It’s Inauguration Day, and if you’re wondering how soon the new administration could impact your wallet, the answer is: very soon. Over the years, Congress has granted the executive branch broad oversight of tariff implementation. In the short term, these taxes on foreign goods may drive up the prices of everything from beauty products to groceries. And even if you’re committed to buying “Made in America,” the higher costs of imported components could make that more expensive, too.

Every new administration inspires a mix of economic optimism and uncertainty. But this one is eager to act quickly on economic promises, pledging to impose tariffs on at least 10% on all foreign goods, applying even steeper taxes on imports from Mexico, Canada, and China. Oh, and President Trump plans to do this on Day One of his presidency. He has floated the idea of declaring a “national economic emergency” to expedite these moves. He’s even threatening to impose a 25% tariff on goods from Canada — a key US trading partner and energy supplier — citing concerns over Canada's alleged role in illegal immigration and fentanyl trafficking.

The best way to prepare? Stay informed and flexible. Know where your favorite brands are made, pay attention to prices as they hit your cart, put some extra padding in your budget for big ticket purchases — and maybe buy that new phone sooner rather than later.

High-yield savings accounts are great … unless your bank actively misleads you and their other customers out of a collective $2 billion.

Money Talks

Q: My husband makes a lot of money. I do not. He keeps saying it’s “our” money, but 10 years and two kids later, I still feel like it’s his — his earning power means he drives our decisions. How do I make sure I have a say? — Our money, my voice

“I can almost guarantee you haven’t had a real conversation about money,” says Sethi. The good news? It’s never too late to change the script. Here’s how:

1. Redefine What “Contribute” Means

“Many people think earning money equals power in a relationship. I reject that premise,” says Sethi. Contribution isn’t just about paychecks — it’s about everything you bring to the table. Whether it’s caregiving, emotional support, or managing the household, fully understand that you’re an essential part of the team.

2. Start a Positive Conversation

Money usually comes with a side of stress, notes Sethi. Change the dynamic. Your first money talk should be about what your cash has already done for both of you. Then, ease into discussing your shared dreams and goals. It’s also OK to admit these conversations leave you feeling unsure or overwhelmed. Ask how your partner feels as well, and remember to keep the chat short. It’s about opening a dialogue, not arriving at an immediate consensus.

3. Know Your Numbers

“Have some skin in the game,” says Sethi. Schedule regular money check-ins (think: once a month) to review savings, retirement accounts, and goals. When you know the numbers, you’re equipped to start informed, meaningful discussions — and make decisions together.

Finally: You’re not alone. Sethi talks weekly to couples facing money challenges: The couple worth over $1M who can’t agree on spending, the couple trying to figure out how partnership works when one parent becomes stay at home, and the couple making nearly $27,500 a month who still stress about finances and he says it’s never too late. “Talking about money is one of the most courageous things that a couple can do in their relationship,” he says. So start the conversation!

Use the letters below to identify the word or phrase. Then, click to reveal the answer.

Clue: A ratio that measures how much of your income goes toward debt payments. It's also a key number lenders use to decide if you're ready for a mortgage or some other big-deal loan.

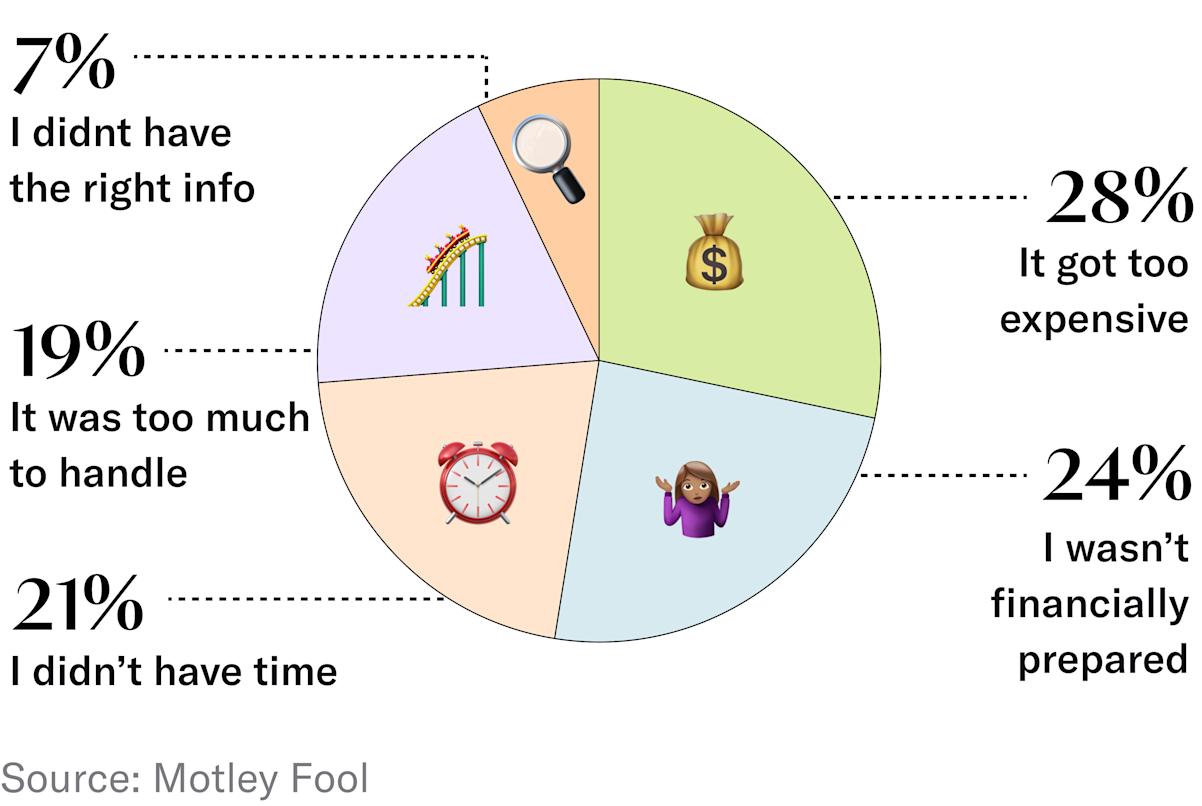

What got in the way of keeping your financial resolution last year?

If setting your child up for success is one of your money goals this year, a low-effort proactive step like opening a Fabric by Gerber Life kid’s investment account can help. They make kick-starting your child’s financial future easy, thanks to quick onboarding, low minimums, and automated investing. Start with as little as $20 and enjoy perks like penalty-free withdrawals for current child-related expenses (which are probably piling up right about now), plus zero hidden fees. Psst…once they become an adult, the account is all theirs. But don’t wait, if you open an account before the end of the month, you’ll get $25 to start†.

Wealth Builder

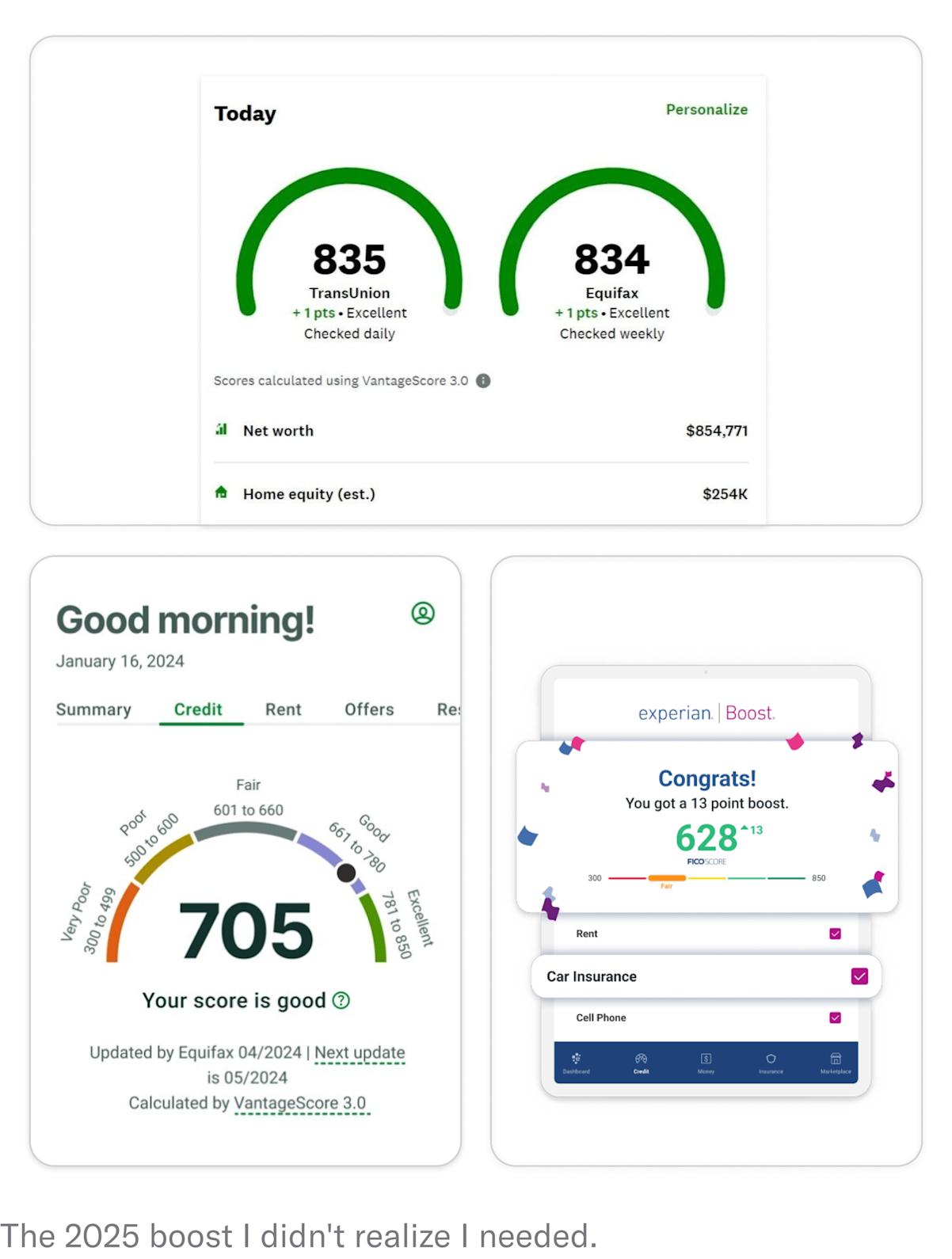

Credit Up, Stress Down: 3 Tools to Boost Your Score

A higher credit score isn’t just a number — it’s your ticket to lower rates on budget-altering things like mortgages and car loans, and it can improve your chances of getting approved for new credit. If your score isn’t quite where you want it, paying down debt is a solid first step. But if you’re looking for extra help, these tools can give your credit a boost:

Rent payments: Rent is often your biggest monthly expense, but it typically doesn’t count toward your credit score. The fix? Use apps that report your on-time rent payments to credit bureaus. One to try: Esusu. For $2.50 a month, Esusu reports your rent payments to major credit bureaus, helping your score reflect how reliable you are.

Monthly bills: Your phone, internet, and utility bills don’t usually show up on your credit report. But they could. One to try: Experian Boost. This free tool lets you add eligible monthly payments — like your cell phone or streaming services — to your credit report, even if you pay via debit card or automatic bank transfer.

Credit-Builder Loans: These loans are designed to build credit from scratch or repair a low score. You borrow a small amount, but instead of getting the cash upfront, the lender holds onto it in a savings account. As you make payments, your credit score gets a lift — and you’ll typically get the full loan amount back at the end. One to try: Credit Builder from Credit Karma. It helps you build credit while saving money, with no hard credit check required.

SKIMM+

Even More Smart Money Moves on Skimm+

Skimm+ is the membership that helps you seamlessly handle life's complexities, learn from Skimm'rs who have been there, and spend your money wisely with perks on services you already use.

Key membership features:

Databases with real numbers and honest intel on everything from daycare costs to self-employed salaries, sourced from Skimm'rs.

Scripts to help you handle tricky conversations, like negotiating a raise and navigating parental leave.

Live workshops and Q+As with our favorite experts.

Gone are the days when you had to spend a fortune to look like you make a fortune. These clothes and accessories look expensive, but they secretly...are not.

Psst…love our recs? Follow @skimmshopping on Instagram for more products, gifts, and services that are actually worth the hype (and the price tag).