.

- As China’s property crisis enters a fifth year, there’s little sign that things will improve anytime soon.

- President-elect Donald Trump picked a former Treasury official to head the Council of Economic Advisers.

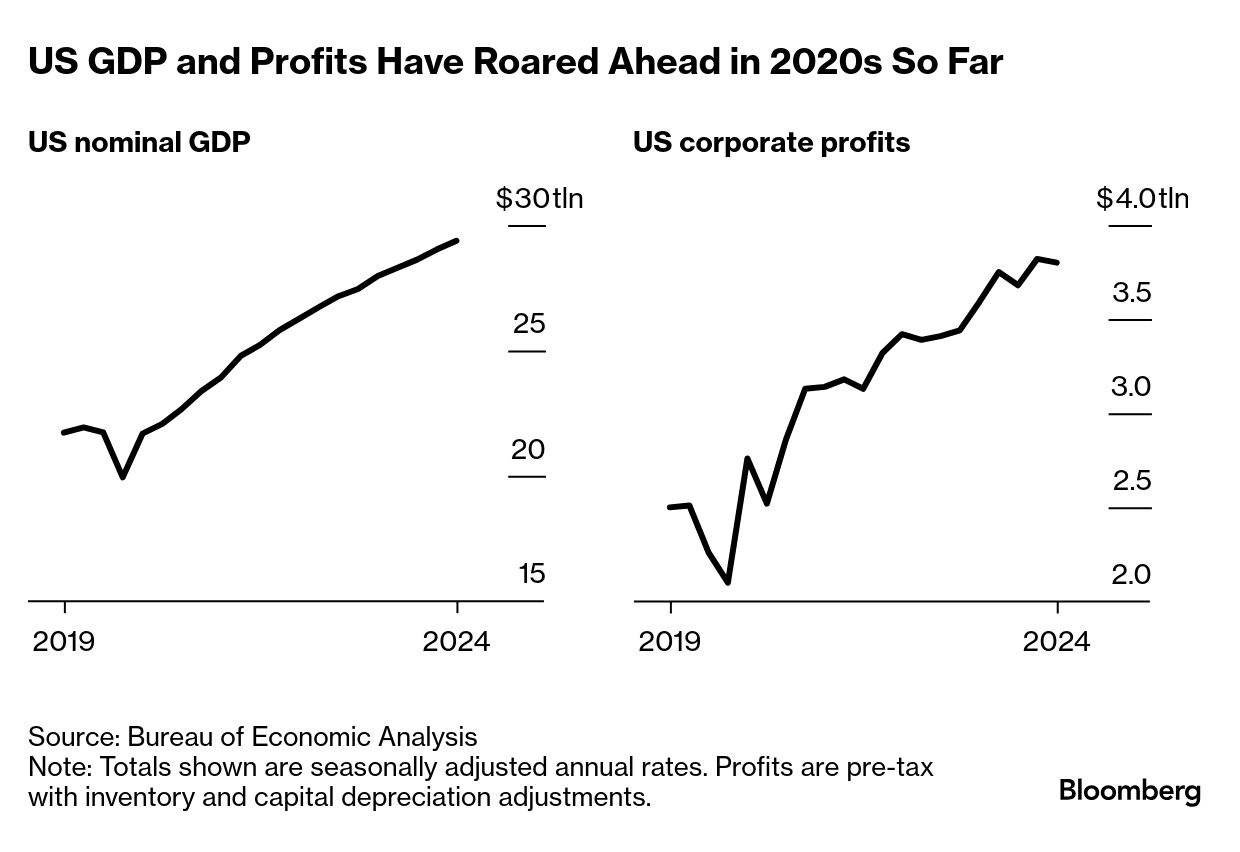

When the world entered the 2020s with a mass human crisis that killed millions, things could hopefully only improve from there. Thankfully, they did. In the US, it’s not a stretch to say there’s been a “Roaring ’20s” quality in markets and many parts of the economy — taking a page from the post-World War I boom of the 1920s. That’s how veteran economist and market observer Edward Yardeni has described it, saying the new era features strong productivity, growth and substantial equity returns. Those investing in the S&P 500 Index at the start of the 2020s have roughly doubled their money. Nominal US gross domestic product has climbed almost 34% since the 2020s began. Corporate profits have soared more than 50%. Read More: Elon Musk Makes ‘Overstaffed’ Fed Target in Quest for Efficiency Next year may pose the biggest test yet for what’s been a terrific economic and markets rally. President-elect Donald Trump takes office in four weeks, pledging a raft of measures that could reshape the outlook, including major trade restrictions and an historic deportation of immigrants — who have in recent years contributed to a notable acceleration in US labor-force growth. “A Trump presidency has the potential to reshape the US economic and geopolitical landscape,” Swiss bank UBS’s chief investment officer wrote in a note earlier this month. Federal Reserve Bank of New York President John Williams was candid on Friday in calling out the degree of unpredictability about 2025, saying that with regard to the central bank’s monetary stance, the issue was “getting policy well positioned for whatever may come next.” That provided some context for Fed policymakers last week reining in their expectations for interest-rate cuts in the coming year. Williams, who’s vice chair of the Fed’s rate-setting committee, said he’d incorporated into his forecasts some thinking about how immigration, fiscal policy and other factors will evolve. But “there’s just a lot of uncertainty about what’s going to happen next year,” he said in an appearance on CNBC. Odd Lots Podcast: Fed’s Mary Daly Explains the ‘Hawkish Cut’ While many economists see tariff hikes and immigration curbs as having the potential to both push up inflation and curb demand — a stagflationary shock — surveys have suggested resounding confidence in Trump’s plans for deregulation, energy-industry expansion and an extension or even expansion of tax cuts. And negotiations with US trade partners, along with domestic legal challenges, could diminish the scope and impact of tariff and immigration measures, UBS says. The bottom line, says Mark Haefele, chief investment officer at UBS Wealth Management: “we have to be prepared for a wide range of outcomes in the year ahead.” The Best of Bloomberg Economics | - UK economic data relied on by markets, businesses and the government are cast in doubt as survey responses collapse.

- The European Central Bank is nearing its consumer-price target but must remain alert to lingering dangers in some sectors, according to President Christine Lagarde.

- Emerging markets underperformed US stocks, many of their currencies have fallen against the greenback and economic pain is set to intensify with tariffs.

- Private sector activity in the UK is set to decline steeply in the next three months, warns the Confederation of British Industry.

- In Japan, consumer loans surged by the most in 16 years and bankruptcies are set to hit more than a decade high as an era of ultra-cheap money ends.

- Hong Kong’s Financial Secretary vowed to boost innovation and liquidity in financial markets after President Xi Jinping said the city needed to better integrate into China.

In a further sign of the disinflation process proving “bumpy,” as Fed policymakers like to put it, the price of Christmas continues to rise. Specifically, the items in the classic carol, The Twelve Days of Christmas. For some 41 years now, Pittsburgh’s PNC Bank has run a light-hearted estimate of the cost of the full package, from the partridge in a pear tree to 12 drummers drumming. PNC’s “Christmas Price Index” increased 5.4% this year, double the gain seen for 2023. Boosted wages for skilled labor pushed up the cost of the performers – including the dancing ladies and piping pipers.  Source: PNC “We’re still seeing the cause and effect of the pandemic-inflation hangover, even nearly five years later,” says Amanda Agati, chief investment officer of PNC's Asset Management Group. “With years of steep price increases, we’d think inflation has nowhere to go, but we’d be wrong. This latest PNC CPI is an accurate reflection of what we’re seeing in the market.” |